Investing in real estate when interest rates are rising can be a challenging decision. But if you know what you are doing, there is a world of opportunity.

When interest rates rise, finding profitable real estate deals may be difficult. What might be a fantastic deal when mortgage rates are low could potentially lose you money when mortgage rates are high. In times of high interest rates, people tend to panic, and novice investors or owner-occupied borrowers think the best idea is to wait it out and start investing when central banks pivot again.

But this approach means they miss out on some amazing deals and delay their investment goals. For those beginning their investment journey, it could mean never actually getting started. Are you aware that currently, 84% of Californians may be forced rent because it has become “unaffordable”? For sophisticated real estate investors, this means an opportunity to obtain the highest rent while also having the power to negotiate the purchase price of real estate. A perfect storm for savvy investors!

The key is to know how to invest in real estate in a high interest rate environment. This allows you to make the most of the situation and come out stronger. For those who know what they are doing, these times are great for finding amazing deals. If you know what you’re doing, these times can greatly increase your net worth.

There is a reason why this statement holds true through time:

“Money can be made in bull markets. Fortunes are made in bear markets.”

Use Interest Rates in Your Negotiations

When buying an investment property in America, many may be concerned about whether the deal will be profitable when interest rates are on the rise. There will also be worry about where interest rates could be in the future.

This may seem like a bad position to be in. But guess who else will share these worries? The seller and the realtor selling the property. Both the seller and realtor will be aware that fewer people can afford to buy their property. They’re also aware that if they don’t sell the property fast, interest rates could rise again.

In this current market, the experienced real estate investor will ensure interest rates are part of the conversation when negotiating. If one does this correctly, one could get an excellent deal with the right seller. This is particularly true if the property has been on the market for a while and the seller is motivated. If a seller waits too long when buyers are skittish, they may be waiting a very long time to sell the property. Use this market pressure to your advantage!

Getting a great deal is particularly important in these circumstances, as buying a property below market value will give you some leeway in volatile market conditions. It also puts you in a fantastic position when interest rates go back down, and property values rocket up.

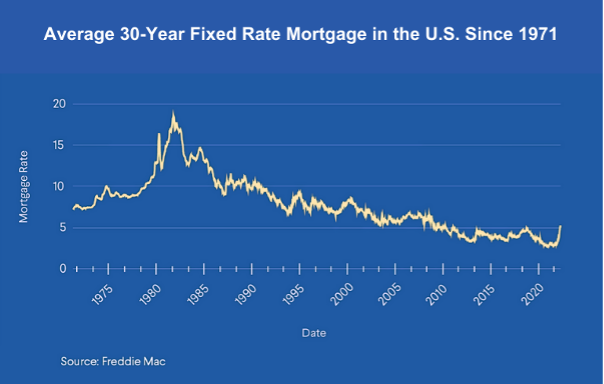

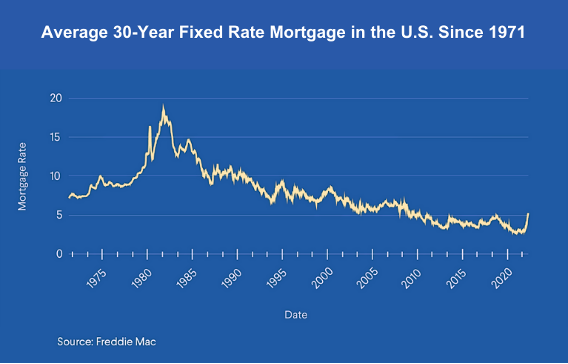

Fixed-Rate Mortgages

Unique to the U.S. and one of the most valuable tools rental property investors have in the U.S. is the 30-year fixed-rate mortgage. Surprisingly, this style of mortgage is very much an outlier compared to what’s typically offered in other countries. Most countries tend to offer adjustable, variable, flexible, or renegotiable rate mortgages, all of which pose an inherent risk with the potential of an unexpected interest rate hike during the ownership of the property.

Rent Increases

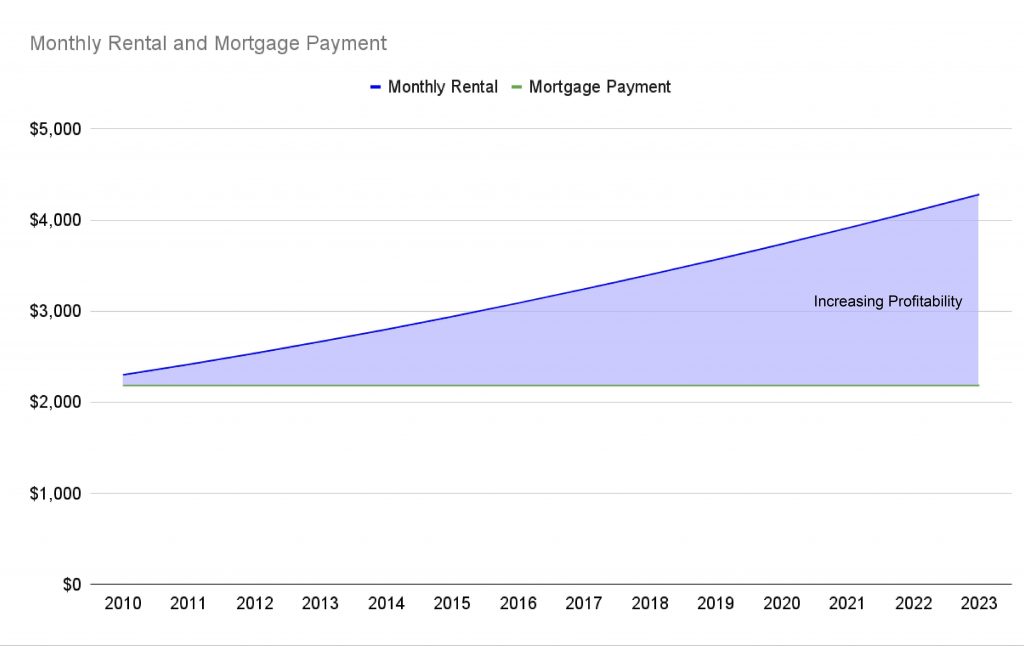

As pointed out, a rental property’s projected cash flow is based on today’s rents, not tomorrow’s. Rents increase for two reasons: appreciation and inflation.

Guess what doesn’t increase over time and is not affected by appreciation or inflation? Your mortgage payment when you have a fixed-rate mortgage!

This means your cash flow spread will continue to grow over the life of your rental property as you continue to increase rents.

Your expenses, such as property tax and insurance, may increase over time, but they’re unlikely to increase at a rate anywhere near what rents will increase. Overall, you’ll see that rents will continue to pull farther and farther away from your fixed-rate mortgage expense, and your profits should continue to grow exponentially.

How a Rental Property Makes Money

Before learning about U.S. real estate investing, you may have known that rental properties in America can be much more profitable than you think with the right tools and partners.

The five ways that rental properties can make money are:

- Cash flow

- Appreciation

- Tax benefits

- Equity built via mortgage paydown

- Hedging against inflation

When you understand the details of each profit centre, you will not only become savvier about the power of holding a rental property long-term instead of short-term, but you’ll also begin to realise that the expense of an interest rate that’s a couple of points higher than what you’re used to likely doesn’t hold a candle to the profit potential over the lifetime of the rental property.

You may already be saying, “But those other profit centres are speculative, and cash flow is still important, and the higher mortgage expense increases my risk by lowering my cash flow.” However, when dealing with this situation, your approach should focus on two essential factors:

Learn how to manage your various sources of income. If your available funds decrease due to a higher interest rate, explore other ways to make money. For instance, if you’re purchasing property in an area that’s improving and in high demand, you might expect its value to increase. Alternatively, if you’re investing when prices are rising a lot, how could you adapt? Visualise this like a chart with different bars representing each way you make money. If one bar goes down, are any of the other bars going up? If they’re all going down, that’s a concern.

When some bars are higher than usual, do those help to balance them out? It all depends on your specific situation.

Put a big focus on location and demand. Just like in the earlier example, a crucial factor is buying properties that can contribute to the “appreciation” part of your earnings, along with inflation and rental demand. When people really desire the properties they own, the chance for higher profits from these profit centres increases, and these profits will continue to grow consistently over time.

When you understand how rental properties make money, you can begin to wear the investor hat rather than the consumer hat. It’s the consumer mindset that often leads people to view increased interest rates as deal-breakers. However, those who genuinely understand how rental properties make money not only learn to look beyond the interest rates but also gain insights into how to compensate for it.

Find Cash-Flow Strategies

The traditional buy-to-let approach, while profitable when interest rates are low, might not be effective when rates are higher. Deals that used to bring in good cash flow with a low-rate interest-only mortgage could turn into situations where you break even or even lose money when rates are up. This means that traditional landlords and property investors miss out on many opportunities. This is where creative, informed, and forward-looking investors thrive. If you think outside the box, you gain a clear advantage in this kind of market.

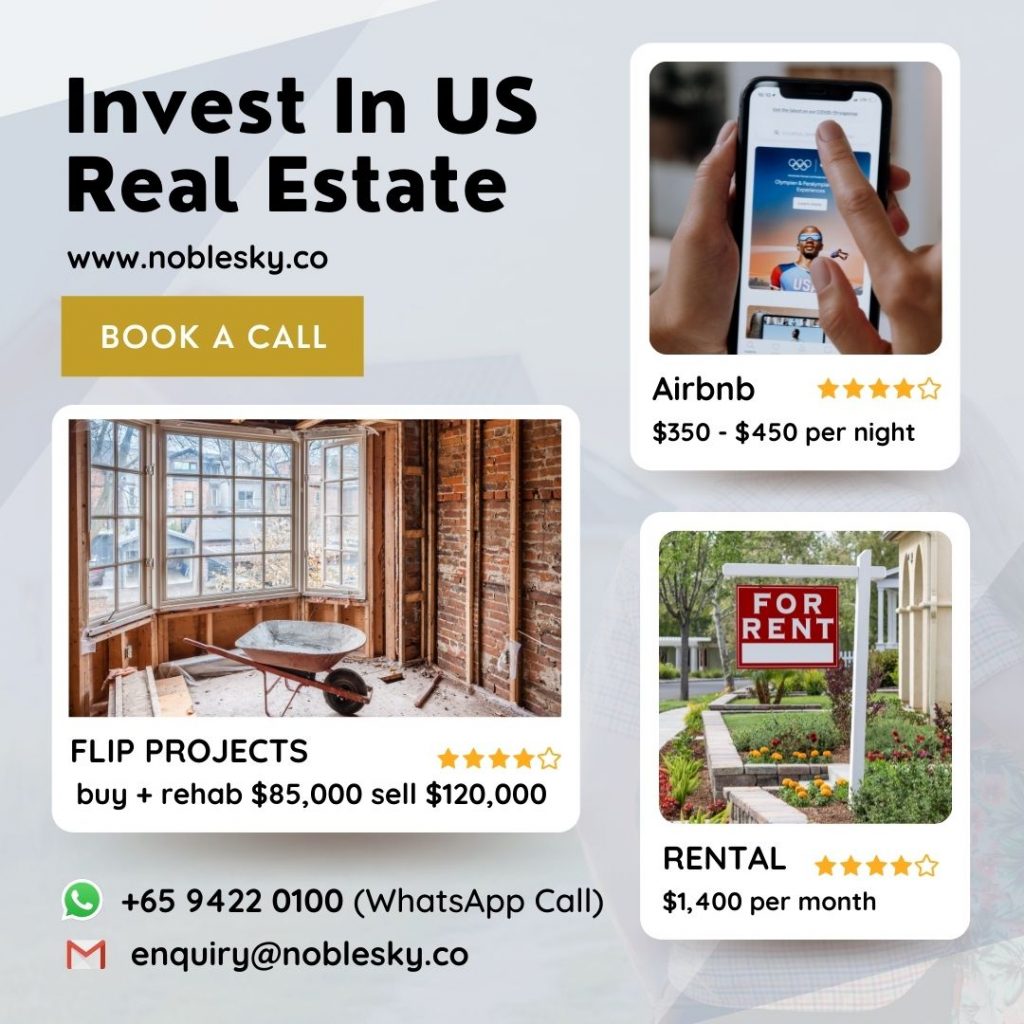

An example of this is serviced accommodation. A property that might have generated low cash flow single-family buy-to-let can turn into a profitable short-stay let business. Renting it out on platforms like Airbnb can earn you much more than renting it out for the long term.

There is a broad range of clients for serviced accommodation, and it isn’t just holidaymakers. You don’t necessarily need to be in a vacation location as short-stay lets are used by everyone from contractors to re-locators. Simply find a location reasonably close to a chain hotel and check that the hotel is regularly fully booked.

Think Long Term

Property prices are volatile when interest rates are high. You should not be thinking about the cost of the property in short to medium term. If you have bought a high cash-flowing property, you should consider it a long-term hold. Don’t become overly concerned with month-to-month or even year-to-year price movements.

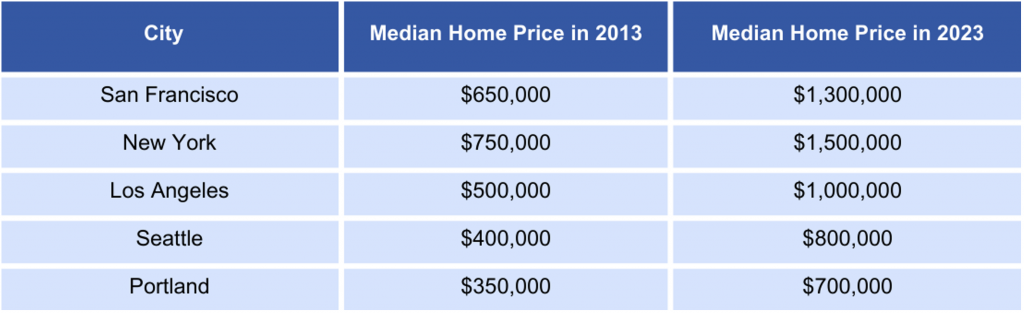

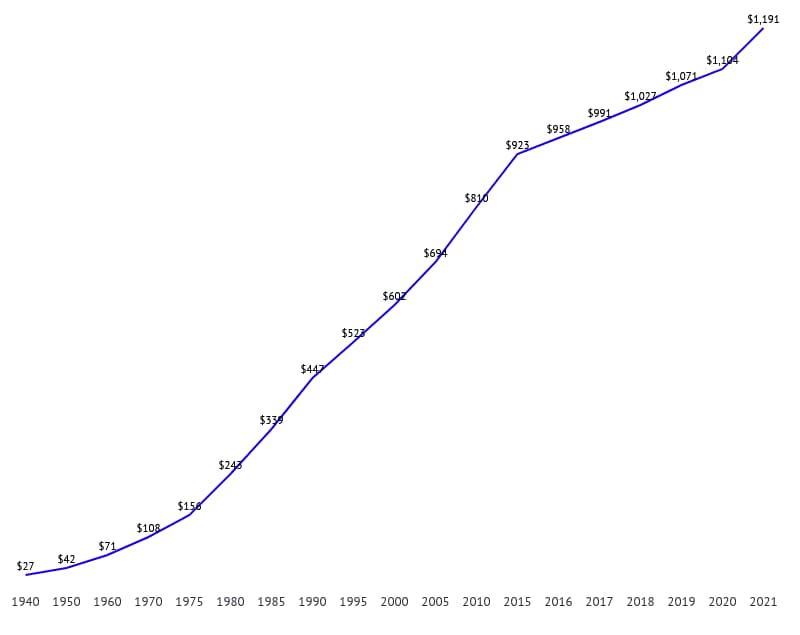

While past performance doesn’t guarantee future outcomes, real estate has historically been a reliable long-term investment. The global population continues to grow, and right now, there’s a shortage of at least 6.5 million properties in the U.S. Remember that in certain regions and cities, available housing space, especially in desirable areas, is limited. If you’re patient and able to wait out market fluctuations, there’s a strong chance you’ll reap significant rewards.

In conclusion, a high-interest rate environment can be a great time to buy an investment property, provided you’re well-informed. While the market might discourage other investors and property owners, you have the chance to uncover valuable opportunities. This means being creative, having the necessary experience, or having the willingness to gain the necessary knowledge to succeed in such a situation.

There is a world of opportunity for those willing to put in the time to learn and understand how to invest in real estate in times of rising rates. Many new millionaires and billionaires will be made in these times; it is up to you whether you will be one of them!

As a company America Mortgages has one focus, providing market rate mortgage financing for Foreign Nationals and U.S. Expats. This is all we do.

This is our expertise and no one does it better.

If you’re a sophisticated investor you will understand why working with experts in their field is so important. If you’re new to the U.S. real estate investor market, we welcome you to give America Mortgages the opportunity to work with you hand in hand to build your real estate portfolio in America. Getting approved for a mortgage is the first step. To arrange a convenient time to speak with a U.S. Mortgage Specialists in your time zone, please use this convenient calendar link.