04:31

Donald Klip

Hi, everybody. Thank you for joining us. For another one of our webinars. This is quite a unique webinar. We have not had a founder’s chat for a long time. So, I’m happy to have my co-founder of global Mortgage Group and American Mortgages, Donald Clipp on with me to discuss not only the recent rate drop, but some really amazing enhancements for our business, which certainly adds or certainly adds value to you as clients and to our loan officer team and so forth. So, Donald, thanks for joining. It’s been a while. I’m glad you’re able to make the time for this.

05:22

Speaker 3

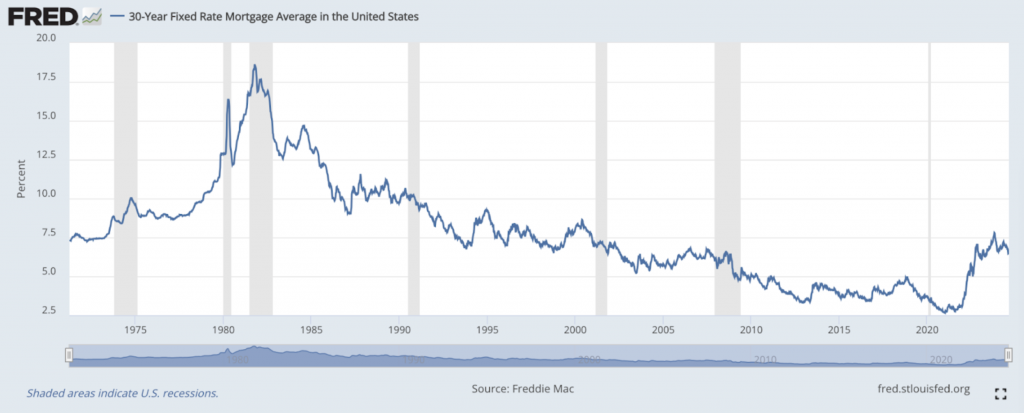

Come on. I’m super excited. We haven’t done one of these in a while. I’m really excited to engage our audience and our community, and I really appreciate everybody tuning in. 06:00 p.m. Asia. Time to listen to this presentation. There’s a lot of information you read in the news. Interest rates have been coming down. There’s a lot of reasons on why that is, but the bottom line is they have come down. So, to the extent that you are looking to potentially buy real estate or invest in us real estate, you want to get an update on the key factor in that decision, which is the cost of funding. So, looking forward to kind of discussing that as we speak. So, let’s get started.

06:09

Donald Klip

Yeah, so how this webinar will go is we will talk about the recent, big updates that we have for America mortgages, and then we will discuss the recent rate drop and why and sort of our outlook on what’s going to happen with the US real estate market. And then we’ll do our normal going over the loan programs, and then we’ll have a question-and-answer session. So, during the process, if you do have any questions, please put them into the chat and we will answer it towards the end. One thing as well, if you want to use our new platform, which we will discuss shortly, you can apply for a loan directly through the chat, or you can arrange a time to speak with one of our loan officers.

07:06

Donald Klip

Our loan officers are based all around the world, and it is literally a 24/7 schedule. So, with that, Donald, let’s start. I shall, yeah, let’s do it. Can you say that? Okay.

07:24

Speaker 3

Yep.

07:25

Donald Klip

All right. Okay. So, US mortgage loans for international clients, that’s what we do with America mortgages and global mortgage group, as everybody is probably aware, our big updates. So, for, so for the loans in general, we have seen a decrease of at least 1% across the board. So, Donald, I know were talking about this earlier today in the office. Now, if you look at where were pricing foreign nationals, for example, just two weeks ago, they were around eight and a half percent. And I think today we price something out in the very high six s, which is absolutely amazing. Okay. One of the other updates we have is that we used to have, when we first started, a minimum loan amount of 150,000, I’m sure you remember, and that has been a consistent request for our clients.

08:51

Donald Klip

So we’ve recently been able to reduce our minimum loan amount to $75,000, which is huge for a lot of our investors that own a lot of smaller properties. So now, with up to 75% financing and a reduced loan amount of $75,000, Donald, I think we’ve really made it so that almost anybody can be a real estate investor. I don’t know if you have anything you want to add on that.

09:27

Speaker 3

No, the lower loan amount has really opened up opportunities in some states where the cost of the homes is much cheaper. And that makes it very attractive for a real estate investor. If you’re investing your disposable income, obviously, you could buy some stocks, you could buy some crypto. But if you wanted to buy a home, for example, in Manhattan or Los Angeles, it’s hard to come up with a million dollars for a 50% loan-to-value on a $2 million home. However, there’s a lot of growth opportunities in the Midwest, for example, in Ohio and Michigan, and those loan amounts are smaller. So, this lower loan amount allows an entry point for a bigger and wider audience who want to take part in this amazing investment opportunity, which is us residential real estate.

10:22

Donald Klip

Excellent. Well stated. So, I’m sure a lot of people are aware of our interest only program. I think this is one of the key features that we have as a company that is super attractive when it comes to investing in us real estate. And just to cover it a little bit, our interest only program is a fixed rate for ten years. Now, that ten-year fixed loan, you’re only servicing the interest for that ten-year period. After the ten years, that loan will not reset. It’ll stay at that same rate. But now you’re paying principal and interest, so you’re looking at a total 40-year tenure. And I think what makes it super attractive, especially as rates come down, you’re really going to be able to take advantage of the yield of a property.

11:21

Donald Klip

And you assume after the ten-year period, when that rate converts into a principal and interest, 30 year fixed, your rental rates are going to be significantly higher. Wouldn’t you agree, Donald?

11:35

Speaker 3

Yes. The purpose of real estate investing, or investing in general, is to maximize your cash flow. And so, if you can have ten years where you’re not paying principal and just paying the interest, it means for those ten years, you are maximizing your cash flow opportunity, that is rental income for those ten years. Now, obviously, in ten years, the property price is going to go up and it allows you more financing options down the road. But if you’re strictly looking at earning as much rental income as you can over a period of time, this is the best option.

12:11

Donald Klip

And I think one thing that also makes it very unique, too specific to the US, is there’s no age restrictions. So, whether you’re 19 or 99 in the US, they feel you should all have the same opportunity when it comes to housing, which is considered also for the mortgages. So, no age restrictions, as in most countries, you know, it’s going to be either limited to a specific age or to a working age. So, it really makes it fantastic. All right, the next big update. And this is something, again, much like the reduced loan amount we’ve been getting requests on a regular basis. And that is if you buy a property, you renovate it and you improve the value significantly. We used to have to wait six to twelve months before we would use the new appraised value.

13:09

Donald Klip

We’re really excited to announce that we reduce this to only three months. So, I think, Donald, you have a very good example of this for clients out of Singapore, so maybe you can give a little explanation on that.

13:25

Speaker 3

Yeah, I think for those of you out there, these sophisticated investors, which is our audience listening right now, you will likely have stumbled across an investing technique called the BrRr method, which is buy, renovate. Let me get this right. It’s bought, renovate, refinance, rent out, and repeat. And what that means is you buy a home that’s undervalued. Let’s just, for example, in the neighborhood, it’s 250,000. You see a home that’s worth 150,000, you go to Home Depot, you engage a contractor, you spend ten, $20,000, and once you’re done, it actually is worth $300,000. Now, historically or previously, up until now, you would have to wait six months before you’re allowed to refinance. But now, as soon as it’s done, we engage in appraiser, and that comes out at 300. You can refinance 70%, 75%, even 80% as an expat of the new value.

14:24

Speaker 3

So you pull out the equity of the increased value, and that can be done ASAP. So, the time in which you can execute these type of strategies has now been reduced to zero previously six months, and anything can happen in six months, and that ties up your capital for six months as well, as opposed to using it to make more money.

14:47

Donald Klip

We still have a minimum time that needs to be waited, which is three months, But we’ve reduced the time by half. So, it’s absolutely fantastic. Everybody is probably already aware that we have common sense underwriting when we do our loans. I mean, you know, specifically what that means is instead of asking you for your tax returns and your pay stubs and your end of year statement, or w two, or whatever it may be called, we are only qualifying the rental properties off of the rental income. I mean, if you think about it just makes sense. Sense. This is something we’ve been doing for a while, but not everyone is aware of it. So, we talked about this the other day on our group loan officer call, Donald, and I think you brought something up about what’s needed to qualify for this.

15:49

Donald Klip

Is it a one to one or what specifically are we looking at?

15:54

Speaker 3

Yeah, you know, I think, you know, the audience, once they contact us to learn more, they’re going to be really surprised and impressed on how easy that we’ve made this foreign nationals looking to buy property for investment income. So, the way this works is, you know, we, you know, like any purchase or refinance, we will have to, you know, you will have to. There will be an appraisal that will be conducted along with a rental comparison. And what that means is if the rental comparison comes in at, let’s just, for example, say, 2000, and your mortgage and mortgage related expenses comes out at 2000 or 1999, you qualify. It’s not based on, like Robert said earlier, your pay stubs, your human resources need to write you a reference letter. All these things that typical bank loans require; we don’t need them.

16:55

Speaker 3

And it makes it easier for our clients, which are all outside the US, because sometimes there’s different, there’s time zone issues, there’s language issues. And so, we’ve made these. We specifically created these to make it easy for our international clients to qualify when they buy property in the US.

17:15

Donald Klip

Yeah, it’s actually a fantastic loan program because besides the reduced loan amount of $75,000 and not having to have us credit, being able to qualify just strictly on the rental income really makes it to where almost anybody can be a real estate investor. Build your portfolio, and for the future have passive income. The biggest update that we have, and something that Donald and I and our entire team has been working tirelessly for more than a year, is the launch of Morty AM. Morty AM is our mortgage application platform. Now, what this does is it allows you to get a pre-approval and often less than 24 hours. This is an online application, but it is also available within two weeks on the Apple and the. What’s the other one?

18:24

Speaker 3

Android.

18:28

Donald Klip

It’ll be easily downloaded, and you will have access to this anytime you want to buy a loan. You get a pre-approval, you get it into the system. You’re talking to a realtor, maybe they’re somewhere in some country and you can zap them that pre approval letter. So, it’s a really slick program. The application itself, it’s really simplified. I don’t know if, Donald, you want touch on anything about, especially how we really worked. Very difficult to, I mean, in a very diligent way, to make this application applicable to our foreign clients.

19:08

Speaker 3

Yeah, everything we do for our clients. We created this to fix a problem. We’re a small company trying to fix a big problem, which is trying to get access to us mortgages while living overseas. So, we hear our clients, we hear the feedback. And what we’ve heard is that the world is ready for a digital solution. The world is ready to, you know, for certain aspects of a mortgage. They’re ready not to speak to somebody, obviously, you know, the initial call and the follow ups and, you know, the urgent questions, you know, we’re here for you, but a lot of the manual, things such as, you know, you know, uploading financial statements, things that, you know, that can be on autopilot through this software, just makes the clients lives a lot easier.

20:03

Speaker 3

And you could do it at your own time, as opposed to sometimes you get an email from a loan officer and forget, and you go to work and you kind of miss a day here and there. Here it’s all online. It’s, you know, you, you know, it obviously sends you reminders, but it allows you to. It allows the process to be a lot faster than normally it would be when you’re dealing with a financial institution back in the US.

20:32

Donald Klip

Yeah, I mean, I think with this launch of this program, we’ve made our services even more valuable than most of the big banks. So, it’s really fantastic. And if anybody wants to download the application or actually right now, it’s more of a link to the web portion of it. You can scan the QR code that is on this page here. So, we will go to the next page. Okay. More big updates. As everybody is aware, because all of our clients are living and working abroad, we understand that they don’t always have the ability to search for services or providers which you may have ready access to if you were living in the US. So, we’ve made it very simple.

21:33

Donald Klip

We have on our website in the middle section, our concierge section, and on that you can do everything from setting up an LLC for your company to own the property, to streamline your insurance with prime insurance coverage, to even getting the best rates on FX exchange when you need to move your money per se, of a down payment, to being able to provide proper and adequate property management solutions through a company similar to us that only focus on foreign nationals. So, another big update, and again, this comes from a lot of requests for our clients. We get clients all the time that get pre-approved for a loan. But once they get pre-approved for a loan, they don’t know where to find a property, or they’re not really sure where to find a property.

22:34

Donald Klip

So Donald has actually been the driver on the real estate portal. So, Donald, why don’t you tell us what we’re looking at and what our clients should be expecting?

22:47

Speaker 3

Yeah, so I don’t want to spill. I don’t want to, what do you call it? Unveil sort of the surprise. But I need to plug a report that we will be publishing very soon, which is, this ties into what you just said, which is we analyze the price per square foot for every major city in the US and every major global city. And we also analyze the rental yield in every major global city and the top 100 cities in the US based on population. And the reason why I say that is because once on your real estate journey, everybody has different criteria on where they’re looking for. Is it close to my relative? Am I going for pure, the highest return? Or it needs to be near an international airport or needs to. We all have different criteria, but finding the properties is difficult.

23:36

Speaker 3

So that report is going to help you narrow down your search. It’s never been done before. We’re the first ones in the world that will be able to do this. So, keep your eyes out for that. And that leads into this portion, which is when our clients use us to get a pre-approval. First of all, you need a pre-approval to buy a property because sellers won’t sell you the property unless they feel comfortable that you have financing behind you. But being able to offer carefully selected and curated property that meets the needs, price point and logistics of our international clients is very valuable. And one thing, I’m going to talk about this in the upcoming slides, but there is a six to 7 million home shortage in the US. That’s why it makes.

24:30

Speaker 3

I don’t want to pre-empt sort of my portion of the presentation, but getting property to be sold is like gold dust. So, we’ve been trying for a long time and so we’ve been able to secure homes just outside of Dallas, Texas, which is a really amazing location for gentrification. A lot of people working from home. But anyhow, I want you to contact us. We’ll give you the details for that. The website is the link is up for the properties that we have available to sell. These are new properties. They come with property management. They’re amazing. They fit the price point for our international clients. So, we will, when we send you a thank you letter, we’ll add the link to that email. So, keep an eye out for that along with the research piece that will be coming out very soon.

25:18

Donald Klip

Yeah, I’m very excited about it. I know. Again, it’s just like all of the things that we work to improve or to fix this has been a huge contention for a lot of our clients. So, with that said, we will, Donald will discuss, is this the best time to invest in us real estate? And really, here is why.

25:42

Speaker 3

Thank you, Robert. That was a fantastic presentation. I’m going to talk about really quickly the current supply demand landscape of the US. I know you read a lot of things, maybe in the media, India, a lot of it is true, but a lot of it is not understood why. Now, interest rates have gone up a lot, but if you can believe it, home prices in the US went up 8% last year. I mean, that’s unbelievable. Interest rates went up 400% and property prices still went up. Now, I’m going to address this in kind of a systematic format, which is supply and demand. So currently, over the last ten years, there have been 5.5 million households formed versus homes built. That means there’s five to 6 million more homes, households that have been created versus homes that have been built.

26:35

Speaker 3

And like it says, so there’s a massive shortage, which you’ll read everywhere when you’re doing your research. Now, those are new homes. Now, existing homes, which is about 90% of, you know, kind of the transacted homes, 80% of the folks that have mortgages, 80% of those mortgages are fixed for 30 years under 5% and 40% are fixed for 30 years under 3%. Sorry, that’s a typo. Under 3%. So, what that means is that it’s kind of put this supply grip on the market. And so, if you think about it, what happens if new homes are being built? And this is also why it’s been really difficult for us to get new homes to bring, to show our overseas clients, is that as soon as homes are built, guess who’s buying them?

27:31

Speaker 3

The average person may not be able to buy them at 8% fixed for 30 or 7% fixed for 30, but institutions can, right? And this is their playbook. They try to buy as much supply as they can because they know the supply demand is imbalanced. They control pricing. And this is no secret. You can google institutional buying of single-family homes in the US and you will see what’s going on. Like any smart investor, it’s a lot better if you invest alongside smart people. And we think the folks like Blackstone and American homes and these type of landlords that you see are fairly smart. So that’s happening now. Next slide. Now what’s happening with demand? Now, what happened with COVID was that people worked from home, they went from.

28:22

Speaker 3

It was always kind of growing at 2.5% a year, so it was heading in that direction. But during COVID overnight it went to 100%. And I think a lot of companies realized that there actually is a portion of. Of work that can be done at home. And I think that’s allowed people who lived in different states to move to find work opportunities in other areas easier. Now, the US, it’s a lot of things, but in terms of its ability to gentrify is without a doubt the best place in the world. If you can’t afford to live in California, which many can’t right now, you can rent a U Haul and move your family to Texas, which a lot of people are now, and make a living.

29:07

Speaker 3

And you look at what’s happening in the US right now is a lot of the coastal states, specifically California and New York, a lot of these big companies are created there. Facebook, Amazon, you name it, Tesla. And they become so big that folks can’t afford to live there. So, companies move their headquarters to Texas to low or no tax states. And that’s happening end masse. And that’s driving the demand to rent homes. And you’re seeing that now. In fact, Dallas is the headquarters for the most fortune global Fortune 500 companies in the world. And coincidentally, I don’t want to plug our property again, but the new homes that we’re offering at the moment is 40 minutes away from Dallas. So really want to show you those homes when we get a chance. Next slide. So, this is really eye opening.

30:05

Speaker 3

So if you look at the G seven countries, I mean, this is just a select a number, the rental yield, and this is cash flow received from rents, it’s really low. In fact, I would argue that you cannot make money of renting homes anywhere in the world except Dubai and the US. Now, if you look at the average rental yield in the US, it’s 8% at the moment. Now, if you take out California, New York, that actually turns out to be twelve to 15% gross yield. It’s really hard to believe, but it’s true. And there’s just lack of information in the world about this phenomenon. So, if you are sitting in these countries where you’re making a good living, a good income, and for example, in Singapore or Hong Kong, where I’m from, getting in the real estate market is really expensive.

31:01

Speaker 3

It’s minimum, two, three, four, $5 million. Whereas in the US, you could play this game with 100, $150,000 and enjoy 15% rental yields. Now, there’s obviously a lot of things that you need to learn, but like anything in life, you’ve put in the hard work, you reap the rewards. This is just a snapshot. In fact, I would argue that this is a little outdated. The numbers are even slightly higher at the moment. But you can see this is not to say that you should rush out and buy a home in Detroit or Milwaukee or Omaha, where actually Warren Buffett is from, but you look at places like Ann Arbor, a huge college town. University of Michigan is there. You look at Las Vegas. It’s the center of all convention business in the US at the moment.

31:50

Speaker 3

Atlanta, the home of the busiest airport in the world. Each one of these cities represents a different thematic. And look at the gross yields. This is one of the biggest surprise slides that when people see that, they go, oh, my God, why didn’t I not know about this? But now you do. And now with leverage, you can take advantage of this. So that’s my bit on the market. I will hand it over to Robert to go into our loan programs and then towards the end, open it up for Q and A. And I look forward to that.

32:24

Donald Klip

Thanks, Donald. I think too, going back to just say the yield slide that you are showing, if you look at what the general yield is in the US, say 5% or less, that is taking into account the coastal states such as California and New York. But if you were to take those out of the picture, these are actually what people could potentially be looking at. And as you said, and because we do loans, not just in the US, but all around the world, we really understand this probably better than any other country or company that are offering mortgages. Okay, so let me give a general overview of the mortgages that America mortgages offer. Now, again, 100% of our clients are living and working abroad, but obtaining us mortgages, whether for purchase, refinance or cash out.

33:28

Donald Klip

I think as we’re seeing interest rates go down, we will see people just refinancing, not pulling cash out, but merely just to reduce the rate. So, if you’re a foreign national, you are able to get up to 75% loan to value in all 50 states. If you are a us expat, we try to make it exactly as if you walked into a bank in the US and you were living and working there. And for an investment property, you can get up to 80%. Something very unique to us mortgages. Again, there are no age restrictions. So, I always like to say, whether you’re 19 or 99, you still have the same mortgage amortization regardless of the age of the borrower. We discussed what ten-year interest only loans are absolutely fantastic.

34:24

Donald Klip

If somebody wants to maximize yield and lock in a rate to where they don’t ever have to worry about refinancing again, unless they choose to. We qualify on the rental income of the property for investment properties. It makes it a very simple, clean, easy way. We don’t care if you are self-employed or you are employed all we care about is the cash flow of the property, which again, is common sense underwriting and just makes sense foreign income. If you are, say, a US expat or you want to qualify using your income, we absolutely allow it, because again, this is all we do, all we deal with. It’s very common and very normal for us. Again, these are loan programs for non us residents, whether you are a non us passport holder or you are a us passport holder living overseas.

35:30

Donald Klip

What also makes these programs very nice and why we have a lot of business which is referred to from private banks, is all of this is dry lending. And if you’re familiar with lending in Europe, most lending requires the borrower to open up some sort of account with the bank that they’ve got a mortgage with a minimum deposit. We have no requirement for that. This is pure dry lending, meaning there is no requirement to open up a bank account with that lender. A loan process in general, once we get your application, we’re looking at 72 hours for issuing a pre-approval. With the launch of Morty, we can actually reduce that to 24 hours, if not sooner.

36:25

Donald Klip

Our average closing time is 30 to 45 days, and you can sign your closing documents in your home country without ever having to leave to travel to the US. So basically, you can start the application online through Morty, and you can close even at your local notary, depending on the country that you’re in. What makes us also very unique, and a lot of it has to do with qualifying off of the rental income of the property is 97% of the applications that get submitted are approved. It’s a number that we’re super proud of. And it’s something that if for some reason the loan isn’t approved, it’s normally property related and not really related to the borrower. Again, and this is in the chat link for everybody to work with.

37:22

Donald Klip

We have 24 hours a day, seven days a week loan officers all around the world. You speak, or you’re more comfortable speaking another language. There’s a variety of options, which, when you’re choosing a calendar time, you can click if you would prefer to speak Spanish or Chinese or whatever it may be. So, I’ll just go over a couple of the loan programs quickly and then we’ll get to the questions and answers. So, our most popular loan program is the America mortgages rental coverage plus loan. And this is something that Donald and I had talked about earlier in the webinar and what I had just gone over. This is the loan program that everybody loves. It requires you to submit no personal income. So, whether you, again, if you’re self-employed or you’re employed, you don’t show maybe your true serviceability of income.

38:19

Donald Klip

This allows anybody to still be a real estate investor. If you’re a foreign national, you can get up to 75% financing and a US expat, assuming you still have us credit, you can get up to 80%. No us credit or residency is required. It’s a very fast, simple loan program and the loan amounts are as low as $75,000 and can go as high as 3 million. Again, we offer on these programs 30-year fixes, interest only. If you look at how this loan qualifies, it’s on the bottom of this slide and it’s a very simple process. If the rental income covers the mortgage, taxes and insurance, the loan is going to qualify. So, it’s very straightforward. In the event, say that the rental amount does not qualify, it does not mean that the loan is not approved.

39:18

Donald Klip

It just merely means that maybe you have to bring in a little bit more money to be able to get that number to work. Next program is our expat program. If you are a US expat and you’re living abroad and you have gone to your local bank or one of the big banks that are well known, you will find out that you’re going to get halfway through the process before they realize that you’re earning your income in euros or in yen or whatever it may be, and they’re going to say, I’m sorry, we cannot do your loan. Well, again, because 100% of our clients fit this box. We’ve made sure that all of the loan programs that we have are specific for our clients living globally.

40:11

Donald Klip

If you’re a US expat, we allow foreign income, we allow your bank account to be in a foreign country, and there’s no requirement to provide a w two. That is huge. The only real, I guess, caveat on this is you still need to maintain us credit with at least a 646 80 credit score to qualify for this. The minimum loan amount is $150,000 and we can go all the way up to 5 million. This works just as it worked when you were living and working in the US, where it goes on your debt-to-income ratio. We have a debt-to-income ratio of 43%.

40:55

Donald Klip

So in this example, as long as you’re making $10,000 a month, and that is your gross income, not your after-tax income, and the mortgage payment, taxes and insurance are at least 4300 and below and including any other debt that you may have in the US, your loan is going to qualify. So again, we try to make this with the same rate, the same terms and the same programs as if you were living and working in the US. Absolutely fantastic program. So that’s it for our webinar for today. This is our contact information for our office in the US, as well as our office in Asia, where Donald and I are both based.

41:42

Donald Klip

You can click on, or you can scan the QR code, which is on the right hand side, that will link you directly to a WhatsApp messenger where you can reach out to one of our loan officers, ask a question about a loan, or even get the direct link for Morti to apply for a loan. Again, we have a link within the chat that allows you to schedule an appointment with a loan officer 24/7 or if you want to, you can go online and apply directly through mortgage. So, let’s get to the questions, Donald, and let’s see where we are at. So, what I’ll do is I’ll ask the questions and then we can both kind of enter and see where we go. So, first question is, what is the likelihood of being approved? Donald, do you want to take that?

42:41

Speaker 3

Yeah, I mean, the short answer is highly likely, you know, depending on what loan program you’re seeking. But as with regards to specifically the loan program that we mentioned earlier, which is based on the rental income of the property, you know, when you’re doing your research, you have a pretty good idea of what the rents are, right? You speak to you, you look on Zillow or Redfin, you speak to your realtor. So, you can do the math. And you just need a few documents to get a pre-approval with us. Robert, you want to talk about what kind of documents are actually, this answers the next question as well. What kind of documents you need to get a, a pre-approval.

43:25

Donald Klip

Yeah. Fantastic. So, to get a pre-approval for the loans, it is about as straightforward as you can get. Assuming you’re a foreign national, you’re just going to need your passport. And this is, again, on our portal, you can securely upload everything. So, there’s no security issue or trust issue on this go through, you can complete the loan application. And really the biggest concern or the biggest hurdle that most people have is the down payment for the property. So, we need to see for AML purposes that any money that is going to be used in the transaction has been in your account.

44:07

Donald Klip

It can be in the US, it can be overseas for a minimum of 60 days if you’re fine with that hurdle, then once you submit all the documents, your loan officer will review it along with the application, and we can issue a preapproval in 24 hours. Next question.

44:27

Speaker 3

Rates have come down, but will they stay down? Well, that’s a crystal ball question, but I think I could take a stab at this. Rates. I think we can all assume that rates will be cut. And these are fed fund rates now, will they stay down? I can’t see them going up. I think inflation print just came out overnight and they look like inflation is coming down. So, there’s more room to move the rates down, but who knows? But I would have to say over the course of the next few years, I can’t see rates going up, either staying flat or coming down, which is really good for being a property investor.

45:14

Donald Klip

Absolutely. So, okay, next question. What would cause a loan application to be rejected? Well, I think there’s a couple possibilities, is if you’re a us expat and say, maybe you don’t have sufficient credit, that could be a reason. Or maybe your debt to income doesn’t work. But we do have loan programs that will help you with that as well. For us in general, normally it’s not about does the loan qualify or not? We qualify 97% of our loans. It’s really, does the rental income cover the mortgage payment? And again, with that, it doesn’t really mean that the loan doesn’t qualify. It maybe just means that you have to come in with a bit more cash. Okay, next question. What is the most popular loan program in American mortgages? Funny, because that is exactly how I introduced that loan program.

46:12

Donald Klip

That is our rental coverage plus. And again, if we go back to the question about what causes an application to get rejected, this is the most straightforward, most common-sense underwriting loan program that you have where you’re qualifying off of the rental income and not the personal income of the borrower. Next question. Hey, great presentation. Which banks do you work with for underwriting and disbursement? Let me jump on that, Donald, and then maybe you can add something. But last December, we actually became a direct lender ourselves. So, we are able to lend in our own name, which makes it fantastic because we have a lot more control over the loan programs. Now, when it comes to loans that maybe don’t qualify for our own lending, then we have a variety of options.

47:07

Donald Klip

These are banks that likely you have never heard of, but banks that we’ve curated over the years that understand our clients being foreign nationals and expats.

47:20

Speaker 3

Yeah, maybe I’ll add a little bit of. A little bit here. So, it’s, you know, we’re preconditioned to think, well, most of us are not you and I, but most people in the world are preconditioned to think mortgage. They think banks. However, in the US, most and the biggest mortgage lenders are not traditional retail banks. I’ll give you an example that everybody knows. Rocket mortgage. Rocket mortgage is the largest mortgage lender in the US. But they’re not a bank. They don’t take deposits. And these are called wholesale lenders. So, these are the type of lending institutions that we work with. And we are one ourselves, as we are a lender ourselves as of December last year, which is great. So, this makes, you know, American mortgages is the only us mortgage broker outside the US. We created this process. We are the global leader.

48:20

Speaker 3

And just like, I guess, many restaurants like to use farm to table, we want to move higher up the food chain. So, we’ve become a lender so we can give you the type of service, pricing, transparency and accessibility that our clients need, deserve and want. So that’s a little bit of background on kind of our journey to becoming our own lender.

48:41

Donald Klip

Perfect. And Raul, to answer your question again, we don’t use a normal bank, even for us citizens. We’re going to use a bank that understands you as a borrower. So, it’s what we do is unique, and it really works when it comes to earning foreign earned income. As an expat, which I’m assuming you.

49:05

Speaker 3

Are, I’m going to give a quick anecdote to our audience, and I think folks in Hong Kong can empathize with this. We had a client recently call us and said that their loan got rejected because they could not put a zip code into the little box that says, what’s your zip code? Because Hong Kong doesn’t have any zip codes. And just because of that, they couldn’t move forward with their loan. Now, this is just a microcosm and a small sample of the issues that we’re trying to fix. And, like, we know the cultural and country idiosyncrasies of folks living outside the US. And this is just a funny example, but it’s true. And it happens all the time, but not with us, because all we do.

49:53

Donald Klip

Yeah, absolutely. I would probably say 20% of our business is expats that were going through a major bank in the middle of a purchase to have their loan officers say, oh, I didn’t realize that you are earning foreign income. So. Okay, next question. Can a loan commitment be less than 30 years, if you choose. Absolutely. If you want to have a 15-year term, that’s your option. In general, our loans are 30-year fixes just because people want that safety and that security. But if you want to pay your loan off or make double payments or even have a reduced 15-year term, that’s absolutely fine. Again, we just, if you’re qualifying off of the rental income, you know, when you shorten the amortization, that could be an issue, but is absolutely perfectly acceptable. Next question.

50:45

Donald Klip

How do we make sure that the rental price, I’m assuming this means, is accurate. And that’s a super good question. And I think we receive this every day when we order the appraisal or the valuation, depending on the, depending on where you’re living, we order a supplement to go along with that. That supplement tells us exactly what the average rent is for that specific property, and that’s the number that we use to qualify. So, it not only protects the lender, but it also protects yourself to making sure that this is the type of rent that, you know, you’ve been told by the realtor you’re going to get. Next question. Do your loans have unit count Max or minimum? I’m not exactly sure what that means. Donald, do you have an idea?

51:38

Speaker 3

Yeah, so I think it’s the number of doors per loan. I think you’re going to be more of an expert on this, Robert. But I think the per loan, the number, I think it’s a four-unit max for four door max on some of our loan programs. I really should get more involved in the loans, but I apologize. I believe that’s what this.

52:06

Donald Klip

Okay, so, yeah, if that’s what it means. So, a one to four unit, we can qualify technically as a single family. So, you have the same LQB options that’s available. So, thanks for the explanation, Donald. Next question. You mentioned that you qualify most of your borrowers, and usually the properties fall down to a 3% rejected application. Could you give us an example of the type of properties that you will not finance? Again, very good question. If you look at, say, exactly in New York has a lot of co-ops, very difficult to finance. We won’t do rural properties. So, properties that are quite far away from the city center, and we really will stay away from mobile homes or manufactured homes. Otherwise, it’s an open market.

53:04

Donald Klip

You find a property that you love, you want to be able to finance, you know it’s going to get fantastic rent a, give one of our loan officers a call and run it by them. They’ll tell you immediately if it’s going to be possible. Yeah.

53:15

Speaker 3

And one thing, you know, one thing that, you know, part of that 3% that were not approved, a lot of that has to do with the property that you may have missed when you. When you. When you. When you view the property. You know, for example, in San Francisco, there’s, you know, part of the appraisal is looking at asbestos, which is in between walls, which there’s no way you would be able to see that. So, in different cities, they’ll look at different things, you know, the structure wise or what’s in the walls or maybe holes that you didn’t see, and they don’t pass the appraisal process. So, a lot of times it has to do with the specific property, not actually you as a borrower. So that’s really important to say.

53:57

Donald Klip

Yeah, absolutely. Okay, next question. Some investor loans that fall into the better financing deals have a four-unit max. So, this is actually a really good question. In general, our very vanilla loan, especially the loans that we offer ourselves, are one to four units. So that is, we can do that every day. However, we also have loan programs that are for five to eight units. So, if you see something that, you know, it’s a fantastic loan, we can still qualify our fantastic property. Sorry. We can still be able to provide that loan for that up to 75% loan to value up to an eight-unit property. Next question. Can I close my existing loan midway through the tenor and reset my rate? So, in general, an investment loan will have a prepayment penalty.

54:56

Donald Klip

So that prepayment penalty normally will be a decreasing amount, that every year will get less, but it is still there for investment properties. However, it does not mean that you cannot. If interest rates go down and you’re able to do a simple calculation of what the breakeven is, it doesn’t mean that you will not be able to refinance your property at any time. If you wait until the prepayment penalty is finished, certainly you can refinance it without any penalties into either a shorter loan or you wanna pay it off, or even a brand-new loan and pull cash out. Next question. In the last question of the night, what is the minimum down payment required to qualify for a loan? So, in general, it’s 25% if you are a foreign national with no us credit.

55:54

Donald Klip

If you are a us expat, then it is 20% with that. Thank you, everybody, for staying through this hour. I think when Donald and I were talking about doing this, were saying we’ll probably knock it out in 15 to 30 minutes. But as you can see, with a lot of involvement and all of these fantastic things that we’re able to offer, this ran a bit longer. So, Donald, do you have any parting words that.

56:23

Speaker 3

Yeah, listen, all I want to say is, I say this to clients, is, if you can make the numbers work now, they’re only going to get better because the cost part of your equation is going to go down, interest rates and the income part of your equation is going to go up, which is your rental income. And then after, because the property is increasing in value over time, which has been proven that at some point you can refinance at a higher rate and recoup some of your initial capital expenditure. That’s what makes us real estate, the game of us real estate investing, unlike any other place in the world.

57:04

Donald Klip

Refinance at a lower rate.

57:05

Speaker 3

Lower rate. Sorry.

57:08

Donald Klip

So, again, I think just to kind of, like, add to that, if you’re waiting for interest rates to hit the lowest p or the lowest point possible, you’re going to miss out on what right now is still a buyer’s market. So, we always recommend, get in there now, rates are still absolutely fantastic, especially if you lock it in long term, you do an interest only. So, thank you again, everybody. Thank you, Donald. And we will see you, I believe, in a couple weeks for the next webinar. Appreciate everybody’s time. Don’t forget, in the chat box, there is a link to either doing the application on Morty or to schedule a time and day to speak with a loan officer. So, thank you, everybody. Appreciate your time.

57:52

Speaker 3

Thank you, everybody. Have a good evening.

Disclaimer: This transcript is AI-generated, so kindly pardon any transcription or grammatical errors that may be present.