SINGAPORE, August 18, 2022 /EINPresswire.com/ — America Mortgages, one of the world’s leading global mortgage financing firms with a sole focus of providing market rate mortgage financing on U.S. real estate for non-resident real estate investors, today announced it has added a new Super Jumbo Preferred HNW Mortgage Program that features both fixed and adjustable rate mortgages (ARM), competitive rates, high LTV/LVR and loan amounts from $3 million up to $150 million.

America Mortgages’ new HNW mortgage program can be used for second home and investment properties in all 50 states. International borrowers can use credit and income from their home country to qualify. Robert Chadwick, CEO of America Mortgages states “What makes this program very unique is that the borrower does not need to provide personal income documentation. They can qualify using either their investment portfolio and or cash in the bank” He goes on to state “This is a perfect loan program for Private Bankers to use for their clients when their bank cannot offer a viable option, as there is no AUM requirements and no encumbrance of the portfolio or asset used to qualify for the U.S. mortgage.”

“A lot of our clients come from Private Bank or HNW real estate agents globally. It’s simple, they are looking for new solutions to help their HNW clients purchase, refinance or release equity without having to provide Assets Under Management (AUM) but also at very competitive rates” said Nick Worthing, Vice President, HNW Division at America Mortgages. “Our Super Jumbo HNW Preferred Mortgage program offers high LTV, attractive rates, fixed term interest only or 30 year fixed and ARM options to help HNW borrowers without a financial administrative nightmare to qualify. It’s literally the perfect U.S. mortgage solution for HNW clients. Period.”

For more information on America Mortgages’ HNW Super Jumbo Preferred U.S. Mortgage loan program, contact [email protected].

About America Mortgages and Global Mortgage Group

Founded in 2019, Global Mortgage Group PTE LTD [GMG], and headquartered in Singapore, is a full-service global mortgage financing firm offering mortgages for investment purposes in The United States, Australia, Canada, United Kingdom, Germany, France, Spain, Singapore, Hong Kong, Philippines, Thailand, Japan to name a few. For more information, visit www.gmg.asia or call +65 8499-3229.

Founded in 2020, America Mortgages, Inc. is a wholly owned subsidiary of Global Mortgage Group PTE LTD [GMG]. America Mortgages headquartered in San Antonio, TX, with sales offices in 12 different countries, is dedicated to providing U.S. mortgage options for non-resident Foreign Nationals and U.S. Expats. 100% of America Mortgages [AM] clients are living and working outside of the U.S. Both GMG and AM focus on building quality, long-term relationships with its partners such as Private Banks, EAM, Family Offices, Realtors and other mortgage broker located around the world by offering a wide variety of mortgage loan programs focused on specific markets with an exceptional client experience. For more information, visit www.americamortgages.com or call +1 830-217-6608.

Investing in the largest real estate market in the world – the United States – can be a fantastic way to create future passive income. If you’re a non-US passport holder (foreign national) or a U.S. expat living overseas (Singapore or Hong Kong, for example), you may find it can be very complicated if not impossible when looking for a mortgage loan to buy real estate in the U.S.. Even American expats returning home and buying property in America fail to qualify for a mortgage loan from U.S. banks. Mainly because they don’t have a credit footprint or earned income in the U.S..

Read on to discover how you can easily obtain a U.S. mortgage loan regardless of your passport or place of residence.

Meet the American mortgage loan experts right here in Singapore!

Creating a portfolio of real estate or a single property investment is a proven way to build wealth and pass down a legacy to your family. Asset appreciation, high rental yields, no stamp duty, low barrier to entry and a stable market are some of the factors that make the U.S. real estate market a fantastic investment.

However, before you go shopping for that new home with a pool in Florida or a penthouse apartment in Manhattan, the first step is getting a non-committal approval for a mortgage loan.

America Mortgages (AM) was set up in Singapore earlier this year to unlock the U.S. real estate market for buyers living outside America. The company is a subsidiary of Global Mortgage Group (GMG), the largest international mortgage ‘originator’ for U.S. real estate.

GMG was co-founded in 2019 by Donald Klip and Robert Chadwick, both ex-institutional bankers. The two Americans met in Singapore in 2018 and became friends. Robert’s professional experience was in U.S. mortgages, and he was a seasoned investor in U.S. real estate. Donald was a hedge fund manager and investment banker in Asia with global real estate investing experience.

As expats themselves, both Donald and Robert realised that obtaining a mortgage from a “traditional” bank in a country where you don’t live and/or hold a passport is frustrating and often impossible. This led to them establishing GMG. GMG now has loan options in the U.S., Canada, Australia, Hong Kong, Singapore, UK and various locations in Europe, to name a few.

How America Mortgages helps you get a mortgage loan in America

While GMG specialises in residential, commercial, construction and bridge financing in different countries, America Mortgages’ sole focus is providing market rate mortgages specifically for the U.S. 100% of their clients are either U.S. expats or foreign nationals living overseas. Due to a very focused expertise, AM approves 97% of loans submitted.

Here are the key highlights of a U.S. mortgage loan for foreign nationals and U.S. expats:

For a non-U.S. citizen: maximum loan-to-value (LTV) is 75% for purchase and 70% for refinance and equity release

For a U.S. expat: maximum LTV is 80% for purchase and 80% for refinance and equity release

Minimum loan amount of US$150,000 and maximum of US$50,000,000

Fixed term options of 5, 10 and 30 years

All loans amortised over 30 years, regardless of borrower’s age

10-year fixed interest-servicing-only payments available

Mortgage loans available in all 50 states

Self-employed and employed borrowers allowed

No U.S. credit or footprint required

So, whether you’re a global investor, buying a holiday home for yourself, an apartment for your child when they attend university or simply growing your investment portfolio to pass down to your children, it’s possible for you to buy property in America!

* Indicative values; rates are terms are subject to change

The biggest myth of buying real estate in the U.S.

Although AM suggests that buyers should get advice from their attorney or tax advisor on investing in any real estate market, the myth of the States being a highly taxed country for buying U.S. real estate couldn’t be further from the truth.

For one, regardless of whether you’re an American citizen or a foreign national, there’s no stamp duty when purchasing property in the U.S. There are also no government limitations or restrictions on when or where a foreigner can purchase or sell property in America. Since there aren’t any cooling measures, this means that savvy investors are able to take advantage of properly researched locations and asset types. Yields and appreciation galore!

America Mortgages has been featured in Yahoo! Finance, The Mortgage Daily, Canadian Business Journal and other notable publications for its open architecture approach as well as providing borrowers with access to both in-house AM and third-party solutions to make informed decisions.

The AM team says that it shouldn’t have to be confusing, overwhelming or foreign to obtain a U.S. mortgage to buy property in America; they have loan officers throughout Asia and around the world with the depth of experience and knowledge required for resolving complex issues foreign national and expat borrowers may have that U.S. banks and brokers don’t know how to handle.

Far from being on the outside looking in, now what real estate investors get is a front-and-centre window into the U.S. market. You can open and close a transaction all while sitting in your living room in Singapore without ever getting on a plane!

Hear from an America Mortgages client

“The service and personal attention that we received from Donald and Robert was exceptional. They were patient and took the time to answer all of our questions while leading us through the mortgage process. Everything was handled professionally, efficiently and faster than the service we usually receive from our banks. We will definitely recommend America Mortgages to our friends and colleagues.” – Janey Schueller, Singapore

As many of you know, America Mortgages offers two main ways to qualify to purchase or refinance investment real estate in the U.S. – either using personal income or using only the properties’ projected or actual rental income. For two main reasons, most of our clients use the latter. One, their income may be extremely complex or documented insufficiently, or two, they plan to move quickly with a streamlined, minimal documentation approach.

Difficult times call for creativity and common sense.

At the beginning of the year, qualifying based on rental income, otherwise known as DSCR was easy. Rates were low, rental yields were stable, and properties cash flowed on paper very easily. Since the beginning of the year, rates have continued to increase. Overall, rates remain historically low when you look at the U.S. mortgage market over the last 20 years. Rental yields have continued to climb to record levels, however, documenting these rental yields through an appraisal, which is how we underwrite these loans, has become increasingly challenging as there is typically a lag in rental comps to support the higher rents.

This presented our team with a problem; In the current environment, in order to qualify for a “standard” DSCR loan, clients were required to put more money down to keep the underwriting numbers in line. In general a DSCR loan requires the rental income listed in the appraisal to be greater than or equal to the mortgage payment. Unfortunately, it’s going to take time for rental appraisals to correlate with the higher rental yields, to where DSCR will be a viable option again. However, we have a solution…

Rejoice Global Investors…Introducing America Mortgages’ No-Ratio Mortgage Loans!

“No-Ratio loans,” have recently been introduced as options to help clients with minimal down payments to leverage a higher LTV without the constraints of waiting for rental yield to catch up. You might ask yourself – why would someone want to go into a loan knowing the property cash flow doesn’t cover the mortgage payment?

It’s a good question! This is common sense underwriting and as mentioned previously, the rental comps mentioned in the home’s appraisal sets the cash flow target. Rental comps are hard to measure; they are dependent on when tenants in your area have renewed their leases, are the renewed leases at market rent, etc. This measurement is often not the rental amount the client is buying the property for. It is very common to review an appraisal and see rental comps being used where rents haven’t been raised in years; this is likely because it’s a stable tenant, the landlord isn’t in need of maximizing the yield and prefers to keep a stable tenant – a problem when trying to get the maximum rental amount on an appraisal and a cash flow loan to work.

Here at America Mortgages, we put a lot of emphasis on figuring out the client’s plan for the property. How do the rental comps in the area look versus what their realtor believes they can rent it for? Are they buying for long-term rentals or short-term rentals? All of these questions plan into the type of mortgage program they will utilize – and now more than ever, it’s the no–ratio loan that allows them to avoid the hassle of counting on rental comps in appraisals and still put minimal down into the mortgage as possible – they also understand the ability to refinance the loan when rates improve in the future – which they will.

Bottom line, America Mortgages’ clients are sophisticated and seasoned U.S. real estate investor. Our U.S. loan officer based in 12 different countries know and understand the market. Better than anyone else. We listen to all our clients requests, and if possible we find a solution which fits the market and “makes sense”. No Ratio Mortgage Loans is such a solution!

Contact us today at [email protected] to speak to our team of U.S. mortgage specialists today!

The “Bizarro World” references Bizarro Superman, a supervillain who lives in a world where everything is opposite. Here’s a great explanation from the TV show Seinfeld.

This reminds me of the world we live in now; mortgage rates double in 10 months, and yet, rental yields continue to increase double digits, year-on-year.

I have been telling our clients over the past few months that it is a great time to be owning a home in the U.S. for investment income. Most of us have lived through a few economic cycles, and for most of my career, 30-year fixed rates were between 6-7%, which is when I got my first mortgage in 2006, similar to where rates are now.

However, back then, you owned homes almost as leveraged equity, not like what it’s meant to be, more similar to a bond.

When academics say real estate is an inflation hedge, that is a peculiar concept since we have not really seen any inflation since the 70s, so not many of us know what that means in real life.

Till now….

This world is very different. Good or Bad, the fact is that there are significantly more people who need housing, millennials are unable to afford homes, and the rising rates have squeezed out the marginal buyer, and all of the above need to live somewhere.

My colleagues hear me say this ad nauseam,

“We will be in a world where 30-year fixed-rate mortgages are 7%, but rental yields are 10-15% very soon”.

I will try to explain why in this report.

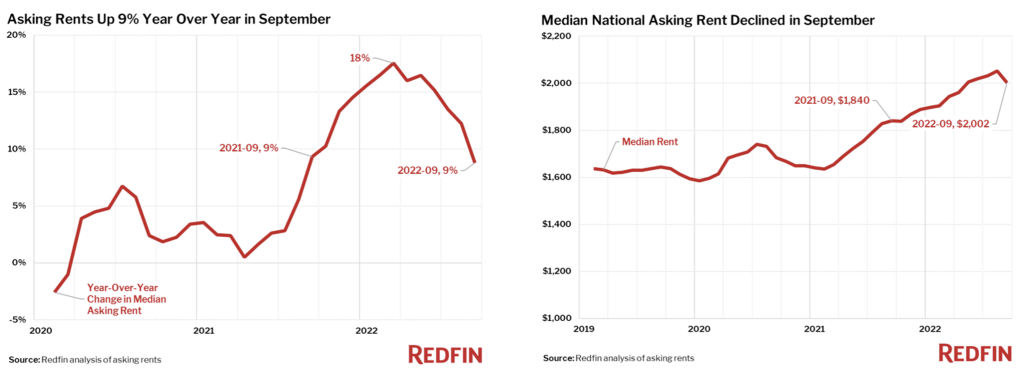

A few days ago, on October 13th, Redfin reported that the Median U.S. Asking Rent rose 9% year-over-year in September to $2,002, the slowest growth since August 2021 and the first single-digit increase in a year. Sure the article makes it sound bearish.

Wait a minute? (sound of car screeching on the pavement).

Mortgage rates have doubled since the beginning of the year, and yet rents are still rising 9% a year. (As recent as May, rents rose +18% year on year!)

While visually, it does look like rents are falling, but that was from an outlier peak of 18% in May….my personal view is anything that has growth in this world is POSITIVE!

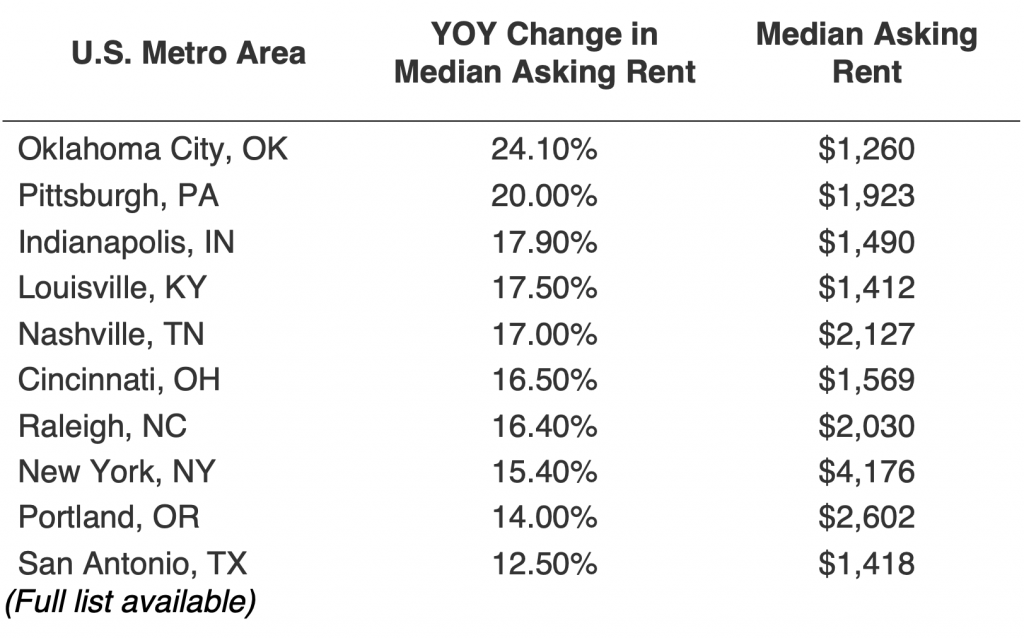

In some cities like Oklahoma City and Pittsburgh, rents rose by more than 20% year-on-year (not a typo). More below.

THE PROBLEM – HOUSING SHORTAGE

A housing shortage is not something you can really see. We hear it on the news or read it in the papers, and we think…how can that possibly be an issue.

Can’t homebuilders just build more homes?

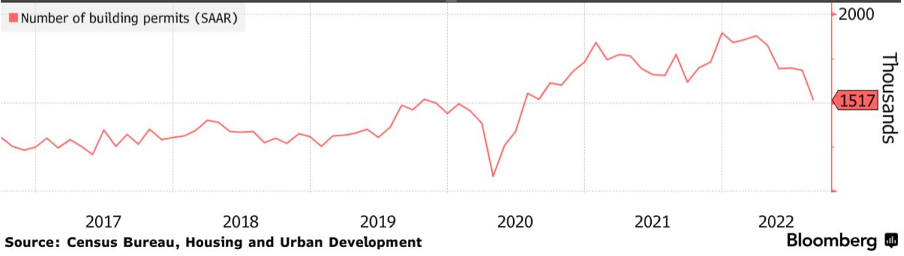

The NABM/Wells Fargo Housing Market Index dropped three points to 46 in September, the lowest reading since May 2014!

Meanwhile, “Application to Build” declined to 1.52M units, the lowest since 2020.

Number of Building Permits (SAAR)

One could also conclude with higher borrowing costs, homebuilders are discouraged from starting new projects, which is not helping the undersupply situation.

Another aspect of this is the financial incentive.

Like many other issues in the U.S. economy, there has been a focus on shareholder returns, dividends, share buybacks, etc., and hence the underinvestment in housing development since the Financial Crisis in 2008.

In fact, fewer homes were built in the U.S. in the 10 years following the 2008 financial crisis than in any decade since the 1960s! Think about that for a moment!

In the normal world, high mortgage rates tend to bring down values, and of course, there are some parts of the U.S. that are seeing a relatively faster decline in home prices, like San Francisco. I would argue that is city-specific, as the local economy hollows out and the homeless situation and cost of living is untenable for most.

Across the nation, there are indeed fewer sales and more price cuts on listed homes.

However, in this “Everything-is-weird” economy, the doubling in mortgage rates hasn’t caused home prices to fall as much as you would think, all things equal.

In fact, I really don’t think we are going to see any substantial collapse in home prices in the coming years because many owners bought when mortgage rates were low and can simply stay put through this phase of the economic cycle.

Also, there was less speculation, and investors put more equity in the properties during a time of tight supply. This will keep many families locked out of homeownership and forced to rent.

Here are some mind-blowing data points: Around half of all mortgages outstanding are under 4% fixed for 30 years, and about 40% of all homes are owned free and clear. Think about that for a moment!

Last month, Philly Fed President Patrick Harker discussed his recent research report with most major news outlets, “Unpacking Shelter Inflation”, September 2022, that the housing shortage is a key inflation driver. Read: “…housing shortage…”

In another research report by the Fed, “Volatility in Home Sales and Prices: Supply or Demand?”, Anenberg and Ringo, June 2022, write:

“We find that a 30% increase in the monthly number of homes coming onto the market would have been necessary to keep up with the pandemic-era surge in demand. Since new construction typically accounts for about 15% of supply, our estimates imply that new construction would have had to increase by roughly 300% to absorb the pandemic-era surge in demand. This is a very large, unrealistic impulse to housing supply in the short-run, suggesting that policies aimed at reducing bottlenecks to new construction would have done little to cool the housing market during Covid-19.”

Read again: “…new construction would have had to increase by roughly 300% to absorb the pandemic-era surge in demand.”

Here is yet another report, this time by Freddie Mac. “Housing Supply: A Growing Deficit”, Kater, May 2022. I give a little more weight to Freddie Mac since they are actually buying the loans. Their thesis is that:

“As of the fourth quarter of 2020, the U.S. had a housing supply deficit of 3.8 million units. These 3.8 million units are needed not only to meet the demand from the growing number of households but also to maintain a target vacancy rate of 13%. Between 2018 and 2020, the housing stock deficit increased by approximately 52%.”

Read yet again! “…U.S. housing supply deficit of 3.8 million units.”

I always take stuff like this with a grain of salt because academics look at things from a 10,000 ft altitude and through the lens of an Excel spreadsheet, but the gist is that every Think Tank in the world seems to claim there is a shortage of housing supply and since they have a few more tools (and PhDs) at their disposal for this that I do, I will take their conclusions at face value.

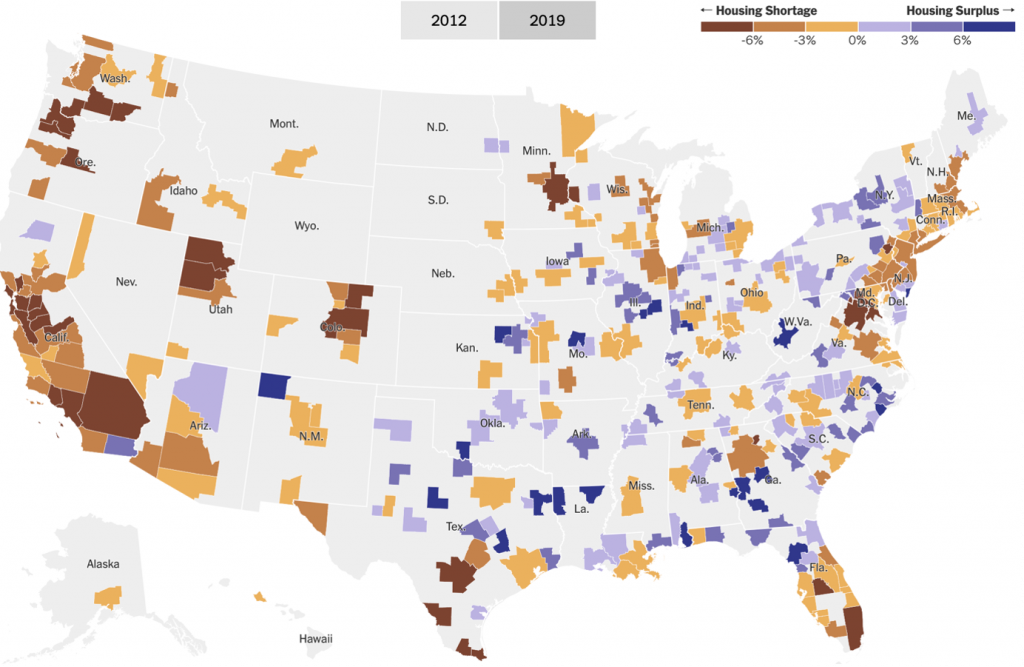

Here is a neat graphic from The New York Times, The Housing Shortage Isn’t’ Just a Coastal Thing Anymore” Badger and Washington, July 2022.

The Housing Shortage has Spread to More Parts of the Country.

Source: Up for Growth analysis of U.S. Census Bureau and U.S. Department of Housing and Urban Development data. Shortage percentages reflect estimated housing units needed to meet demand as a share of existing housing units. Metros with a surplus have enough housing for existing residents.

Let’s look at recent city-specific rental prices:

Top 10 HIGHEST Year-on-year Change in Median Asking Rent (%) *

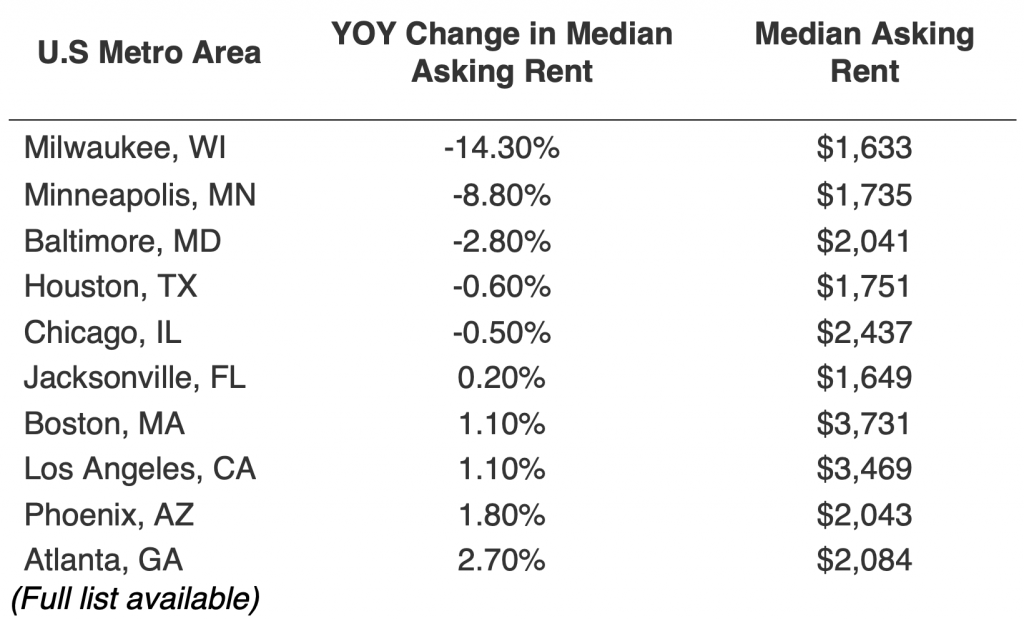

Top 10 LOWEST Year-on-year Change in Median Asking Rent (%) *

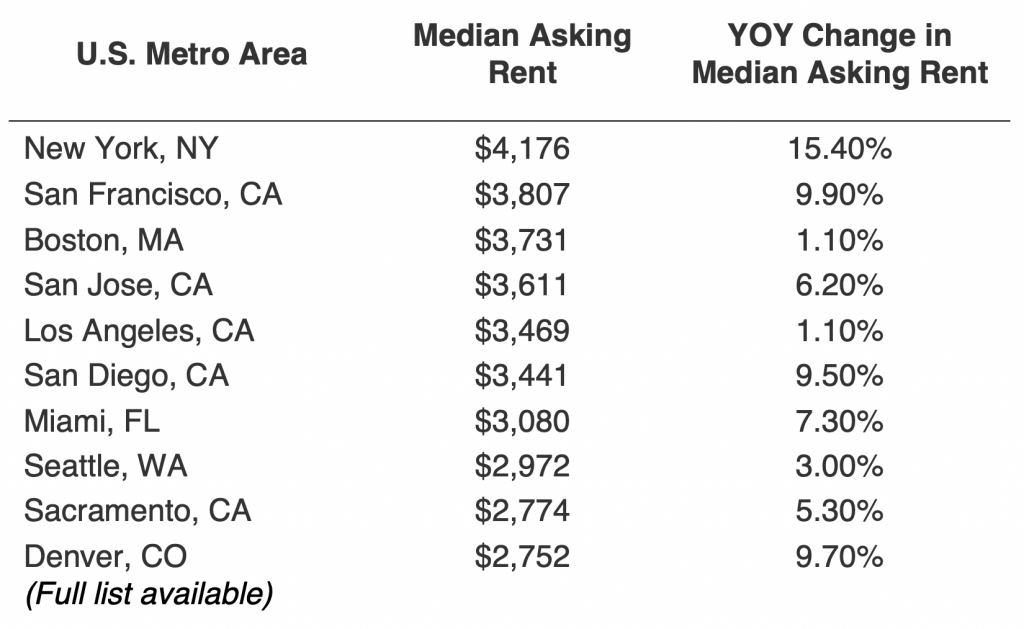

Top 10 HIGHEST Median Asking Rent *

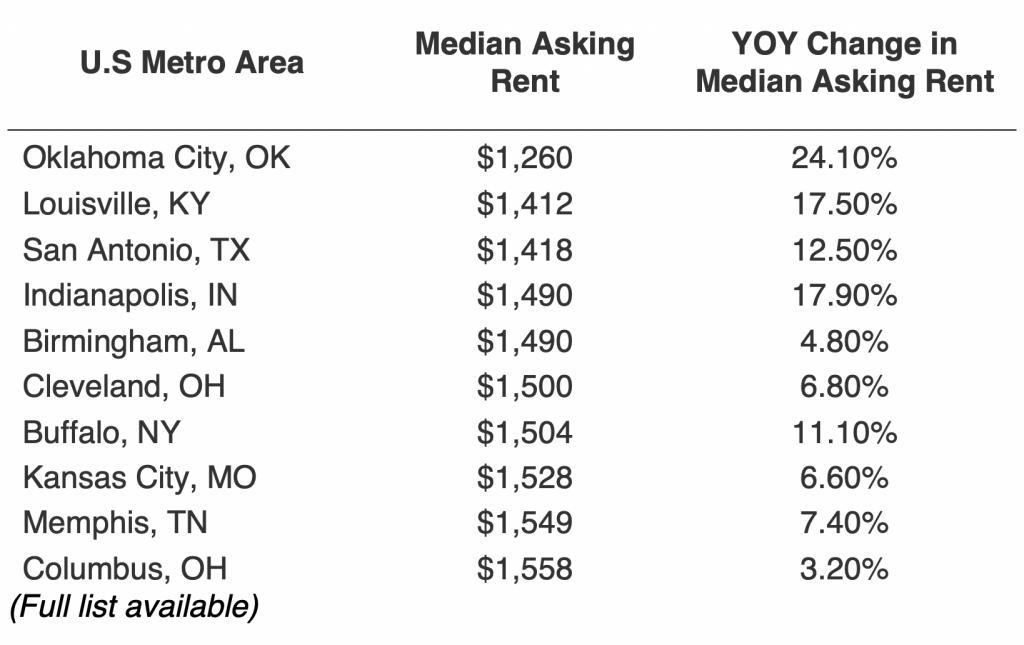

Top 10 LOWEST Median Asking Rent *

* From Redfin News: “Rental Market Tracker: Rents are Growing Half as Fast as They Were 6 Months Ago,” by Lily Katz, October 13, 2022 Methodology – Redfin analyzed rent prices from Rent.com across the 50 largest U.S. metro areas. This analysis uses data from more than 20,000 apartment buildings across the country.It is important to note that the prices in this report reflect the current costs of new leases during each time period. In other words, the amount shown as the median rent is not the median of what all renters are paying but the median cost of apartments that were available for new renters during the report month. Currently, Redfin’s data from Rent.com includes only median rent at the metro level. Future reports will compare median rent prices at a more granular geographic level.

DEMAND IS DIFFERENT NOW

Single-person households accounted for 80% of the new household units that have formed since 2020. Think your one-man Crypto trader or Tik Tok marketer. Meanwhile, the number of Gen Z adults living alone almost doubled from January 2020 to early 2022 (sounds like a lot of COVID breakups), likely using the stimulus income to get started. The point here is that the way labour formation is defined now makes this current real estate cycle and how it interacts with the overall economy very different from past cycles.

Another quirk of the world we live in is Video Conferencing. While we can imagine a world where we go back 5 days a week but in reality, my view is that how we work has changed forever and there are clear benefits for being able to Zoom. What this has done is artificially increased the living space needed (globally). That is to say, adding a corner or a room just for Zoom calls etc, driving up demand for overall living space.

SUMMARY

In summary, the makeup of the labour market, as well as the supply demand imbalances in real estate, are very supportive of higher rental prices and rental yields over the long term.

As a non-resident buyer of U.S. real estate hoping to earn income, this is the perfect storm and has only happened BECAUSE rates are rising.

We may see rates come down in the future where borrowers can easily refinance into a lower rate, but what if prices do not come down or there is a sudden price surge next year? These are all crystal ball-type guesses but what I want to leave with you in this report is that the lack of supply is a major long-term driver of higher rental yields, which is positive for any U.S. real estate investor.

U.S. real estate is considered a safe haven for many – low entry price point, no stamp duties, ease of gentrification, available tax deductions, USD income, ease of travel, quality of schooling, and the list goes on.

If you have any questions about this report or about anything U.S. real estate or mortgage related, please feel free to reach out to me directly at: +65 9773 0273 or email me at [email protected].

A bridge loan is a type of asset-based, short-term loan, typically taken out for a few months to a couple of years pending the arrangement of longer-term financing or an exit, such as the sale. It is used to ‘bridge’ the gap during times when financing is critical but not readily available.

Bridge loans let homebuyers take out a mortgage against their current home to make the down payment on their new home. A bridge loan may also be a suitable choice for you if you want to purchase a new home before your current house has sold. This financing structure may also be beneficial to businesses that need to cover operating costs while waiting for long-term funding.

Introducing AM Bridge!

AM Bridge: A liquidity tool once reserved for the wealthy is now available for everyone!

Real Estate investors are often asset-rich but cash poor. On paper, their net worth may be significant, but their wealth can be tied up in real estate or other businesses. Accessing such funds might mean sacrificing a stake in their business or surrendering some influence over its future – neither of which may be appealing.

It is not always the case that a real estate investor has a few hundred thousand dollars just sitting in the bank readily available to fund a property immediately. Even if they do, they may not wish to tie all their cash upon one property. In today’s market, the property that investors want could be in high demand and needs to be acted on quickly; these could be higher-yielding investments that need immediate funding. Having access to large sums of cash quickly and easily is what HNW investors have had at their disposal for decades. America Mortgages has now made this powerful liquidity tool available to everyone.

– Filling the contingency sale of an old property before you can purchase the new property. You can take a Bridge Loan and use your old house as collateral for the loan. The proceeds can then be used to pay a down payment for the new house and cover the costs of the loan. In most cases, the lender will offer a bridge loan worth approximately 80% of both houses’ combined value.

– To purchase based on the asset value of the new build so the borrower can meet the final payment before delivery.

– For the initial purchase until entitlement or for refinancing after a cash purchase until entitlement.

– To purchase greenfield land to begin commercial development. Once certain stages of development have been completed, it’s easier to obtain traditional bank financing.

– Cash-out Bridge Loan for short-term personal or business use.

The Market

The pandemic has created a boom in the bridge loan market in several ways.

Firstly, it has created an economic environment filled with uncertainties, and as a result, more businesses need capital as soon as possible and can’t afford to wait for a traditional loan. They will thus turn to bridge loans.

Secondly, cash is king these days. With the current value of the U.S. dollar, it may be time to look at accessing liquidity quickly and easily. Normally regardless of your current financial situation, a bridge loan gives you quick access to up to 70% of your property value with simple, easy-to-understand terms.

Thirdly, there has been an accelerated trend of people migrating to Sunbelt cities due to greater job opportunities. This has driven up rents in these cities – the Phoenix area had the biggest rent increase in July, up 27% from a year ago. Due to the profitability of the rental trade, more developers and businesses are looking to acquire multifamily rental units. Short-term commercial bridge loans will provide them with the needed flexibility to take on such assets while they look for permanent financing options. This will help businesses get their assets to perform at maximum potential.

The Problem

When an American Mortgage bridge loan specialist gets a request for short-term financing, they ask three things;

Where is the asset?

What is the value and the outstanding debt?

What situation are you trying to solve?

Number 3 is the most crucial and often the hardest to rationalise. Even the wealthiest people have used short-term bridge financing to access liquidity even when “conventional” options are still possible. This is mainly due to the time and effort required to obtain long-term financing. Cash flow, credit issues, or asset use may prohibit a “conventional” bank loan. When time is a factor in a transaction, it is important to see the opportunity cost of not closing quickly or obtaining a simplified equity release.

Our Solution

Typically, the timeline for traditional bank loan processing from origination to closing is longer than most borrowers prefer for a time-sensitive funding solution or if the project lacks sufficient stable cash flow. The short-term nature of bridge loans generally allows alternative lenders to provide an approval decision and funding with greater speed than a more traditional lender. At America Mortgages, we’ve funded loans in as little as a couple of days since the initial contact.

To allow for such a speedy funding process, the sponsor’s expected property value and experience in executing the business plan are the determining factors in the decision-making process. For this reason, the loans are commonly non-recourse, which is another benefit to the borrower.

Bridge loans are often the preferred funding option for uses such as:

– Highly structured transactions

– Discounted note payoffs

– Lease-up stabilisation

– Redevelopment of existing properties

– Repositioning of a tired or underperforming asset

– Property acquisitions with a short closing timeline (or challenges on the property or sponsor)

– Recapitalisations/Debt Restructuring or Partner Buyouts

– Other uses on a case-by-case basis depending on borrowers’ specific funding needs, where traditional funding sources like banks or insurance companies will have a hard time approving such loan requests.

– Lending to foreign nationals with a “same-as-cash” basis

Short-Term vs. Long-Term

Unlike short-term financing, longer-term financing is susceptible to the regulatory hurdles associated with securing long-term fixed-rate mortgages. This is why bridge loans are often provided by unregulated lenders, family offices, or in some cases, HNW investors. In addition to the regulatory scrutiny, banks or insurance companies require, the sponsor’s credit history and financial strength also take a front seat in the credit decision for long-term loans. Keep in mind America Mortgages will never work with “lend-to-own” investors and lenders. Our goal is to find you a solution that works with your situation with a long-term solution and exit from the bridge loan.

While bridge loans are the preferred option for many specific financing needs, several downsides come with short-term financing that is meant to fund projects. When assets need work, lenders will consider these higher risks and, therefore, charge higher interest rates.

Additionally, bridge lenders generally do not exceed 70%-85% of the property cost basis to limit their financial exposure. However, this leverage is higher than traditional lenders would advance for the same project. This is because bridge lenders rely on the sponsor to fix the issues, which made the property ineligible for long-term financing in the first place. This enables the asset to become stabilised and ready for exit through a sale or by refinancing the property through traditional channels.

As a company America Mortgages‘ only focus is to provide U.S. mortgage financing for foreign nationals and U.S. expats. 100% of our clients are working and living outside the U.S. For more information on AM Bridge, please connect with us via email at [email protected].

Did you know? Non-U.S. resident investors purchased $59 billion worth of home purchases in the past year, a 9% leap from 2021, according to a report from the National Association of Realtors.

We asked 387 of our U.K.-based readers their top 5 questions regarding purchasing an investment property in the U.S.

Below, we answer those questions.

1. Can U.K. citizens buy property in the United States?

Yes, U.K. citizens can purchase property in the United States. It’s very straightforward. U.K. citizens can qualify for a mortgage in the U.S. with America Mortgage’s F.N. Investor + loan program. Borrowers can get pre-approved for a loan within 24 hours of application! What makes the U.S. unique from many other countries, the U.S. does not have any laws which prohibit or limit the ownership of U.S. real estate.

2. What documents are required for British citizens to apply for a U.S. mortgage?

The loan document requirements are based on the loan program the client qualifies for. America Mortgages’ approval rate is 97%, so we can almost certainly find a solution for our clients. Below are a sample of two of our most popular loan programs for non-resident U.S. real estate investors;

America Mortgages Investor +

Income letter by either the borrower’s employer or if self-employed, accountant (purchase, equity release, cash-out, or refinance).

Credit report from client’s home country (must be translated to English). U.K. credit report is perfect; however, if the client has credit in another country, that will also be okay.

Two months’ bank statements (foreign bank accounts allowed).

Passport.

America Mortgages Investor

Qualify ONLY on the rental income of the property (purchase, equity release, cash-out, or refinance).

Credit report from client’s home country (must be translated to English). U.K. credit report is perfect; however, if the client has credit in another country, that will also be okay.

Two months’ bank statements.

Passport.

3. Where do U.K. Citizens buy property in the U.S., and what do they use it for?

U.K. citizen property ownership in the U.S. is evenly split between suburban/resort areas (45%) and rural/urban areas (55%). Top states include:

U.K. citizens use their U.S. properties as investments, second homes, and Airbnb:

4. What is the average purchase price of houses in the U.S. purchased by U.K. citizens?

5. Do U.K. citizens pay the same mortgage rates as U.S. citizens?

Non-U.S. citizens may face slightly higher mortgage rates with a minimum down payment of 25%. What makes the U.S. unique from many countries is there are no age limitations on a mortgage. This means a borrower, 19 or 99, gets to take advantage of the same long 30-year tenure (fixed or adjustable).

Overall, with America Mortgages’ Foreign National loan programs, clients do not need U.S. credit to apply for a U.S. mortgage for foreign investors. We accept international credit reports from your home country or country of residence.

As a company, America Mortgages’ only focus is providing market rate mortgage financing for foreign nationals and U.S. Expats. 100% of our clients are living and earning their living outside of the U.S. We have loan officers in 12 different countries speaking your language, in your time zone. If you’d like to learn more about our loan programs, please email us at [email protected].

The worsening energy crisis in Europe has taken the front page of most media channels this week as the Nord Stream 2 pipeline, a 1,200 km natural gas pipeline from Russia to Germany, remains close, which is driving the Euro to a 20-year low vs. USD. The BBC reports that the annual energy bill for a typical UK household is £1,971. From 1 October, however, that’s due to rise 80% – to £3,549!!! Can you imagine paying USD4,000 a month for electricity?! The new incoming PM, Ms. Truss, will certainly be making this a top priority. We really hope for a mild winter in Europe for everyone’s interest.

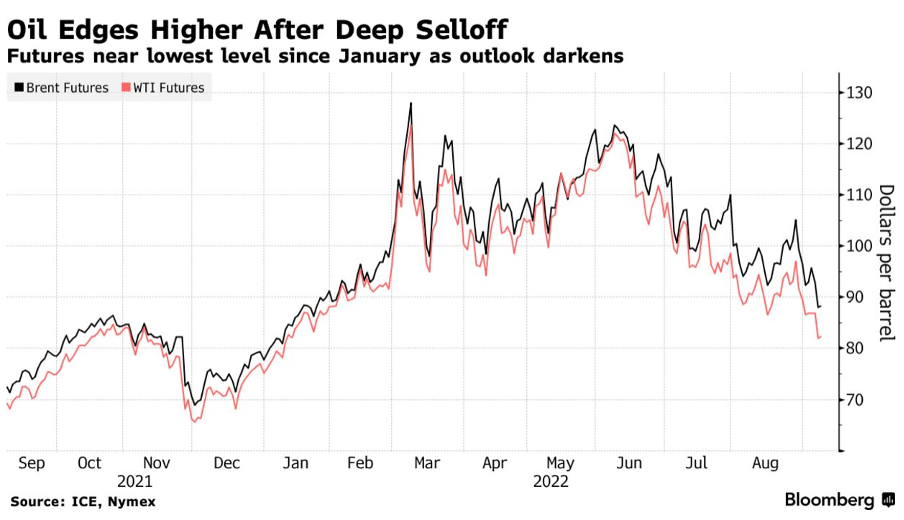

Meanwhile, the Yen is now close to a mind-boggling ¥145 vs. USD, a 24-year low! Oil at $82 is a very critical level and, technically speaking, could break lower, which could give some breathing room to the economy. Seeing Oil go from $120 a barrel in May 2022 to $85 now shows how volatile the world is and also how quickly demand can fall for the most popular commodities.

In the US, Nonfarm payrolls were +315,000 in August (seasonally slow) vs. +526,000 in September, slightly lower than expected but a big month-on-month decline. Meanwhile, unemployment is at +3.7%, slightly higher than expected. The tight labour market while companies are announcing hiring freezes is peculiar. Could this be a recession where employment is less affected? ISM Manufacturing for August was 52.8, unchanged from July – not the decline I was hoping for to give us a little breathing room.

US Rates

30-year fixed 6.12%

15-year fixed 5.32%

30-year jumbo 5.10%

5/1 ARM 5.95%

* Reference only. These rates are Conforming rates, not applicable to Foreign Nationals.

Ex-ante

I’m really keeping an eye on oil prices…I have a sinking feeling that Oil is such a consensus overweight for most hedge funds (and institutions) that technical breakthrough support (say $80) will see a further decline in oil prices which is good news for everyone! European energy prices are now generally 15-20% of GDP, and someone has to pay for it – the public or private sector. If the public pays for it, it will have to run a fiscal deficit of 15-20% of GDP, so more debt on top of the already growing debt problem. The private sector gets tricky, especially for countries that have piled on loads of debt in a short period of time. One country that sticks out is Sweden, with over 150% of private debt to GDP. Nationally, Sweden’s debt service ratio is 27% (highest on record). It appears Sweden, France, and South Korea are the most interest-rate sensitive countries, relatively speaking, according to BIS data. Watch this space. The negative soundbites on the European banking sector are going to get louder and more frequent.

Buy now! Why now?

We are in a perverse cycle where rising rates are actually squeezing up rental yields. The marginal buyer cannot afford to own given rate rises, and the Millennials also cannot afford and must rent – AND, to add to that, there is a 3.8M housing shortage according to the Fed. If you read last week’s “Ex-post, Ex-ante,” places like New York are seeing double-digit percentage increases in rents, BUT 39% of residents are looking to move given the high cost of living. It won’t be long where we are in a world where rates are 7-8%, BUT rental yields could be 15-20% (some parts of Texas can net you low teens yield already).

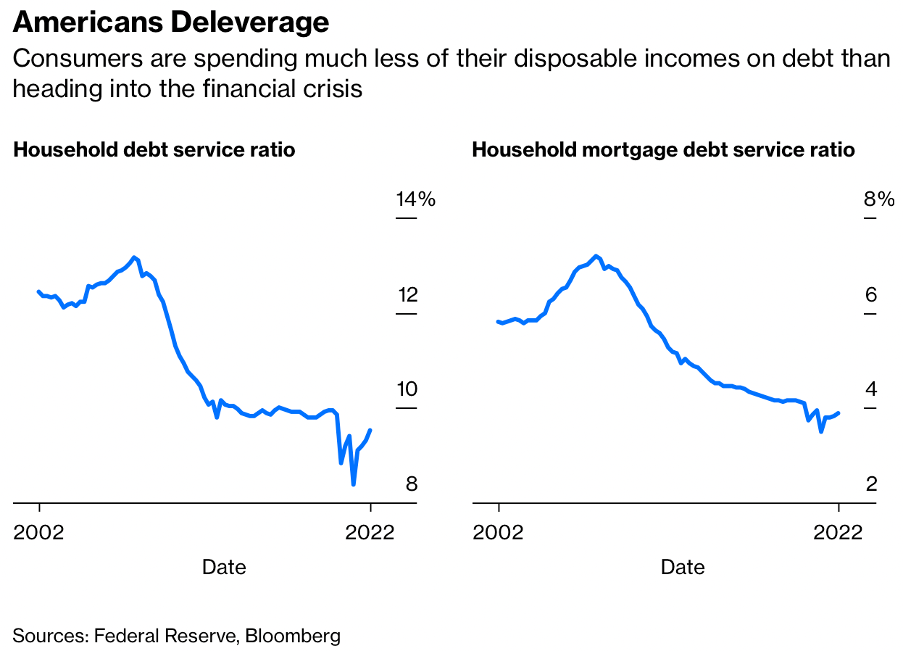

Look at this chart below from a Bloomberg article (7 September) US household debt service ratio has fallen from around 13% at the time of the last housing crisis to 10% now, according to the Fed. The amount households are spending to service their mortgage debt has been cut almost in half, from 7.18% in 2007 to a recent 3.89%!

LOANS OF THE WEEK!

1. Indonesia family uses bridge loan to purchase $5.4M Retail/Office to maximize cash flow

Location: San Diego

Price: $5,400,000

Property: Storefront Retail + Office

Loan Amount: $3,500,000

Cap rate: 4.05% / 100% leased

Loan to value: 65%

Use: Investment

Rate: 8.5%

Loan: AM USA Bridge+

Term: 3-year interest only

– Client was offered a bank loan at 5.75% but given that it is cash-flow based he would not be able to cover the 1.25x cash flow coverage typically required and would be able to get around 40% LTV. Our knowledge was valuable. We knew that California is a tough market as it is with very low CAP rates but the added increase in interest rates is making it even harder to achieve higher loan amounts.

– Our solution: Use a bridge loan with higher leverage, interest-only payment to get into the property. Then position the tenants for renewal of their lease agreements and refinance when rates come back, allowing for more leverage to be supported by the cash flow. Good news is the client is using this strategy to purchase more yielding assets in the US. Loan managed by our Head of Sales, [email protected]

2. Canada tech entrepreneur buys $1.25M condo in Miami

Location: Miami

Price: $1,250,000

Property: Condo

Loan Amount: $875,000

Use: Investment

Loan to value: 70%

Loan: AM Foreign National+

Rate: 6.875%

Term: 30-year fixed

– Client wanted to start building rental portfolio in the US to earn income and to begin developing a credit footprint for future family and business opportunities. Given the nature of his business, he was not able to find bank financing in Canada and we were able to find a mortgage which used his Canada credit and income to qualify. Funded in 43 days with the help of our Canada-based loan officer, [email protected]

3. UK family buys $850K Boston condo in son’s name to develop credit

Location: Boston

Price: $850,000

Property: Condo

Loan Amount: $595,000

Use: Investment

Loan to value: 70%

Loan: AM Foreign National+

Rate: 6.875%

Term: 30-year fixed

– Client bought condo in son’s name to rent out while his son attends boarding school on the East Coast. The intention is for him to stay in the condo upon graduation from university in 4-5 years or continue to rent out to bolster his income while starting out on his career, meanwhile developing US credit for himself. Our UK-based loan officer provided a hassle-free experience throughout their mortgage journey, [email protected]

Biden cancels $10,000 in student debt – timing before the mid-term elections are interesting, but no one can deny that it is a big problem that is stifling growth in many ways. The main event was Federal Reserve chairman Powell’s speech at Jackson Hole, which was a reminder that inflation is being treated more seriously than we are expecting. Risk assets have been correcting ever since – yet bonds haven’t moved with the same intent indicating smart money had priced in the Fed’s response. While 10Y treasuries do not dictate mortgage rates, they 2 are correlated, and we expect some upward pressure on rates.

Ex-ante

Over the next week, we will be paying attention to the Case-Schiller index as a gauge year-on-year home prices, and the big one is August ISM manufacturing index, which consensus has at 51.8 (under 50 is a contraction). If this is lower than consensus, it may portend to be something more recessionary. As we highlighted in last week’s “Ex-ante, Ex-post,” there is historically a big contraction in manufacturing output when rates rise to a certain extent.

U.S. HOME PRICES

We reiterate the underlying fundamentals of housing are very supportive, with an abundant amount of equity and well-known shortage.

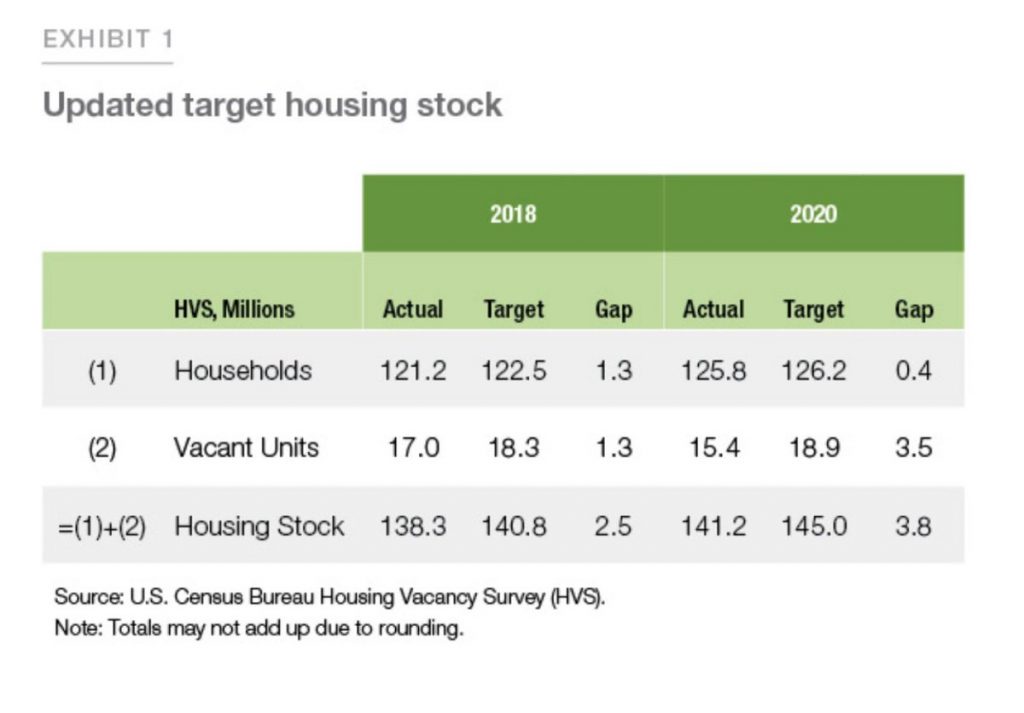

In an article written by the Fed, on 7 May 2021, “Housing Supply: A Growing Deficit”, The claim in 2018, the housing shortage was 2.5 million units, and now, more recently, in 2020, the U.S. has a housing shortage of 3.8 million units.

That is to say, 3.8 million units are needed to not only meet the demand from the growing number of households but also to maintain a target vacancy rate of 13%. Between 2018 and 2020, the housing stock deficit increased by approximately 52%

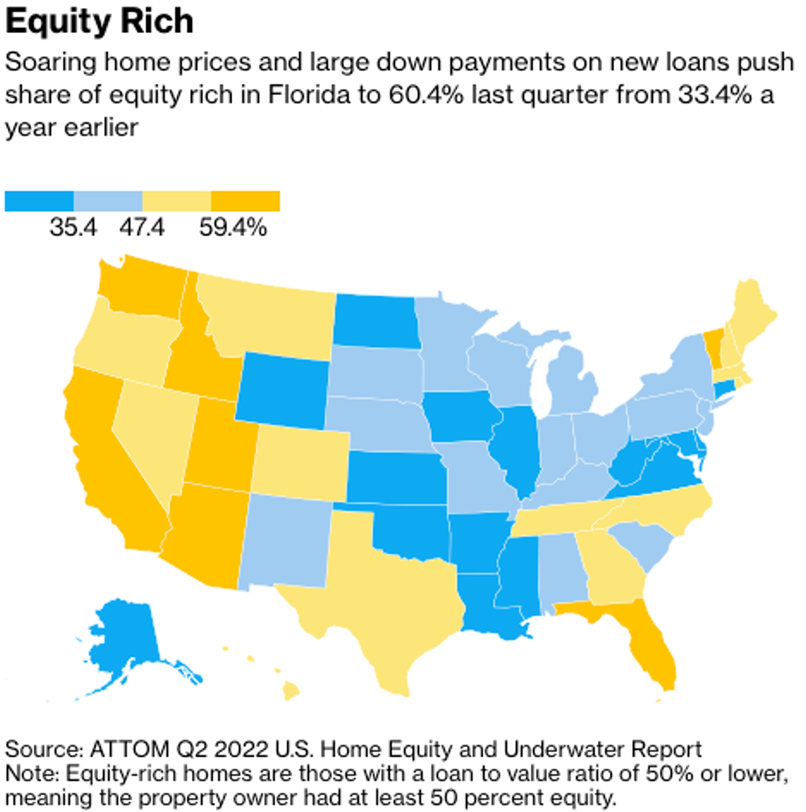

Elsewhere, In Bloomberg’s article published, 5 August 2022, “Almost Half of Mortgaged Homes in U.S. Now Considered Equity-Rich .”This would be the 9th straight quarterly rise, according to the article, fuelled by strong house valuations during the pandemic area. The article definition of Equity-Rich as owners having over 50% in home equity. Some of the highest equity-rich states are Florida, California, Washington, Utah, Idaho (surprising), and Vermont.

LOANS OF THE WEEK!

Singapore citizen purchases new development in Manhattan, New York

Location: New York City

Price: $1,000,000

Property: Condominium

Loan Amount: $600,000

Use: Investment

Loan-to-Value: 60%

Loan: AM Foreign National+

Rate: 6.875%

Term: 30-year fixed

Singapore client attended a presentation by an international realtor on a New York condo launch. America Mortgages was attending the event and helped the client discuss the financing options available.

Philippines businessman purchases home in Florida

Location: Fort Lauderdale

Price: $650,000

Property: Single Family Home

Loan Amount: $455,000

Use: Investment

Loan-to-Value: 70%

Loan: AM Foreign National +

Rate: 6.875%

Term: 30-year fixed

Referred by his local private bank, the client wanted to own a retirement home for the future (he’s only 58) but liked how rental rates have been rising in the area and also wanted more USD income.

Swedish National purchases home in Texas

Location: Austin

Price: $9,500,000

Property: Single Family Home

Loan Amount: $5,225,000

Use: Investment

Loan-to-Value: 55%

Loan: AM HNW+ (Super Jumbo)

Rate: 7.25%

Term: 5-year fixed, 30-year amortized

Swedish client saw our ad on LinkedIn and reached out to discuss the financing options for a Texas property. He was surprised at how easy it was to qualify and close for direct U.S. lending option.

Interested in releasing equity? America Mortgages has a 97% approval rate for both U.S. Citizens & Foreign Nationals. As a company our only focus is providing market rate U.S. mortgage financing for foreign nationals and U.S. expats.

America Mortgages Inc. is a direct lender and leading mortgage broker specializing in financing solutions for U.S. Expats and Foreign Nationals living overseas. We provide access to over 150 U.S. bank and lender programs, delivering tailored mortgage options directly to our international clients. America Mortgages is wholly owned by Global Mortgage Group Pte. Ltd., an international mortgage specialist based in Singapore.