00:52

Donald Klip

My name is Donald Klip. I was not the original speaker. My business partner was speaking, but he fell ill. But were both co-founders, so I’ll just give you a brief background. I moved here from Hong Kong. I’m Hong Kong Chinese. Robert and I identified a gap in the market, which is international real estate financing, in particular the US. Like any entrepreneur, you have a problem, you try to solve it. In 2019, we incorporated this company. We did a round of fundraising with two Korean banks and some venture capital funds.

We have a technology arm. We’re going to be our wholesale lender by the end of the year. But Global Mortgage Group is an international real estate financing brokerage. We offer real estate financing in pretty much every country, and we do specialized real estate financing in Singapore. The pretty lady in the white dress is the queen of GCB bridge lending. She has funded $400 million to date. She is local. We do a lot of specialized lending. Our whole business is servicing private banks globally.

So if a client at Bangkok Bank says, “I want to buy a condo in New York”, they give us that client, and we arrange the financing. The client at the Bank of Singapore says, “I have a $50 million GCV and I want to pull out some cash.” They give it to us, we get the financing done. So that’s what we do. But we have a 100% owned subsidiary called America Mortgages, which is the world’s only US financing company outside of the US. It’s able to secure financing in the US.

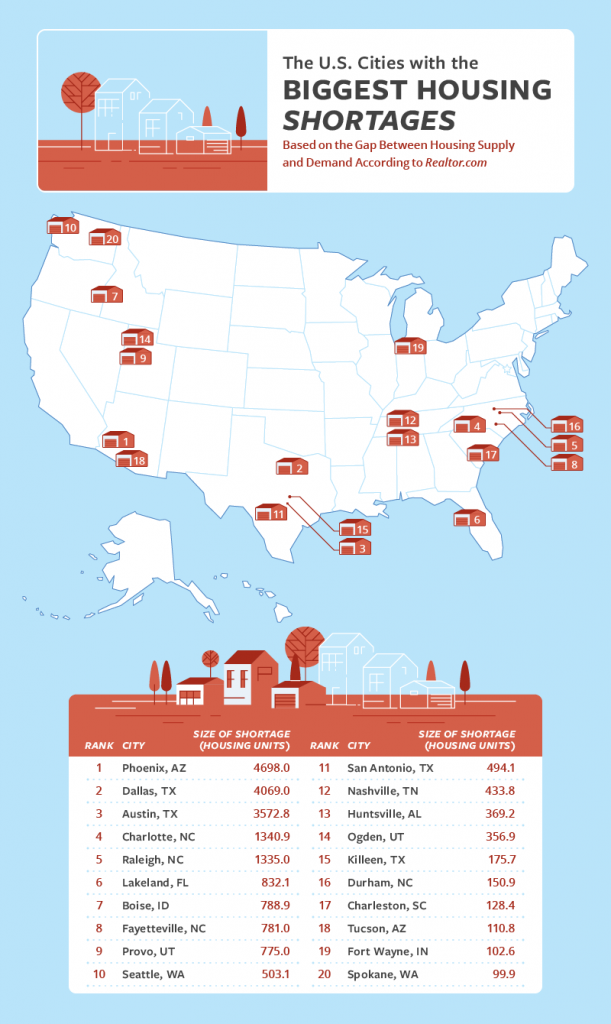

Steve and a bunch of people have heard me say that US residential real estate is by far the best real estate investment in the world. You can’t beat the yield, capital appreciation, tax loopholes, incentives, etc. The entry cost is very low. The trouble is that it’s not something that people know about. So even though we’re focused on the financing, part of our journey is educating folks on the opportunities in the US. I’ll just give you a quick anecdote, and then I’ll introduce our guest speaker who flew here to meet all of you. There is a lack of housing in the US. Depending on where you read, there are about 6 to 8 million units short. Blackstone, which owns Vanguard in Templeton is looking to buy 60% of all single-family homes in the US.

Now, these are very smart people, maybe the smartest in the world. They know things that we don’t know, but I think they know that there’s a lack of housing. And ten years ago, you buy property, it doubles in three or four years. Those days, maybe here, maybe not. I don’t know. But we’ll be in a world where when interest rates are at 8% or 6%, the marginal buyer cannot buy. He has to rent. So, it’s only a matter of time. Every two years, when your rental reversion hits, in five years, rental yields could be 15%, like they were in the seventies. Blackstone knows this. I know this.

Steve knows this, and Hahn knows this, and Tracy knows this. But we’re here to show you why that is. So anyhow, Steve flew in from Atlanta. If anybody knows, the Southeast portion is super moving. Atlanta is the busiest airport in the world. Coca-Cola and FedEx are based there just because logistically, it’s easy to get. Also what’s happening in the US right now is that New York and California are where people go to these fancy schools, and they invent things like Facebook and Tesla and Banks and Morgan Stanley and Goldman Sachs.

But once all these companies get big, they can’t afford to have their business there, so they have to move to places like Georgia and Texas because of low taxes and low cost of living. There’s a lot of opportunity. It’s sort of new, and we’re going to educate you on what this is about. We’re going to talk to you about Atlanta, and why it’s amazing. I’m going to talk to you about how to get financing, and then we’ll sit down and have a nice Chinese meal, and we can talk about life, the stock markets, Atlanta property, health, whatever you want to talk about. So without further ado, Steve, you’re up.

06:36

Steve Kim

Thank you. My name is Steve Kim. As you can tell, the name Kim gives a lot of things away. I’m not the usual Kim. I was born in Jeju Island a long time ago. My family moved to Atlanta in 1973. Very few Asians were there, and I studied German as well. I was in elementary, high school, college, and everything in the US, in Georgia. And when I went to Germany, I was also in East Germany for a month and a half.

When I came back, I saw the world. I wanted to leave America because I grew up in the South. And I had a chance to teach English in Japan. I went to Japan in 1989, and I was in Japan for almost 30 years, and I went back to the US in 2018. And the reason I explained this is I see Atlanta from a hometown person back in 73, from an international perspective. I also know Asian business because I was in Japan for long. Back in 1999, I was working for a company with regional headquarters based out of Singapore and I was a reporter for the oil industry.

I also know many people don’t know anything about Atlanta. When I first went to Japan in 1989, they said, there was an Asian person from Atlanta. They said it’s a lot of racism. They said, what do you know about Atlanta? They said, oh, Coca-Cola, CNN, and gone with the win. And that’s the image of Atlanta. In 2019, they had the Super Bowl in Atlanta. That’s the American football. I was in Tokyo at the time. I’m sure, even though you don’t know American football, I was in Tokyo American Club. They watched together. Aussies, and Germans, watched Atlanta. So what did they talk about in Atlanta? Coca-Cola, Olympics, and Martin Luther King. Coca-Cola is not even in the top ten companies in Atlanta, but people see it as a brand. The biggest company is Home Depot in the top ten. Has anyone been to Atlanta? Please don’t say just the airport.

09:25

Audience

No, but a long time ago when I was a teenager.

09:27

Steve Kim

For business?

09:32

Donald Klip

Trust me, Steve was there.

09:37

Steve Kim

Not so long ago. So most people don’t know Atlanta. So this is the thing I wanted to explain.

The hawks are there. You have Hollywood. I’m talking more about Georgia in general. I’m going to skip around a bit just to show you this is where we are. This is Florida, Alabama. South Carolina, Tennessee, Mississippi. And everyone knows Texas. I attended this conference in Tokyo last week. It’s called SUS, southeast US. Seven states came together with Japan and all the businesses we had in Tokyo. Last year it was in Florida, and next year it’s in North Carolina.

We talked about all the growth that’s happening. The reason I want to show this is you see most major cities in America are built around the water. And prices go up because there’s scarcity. You can’t build more property in Singapore. You have oceans. But in Dallas and Atlanta, we don’t have an ocean. So the property is cheap. That has kept the prices down. Even Phoenix. You saw Lake Denver, and last year the fastest-growing city was Boise, Idaho. But the one that’s crashed the most this year is also Boise, Idaho. You have to understand this. Why do the prices go up, why do they come down? But things are changing in America. Did you know that California is the fifth-largest economy in the world?

US, China, Japan, Germany, California. California by itself has the fifth largest GDP. But the seven states, are bigger than California. We have $3.116 trillion. So we’re the biggest economy together. We’re the fifth-largest economy in the world. I don’t think you’ve been to Alabama, South Carolina, North Carolina, Tennessee, or Mississippi. Maybe Florida or Georgia. So you can see Florida is 1.1 trillion. Georgia is the second largest. But Atlanta is the hub of all. We’re like Singapore. Your regional headquarters are here. Oil companies and their regional headquarters are here.

Because an area is growing so much with development, it needs a regional headquarters. So they’re doing it in Atlanta. They’re not doing it in Tampa, they’re not doing it in Miami. As you can see these are projected by the demographic research Group. That’s Georgia. It’s right here, the 8th largest. Florida is also very big and Texas is already very big. This is the population total. But right now, Georgia is the 8th largest. But it’s going to jump up. This jumping up is very big. These are very famous cities. Tampa, Orlando, Jacksonville, Savannah, Charleston, Augusta, Nashville, Memphis. They need a regional headquarters. So they’re coming to Atlanta. We are becoming like Singapore. Even if you have a factory in Charlotte, Memphis, they need a headquarters here. So it’s becoming a very strange market. We are having development like construction and we are manufacturing. We also have a lot of white-collar regional headquarters. These are some of the major companies. CNN headquarters. Chick-fil-A is also a big brand.

By the way, feel free to ask me any questions. We’re small enough that you can stop me. 31 America’s largest corporation is headquartered in Atlanta. That’s not in Miami. Miami is more financial. Atlanta has 31, like I said. When people think of Atlanta, if you look up in Wikipedia, Atlanta has 500,000- 600,000 people. But metro Atlanta is 29 counties and we have over 6 million people. It’s more than the population of Singapore. So when they say Atlanta, be careful. They are talking about just this inside Fulton County. But the actual area is much bigger. The cost of living is pretty low. Dallas is also very good. This is an interesting thing about this population. 13.8% are born in Northern America.

I’m Korean American. There were very few Asians when I was growing up. But now the Korean American population in Atlanta is the second largest in the US. We just passed New York. New York is a much bigger city. LA is in Atlanta and the Indian population is even bigger. The reason they moved down there is because easy to do business. They’re coming from LA, Chicago. When I was there, we had less than 50 people. Now we have over 150,000. The only thing that I don’t like is they live in one area. I don’t know if you know H Mart. We have more than LA. So there’s a lot. We have, I know it’s a silly name, the Great Wall of China supermarket, but generally, it is still white or African black, basically African Americans.

But we grew the Asian population by 50%. And that’s because of the opportunities there. This is my information. These are the universities. We have over 270,000 students. That is very important for the workforce. We also have a very huge Indian population because of Georgia Tech and Emory University, which has the CDC. You can watch zombie movies, you will see the CDC.

16:59

Donald Klip

It’s also known as Harvard of the South.

17:01

Steve Kim

Yeah, but we need them for the high-tech job. These are the types of homes you should have bought back then. 2019, when you started, you should have bought it. But this is not just Atlanta. A lot of places have increased. The Hatfield is very good for rentals. We have the second-largest film industry in the US after Hollywood. But as far as location shots, Georgia has more location shots than California and 40% still come from outside. We have a lot of short-term rentals for the film industry. We used to call it A list, but now we call it tier one, tier two, tier three, tier four. Like the photographers, and makeup artists, a lot of them have to stay in Atlanta for four to 16 months. And that’s a very good short-term rental opportunity.

Ozark, Avengers, Walking Dead. This is the real recent news. Have you heard of the Inflation Reduction Act? The US and China are not getting along very well. So if you build EV vehicles or clean energy solar in the US, you get a lot of government help. So especially Korean companies, Japanese companies, and German companies are building in the US a lot. This is where they are. Planning and construction, over $50 billion investment. This is going to be very important for housing. We need workers. We need high-tech workers.

18:55

Donald Klip

I’m just going to interrupt. So the workers, are they hiring locally or are they bringing sort of overseas? Like if Hyundai is setting up the EV factory, are they bringing 1000 people from Korea to be based in Savannah?

19:10

Steve Kim

Yes, Hyundai is right here. It’s a $5.5 billion factory they’re building right now. I spoke with SK in Korea. Hyundai by themselves are going to bring 500 expats. They’re not buying houses. They’re renting because it takes them five years to train for the deadline. LG, 4.3 billion. SK, 4 to 5 billion. We’re not talking about the tier three, tier four suppliers. Rivian, which is a US company, 5 billion. We call this the battery belt. Georgia, Alabama, but mostly Georgia, South Carolina, Tennessee and North Carolina. There’s going to be a lot of foreigners coming to Georgia. This is not a small business. EV, from what I understand, is more high-tech. It’s not a cheap job. I showed you the university. It’s very important. They need more housing because even just this one company is creating 5,000 jobs. Where are they coming from?

So there’s going to be a lot of opportunity here. Qcells is the largest solar panel company in the Western Hemisphere. A lot of Korean companies are coming. Atlanta is not a tourist state. When they go to America for two weeks, they don’t stop by Atlanta. They go to Disneyland, Miami, the Grand Canyon, Washington, DC, and New York. So most people don’t know Atlanta, even though it’s a major city, but it’s a very nice city. It’s a great climate. We have mountains. In 1996, the Olympics came to Atlanta. And from 1996, people who would not come to Atlanta came to Atlanta. So the population grew. The film industry started here. People from LA came to Atlanta back and forth, so they started buying houses. EV boom. They’re building right now. The most recent one, was last month.

The US soccer, I think you call it football, is coming to Atlanta. They’re coming from Chicago to Atlanta. And they’re not only coming to Atlanta, they’re building the National Training Center, 23 fields. So the next World Cup is in North America. Canada, America, Mexico. And because our training center is going to be in Atlanta, I think a lot of people will come from overseas. So they will come to Atlanta for the first time. And I think a lot of people will stay because Atlanta is a very good place to live. The temperature is great. This is the Mercedes Benz stadium. This is where one of the World Cup host cities. We do have the Masters if you like golf. This is not Atlanta. This is Augusta, Georgia. But it’s the most famous golf tournament in the world. This is the PGA Tour championship. This is in Atlanta. Everyone likes golf. I do want to show you one thing about Atlanta.

Remember I told you about the water waste? You need water. Water is important because it creates scarcity. Atlanta and Dallas, especially Dallas, have mountains at least, they just keep going. But what happened is this is a highway called 285. And inside 285, because of some civil rights or racial issues, this place went downhill. People did not want to live here. Too dangerous. Bad place. But because the city has grown, this area is becoming very popular. But below this highway, it’s still a little bit rough. I was in Manhattan back in the 1980s. It’s terrible. Good areas now are terrible. I think if I live a long time, in history, this is going to get very expensive. It’s already very expensive up here because everyone wants to be inside this I285. We even have a word ITP, inside the perimeter. OTP, outside the perimeter. Has anyone been to Tokyo?

Do you know the Yamanote line? Inside the Yamanote line is much more expensive than outside. It’s not because it’s any better, it’s just very expensive because people want to be inside. They want to say, “I live inside.” It’s the same here. There are a lot of opportunities here, but it’s rough. Imagine this is the ocean and this is inside because people are vain and they want to be in a nice area. I can talk about this, but I think this is a really big project in Atlanta. This is 22 miles loops, which is 35 km. Also, they’re making this loop so you can walk and cycle. And this is the largest project in the US. If you want to be near this area, it’s also very good. I’m finished with this. I just talked about why Atlanta is a good place to invest.

Here are some properties. These are actually for sale, by the way. There is only one left. This new construction is brand new. They’re building it right now. The price you see the price. And for this one, I think this one you can get 3200 in rental. You do have an HOA fee of 200, but for the price and 3200 in a very growing area in the construction, this is an excellent investment. Brand new. Here’s another one. It’s an older one. This one’s very old. It’s about 100 years old. This is a short-term rental and they are selling all the furniture together you can get 2200 after all payments of utilities, and management fee, but I think you can get a little bit more.

And this is the third one. You can get about 1900 in rental. The price is 214, 900. Smaller. So they asked me to give some samples. Just because the cash flow is good doesn’t mean it’s always the best. It’s my thing. I think appreciation is the best. Even if the cash flow is not so good right now, I told you they’re getting better and better. If you are thinking long term, like ten years, which I hope you do, I think appreciation is key. If it appreciates, rent will increase for sure. You can always refinance in the future. For me, that’s all I have. If you have any questions, even while we’re eating, feel free to ask. I hope you ask more questions, but in the meantime, I think Donald’s going to explain a little bit about how to buy these homes, and how to finance them.

29:05

Donald Klip

So for those of you who came a little bit later, I’m the co-founder of a financing company that finances international real estate. One of our core strengths is US residential real estate, where we’re the only place in the world outside the US, where you can get a mortgage for the US. Most people don’t know that 70% of all mortgage origination in the US is through wholesale lenders and not banks. So, JP. Morgan, Bank of America, Wells Fargo. That’s 30%. The other 70% are wholesale lenders. The most famous wholesale lenders are Rocket Mortgage and Cricket Loan. So those are mortgage originators that give you a loan and they sell it to GIC and BlackRock. This is a snapshot of the types of loans that we do. Of course, there’s no US credit required. We don’t require opening up a private banking account.

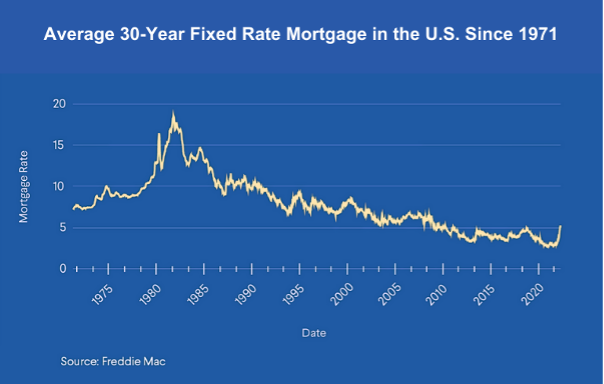

We allow foreign income so you can show your Singapore income tax returns. Loans available in all 50 states up to 75% loan to value. We close it no more than 45 days sometimes. We’ve been known to close the loan in 20 or so days. We can sign all the closing documents in your country. These are purchase, refinance, or cash-out equity. And they’re 30-year fixed-rate mortgages regardless of your age. So in America, you cannot discriminate against anything. So if you’re 100 years old, you can still get a 30-year mortgage. That’s the truth. Now, the good thing about the US is that it’s the only place in the world, and I think this is important to understand. We just had a meeting with a developer and realtor in Irvine, California.

Irvine is like where all the Chinese have moved to in California. Interest rates went up 300% last year and property prices went up 15%. My point is, that the US is the only place in the world that has 30-year fixed-rate mortgages. No other country has this. And the reason why that’s important is that it’s the only product that insurance companies can buy to hedge their liability. So insurance companies, sovereign wealth funds, and endowments have to buy these mortgages because it’s the only thing that you fix for 30 years. A good thing for us is that to finance a property, you can get a mortgage now at 8% for 30 years fixed. But next month, if it’s 7%, you refinance it down for 30 years for 7%. And in 2005, when it’s 6%, you refinance it at 6% for 30 years.

No penalty. For you, my friend, no penalties. The penalties usually are months because the lenders need to sell the loan to the end buyer. Last year during COVID interest rates fell a lot, and all of our business was refinanced. So anyhow, we approved 97% of our loans. And we also have loans, which I’ll get into, that are based on the rental income of the property. These are loan programs. We have three or four. So AM express, we call it the Rico program (Rental income coverage ratio). So basically, we don’t look at your income, we look at the rental income of the investment. And if it covers the mortgage, you qualify. This is probably our most popular program.

If you don’t need to show your financials and your bank statements, you’ll still qualify. It’s much easier if I could qualify above. This looks like a commercial loan, like in commercial real estate financing. You finance a shopping mall, you get some rental income, and then that’s what you base that cash flow on. This is a residential version of a commercial loan. No minimum deposit is required. The loan amount can get quite small as well, and no personal income is required. So this is the most popular loan program in the US. So if the rental income covers the mortgage payments, right now, because interest rates are high, a lot of people can’t buy. So they’re forced to rent. And so the rental income acts as it’s like an option on mortgage rates. So as mortgage rates go up, rental income goes up faster. This has been popular for us.

The next program is an investor. So this is your basic mortgage program. We created this program ourselves with our US bank, where instead of showing your income, you get an accountant to say, “Hey, Hahn made this much money a year and signed it.” Hopefully, it’s true. “So you don’t need US credit. No tax returns are required.” It’s the same type of terms. Except this is based on your income and not the income of the property. This is what everybody in the US gets. It’s called a BTI. If your income is 47% of your mortgage payment, then you qualify. So that is just your traditional US type of mortgage. Again, we’re the only place in the world where you can get this outside the US.

for those of you who joined a little bit later, the holding company, Global Mortgage Group, our whole business is servicing banks. Our clients are Bank of Singapore, and private banks globally. The reason why that’s important is that when a client in Bangkok says, “I want to buy a $5 million condo in New York”, they give the client to us and we finance the loan. This has been one of the most popular loan programs for high-net-worth individuals because they’re busy making money and they just don’t have enough time to show all the financial statements. This is super cool. They look at your stock portfolio or liquid investments and they say that if that balance divided by 60 covers your mortgage payments, you qualify. Your monthly mortgage. This means that this is particularly for bigger loans. It’s cool.

If you have a fidelity portfolio and you have $6 million in a portfolio, you divide it by 60 and you can qualify to get a 100,000. I can’t do the math. But anyhow if you have a portfolio of $5 million, divided by 60, average income of 80. So your monthly mortgage is 80, which is a really big house. You qualify. This has been popular because it’s hassle-free. You don’t need to show too many stuff like that. The more important thing is that the lenders don’t encumber any of those assets. They’re not going to say, give it to us, margin call and all this stuff. They just need to look at it, verify it’s real, and qualify. We invented this. We worked with a US lender to create this. This is your basic US expense.

If you’re a US citizen, and you’re living in Singapore, this is the same as you would get in a bank in the US. Except that we’re here and you don’t have to spend calling banks at three in the morning. We’re here, we can have lunch with you. Are any US citizens here? My parents moved from Asia, from Singapore to the US when I was in high school because they wanted me to go to college and be a doctor. My parents moved to California, and I studied to be a doctor in Los Angeles. But like every Asian family, especially if you have a daughter, you don’t want your daughter to stay in the dorm to meet American boys and do naughty things. So you want to buy a condo so they can stay in the condo.

The trouble is, a lot of lenders won’t accept. You can’t say, “Well, my daughter’s paying me rent.” But now you can. So what we do is your son or daughter stays in the condo, and then we look at the average rent that condo should make. And if that average rent covers the mortgage payments, then you qualify. So this has been popular because my parents did this. Your kids go to school at Harvard Stanford Boston or New York. You buy a condo. After four years, you hope they don’t meet somebody and say that you want them to come back. But after four years, the property price goes up. You can sell it and pay for the university. Or if they want to get a job at Goldman Sachs or Morgan Stanley, you can say, “Well, now you can stay there, and I’ll transfer to your name. And now you have credit.” Because in America, once you have credit, it’s everything. So this has been popular. We’ve been working with education consultants to offer this program. This has been popular. That is a super short presentation on what we do. Let’s spend the next hour or so just talking about the US real estate market. Tod and Tracy are local experts in this area. My friend here, as soon as he came in, said, “Listen, I just want numbers. You can give me this return, I’m going to buy it.” So, let’s talk about this.

41:58

Donald Klip

I know, Steve knows. But there have been Chinese properties, like in Shanghai, Beijing after 2001, of course, everything went up. In Singapore, between 2005, and 2010, property prices doubled. In every country, you have this type of cycle, but it doesn’t last forever. But rental yield lasts forever.

42:31

Donald Klip

So if you do the math, 50% rental yield, you still double your money in five years. But in the US, because of lack of property, as Steve said, there’s $50 billion of EV companies moving to Atlanta. These people need to live somewhere, and they can’t afford to buy. I’ll say one thing. For those of you that came a little bit later, Blackstone is trying to buy 60% of all single-family homes in the US. These guys are smart. They’re not doing it so they can make a 4% return. They’re doing it so they can make 10%, 15%, 20% return because there’s lack of homes. And there’s a lack of homes because after the financial crisis, a lot of home builders, just like other industries, were focused on share buybacks, propping up the share price. They weren’t investing in building as many homes as possible.

43:30

Audience

Excuse me. You’re saying there’s a lack of property, but I think there’s a lot of construction going on at the moment.

43:39

Steve Kim

I will say this. Even though Blackstone wants to buy 60%, all the hedge funds together represent less than 10% of all. Most of the owners are people like you. Do you know why they got into this business? Before Blackstone, BlackRock, and all these people were purchasing multifamily apartments, hotels, and malls, because they did not want to buy one house at a time. That just doesn’t make sense for them. What happened was in the 2007, and 2008 crash, all these homes came on the market, like Foreclosures and Berkshire Hathaway. Warren Buffett said, “If I could buy anything, I’ll buy it. But the problem was who’s going to manage properties?” So what happened is they bought these properties, and people like Excalibur, these property management companies, all they do is manage the property. And they were bought by Blackstone because now they can buy 500 at once, but now they can’t buy anymore.

44:48

Steve Kim

That’s not that many houses and foreclosures. How are they going to buy 60%? There’s no way. So a new genre, basically built to rent, started. We just build a whole community ourselves, and we’re going to make it all into rental. So this is the progression. But the thing is, right now in America, people think we have to own our home. But most people in Asia, when I was in Japan, I never had a dream of owning a home. It’s fine. I can rent. Most of Europe is the same. But right now in America, I think owning a home is key. But to be honest, not everyone wants to live in an apartment. And those expats in Savannah, they’re not going to buy a house. Canada is not going to allow them to buy a house. Atlanta is going to be like New York.

It’s going to be a renter city because prices are going up so fast that they can’t afford to buy homes. There are 270,000 students. They’re not going to buy a house. After you buy a house, it’s really when problems or success starts. So numbers are great, but it’s not met if people are living there. What if they don’t pay? You got to kick them out. You have to evict them. So the property management side of it is also very important. There are strategies. For short-term rentals, there’s section eight. There are many kinds of strategies. I just know that in Atlanta, in five to ten years, even Savannah is going to be a very difficult city. So you have to buy it in an appreciation market.

46:24

Donald Klip

When you own real estate, obviously you want to own a roof over your head, but you either want a trophy asset, which is a pied-à-terre. Like I have a place in New York. It’s cool. New York properties don’t make money. Or you want to own real estate for investment purposes. And the entry points are really low in the US. Like $200,000, $300,000, or $400,000, you can get something that yields 10% to 12% gross right now. But that could be net in a few years.

47:00

Steve Kim

last year the fastest growing city was Boise, Idaho. Because all the Californians were skinking. But the one right now going down the fast is Boise, Idaho, and Austin, Texas. Because there are two or three different markets. There’s the cash-flowing market, that’s not appreciation. Just like Detroit, the Middle East, and the Midwest. New York, and San Francisco, these markets are very trendy. You can go up and down. So if you can time it right, you can make a lot of money in San Francisco, but you have to time it right. But Atlanta, Dallas, and a few cities are stable. It’s a high-interest rate and a high cash flow. Not the best, but also appreciated.

47:48

Audience

I want to add that whatever cities, that you mentioned, Dallas, and Atlanta, are all cash-flow and appreciating markets.

47:58

Steve Kim

It’s not the best cash flow or best appreciation.

48:01

Audience

So your risk is very hedged because if you buy in an appreciating market, it goes down. You have to wait many years to see appreciation. Meanwhile, you’re losing cash flow.

48:11

Donald Klip

Why do you think markets will appreciate?

48:20

Audience

Population, jobs growth. you heard that a lot of places are being constructed. A lot of times news is local. So there are places where we could see over-building construction, like Austin, and Dallas. There are other places, like maybe Atlanta, that may not be seeing overconstruction.

48:55

Donald Klip

If you look at working from home, it was growing at 5% per year. COVID accelerated that. So eventually 20, 30, 40 years, 50 years of that, it’s all going to be hybrid, whatever. But even now, the way jobs are populated or defined, guys aren’t working at a bank or company for 50 years, 30 years anymore. They’re at home. They need to drop shipping on Amazon or do things on TikTok. And they require an additional 100 square foot demand on their rental place. There’s this phenomenon of this additional rental square footage requirement because people are now at home more doing content.

49:55

Steve Kim

The thing is the Southeast, not just Atlanta, Atlanta is the hub, but also a very good investment in Huntsville, Alabama. It’s not sexy. No one says I want to invest in Alabama or Charlotte, North Carolina. Nashville is very sexy. But the Southeast is an area that people don’t know very much. The reason Atlanta is growing is because it’s very young. Most people are not from Atlanta. New business can be started very quickly. It’s hard here in Singapore. Terrible in Tokyo to start a new business. You have people who are already entrenched. You have everything here in Singapore. New business is hard. If you start a roofing company, you can make a lot of money. If you are a dentist, super. Because I was telling you I had some dental problems last year. If I am late 30 minutes, I have to wait another month and a half to get an appointment because we can’t outsource medical stuff.

There’s so much population growth. That’s why the Koreans are the second most. They’re very entrepreneurial. They’re coming from LA. And there are so many new people coming in that it’s going to become a renter city in the state. Because like the 285, there’s finite space. You need finite. People want to live inside. Well, there’s only so much space. We have a lot of problems if we have the zoning issue. Zoning creates scarcity. They won’t let you build up so much. In ten years, it’s a very different city. So I think Greenville and Huntsville are also very nice. Everyone knows California. Everyone knows Hawaii, New York. You’re not going to compete. But everyone still goes to New York. They still go to California. Go to the unsexy places. That’s the key because you have less competition. But as long as it has population growth. Atlanta is a beautiful place. We have Blue Ridge mountains. We have baseball, the NFL, and the NBA. They’re rich people.

52:18

Steve Kim

Don’t go to the sexy. Come to Atlanta. You’ll see that’s why they came in. We have a lot of greenery. It’s 6 million people and it’s growing. We passed New York for a reason. We have a big international community. We’re just far away from Asia. We have a lot of Germans. Japan is the largest foreign direct investment followed by Germany. But we are the hub. We have Delta. 26 years, the busiest airport in the world except one year went through COVID. We have a lot of franchises starting. I hate to say this since you’re not from America, but I can say a lot of people, generally in America, are not that smart. But they’re smarter than Atlanta. All the smart people come to New York.

They see opportunities that the locals don’t. If you listen to podcasts, a lot of people become financially wealthy through real estate in the US. They’re always all very aggressive. They’re not that passive. If you’re busy, passive is fine. I like to focus on appreciation, not because I know it’s going to be appreciated, but because I know the population is growing. I like to buy near a big complex because they know way better than we do. They spend so much money to research an area. So if they’re building in that area, if Hyundai is building in that area and putting in $5.5 billion, I want to be near that area.

54:19

Donald Klip

Capital appreciation is based on three things. It’s population growth, employment, and wage growth. So population growth can be defined as organic population growth, or it means people can move there. Places in California people moving there, and immigrants moving there. But here population growth is these big factories are moving there because Tesla or Hyundai is moving. Because it’s the busiest airport in the world, it’s a hub for all these different places. FedEx is in Nashville. But it’s there because it’s a hub globally. That is what drives price appreciation. It’s employment growth. It’s population growth, which we have because people are moving there. And nowadays, employees have more control over wages. They have sports. Now, the players can argue what they want to make.

55:31

Steve Kim

And there’s two things. Those southeast states are what they call right-to-work states. Meaning for companies, it doesn’t sound good, but it’s easy to fire people. A lot of companies want to go there where it’s easier to fire. Also, it’s tenant-friendly. All of the southeast. Texas, too. If you want to kick out someone, it’s easier. It’s not 100% easy. They’re landlord-friendly. In California, if they don’t pay, you cannot kick them out or you cannot raise the rent. No place in America is 100% landlord friendly. Because even if you win, sometimes you have to wait for the sheriffs to come and take them out. And because of COVID, everyone’s behind. But you do not want to invest in a state that is tenant-friendly.

56:28

Donald Klip

So one thing I also add, some of you know more about the US than others. Some of you may have invested in US residential real estate or real estate elsewhere, but I think you said this perfectly, my friend. You said, I just want to know how much I’m going to make at the end of the month. We have partnered with property managers. Steve has a property management company. But I want to buy something under my name freehold in the US, and rent it out. I’m going to make this much a month. It’s going to sit in a bank account and then the property price is going to increase 5% a year. That’s all I need to know. If you want to find the highest rental yield maybe in Detroit Cincinnati or Cleveland, it’s tougher because they may not appreciate as much. But you need positive cash flow. But, you know there’s these macro drivers that are pushing into that area. That’s what we’re trying to do: educate all of you. It’s not that difficult. We’re focused on financing, but we realize that what we need to do is also educate people. When people say the US, they think Trump, guns, taxes, unfortunately. The funny thing is some of that is true, but the taxes are not true. It’s tax-efficient to set up an LLC, you can deduct a plane ticket to the US to go look at the property. You can deduct your laptop and all sorts of different things. And in fact, we have property in the US. I’m always learning something new. Steve was telling me that in the US, they have an opportunity zone where if you buy a property and double the value in the renovation, after ten years if you sell, you pay no capital gain tax. There are a lot of opportunity zones.

59:20

Audience

It’s all in the master plan for the city.

59:23

Steve Kim

And if you buy an opportunity zone, you know money is flowing in. If you know the local knowledge, I know this is an opportunity. I know it’s going to go up. Is it going to make a lot of money in your first year? I don’t know. No one knows. I don’t know what the interest rate is going to be next year. No one knows. But I know people want to make money if the opportunities don’t give incentives to do it. And then people are coming in. Do you know why? If you know about the Southeast. Let’s give an example of Alabama. Most people probably have a very negative image of Alabama. It’s crazy, people have guns and banning abortion. But you have to put that mind outside. You don’t live there. Alabama is not a bad place. It’s a beautiful coast, but living in Asia, we have a very negative image of America. But most of the money is made there.

01:00:34

Steve Kim

I was there in Tokyo, southeast US. Alabama was there. North Carolina, Toyota factory is bringing a $7 billion EV factory there and he has to hire thousands of people, train thousands of people, and get paying jobs. So they’re not building in California. Everyone’s escaping California. But now California is not bad. It’s a beautiful place. But not a lot of California people are investing outside because it’s better value. If you want to live in California, it’s great. But you’re not living in Alabama. If you’re moving to California, it’s great. The one with the students, that’s a fantastic one. My older brother and his daughter, he said, “I wish I had bought a house for my daughter. Because she would have bought a house and she would have brought in other tenants.” So we call them house hackers. You buy a house, she lives and she brings a roommate. The roommate pays for the mortgage. America is very easy to make money, I think, after having lived in Tokyo for almost 30 years. Hahn, where do you invest?

01:01:58

Audience

Ohio.

01:01:59

Steve Kim

Where?

01:02:00

Audience

Columbus. Cincinnati. I agree with you. Appreciation is slow there. But we are going for cash flow. We do force appreciation. So we buy distressed houses. We create our appreciation so we don’t rely on the market to appreciate.

01:02:21

Steve Kim

That’s another thing. Forced appreciation means we can do it. I can help you up to a point. You buy a thing and you can renovate and make it go up. You force that appreciation. Columbus is a good market.

01:02:40

Audience

Don’t tell people.

01:02:43

Steve Kim

I know. I look at all the markets. Columbus is also good for cash flow and appreciation. I do know this. I know some agents there because Honda is there. It’s in Dublin. A lot of Japanese companies are there with research. So, you have the expensive and the cheap. I’m not just saying Atlanta is good but Columbus is unusual but the weather is terrible.

01:03:06

Audience

But we don’t say that.

01:03:08

Steve Kim

But Columbus is a good market too.

01:03:11

Audience

Intel is going there.

01:03:12

Steve Kim

Yes, intel is going there. As a semiconductor. That’s something called the CHIPS Act. There’s a chipset and that’s bringing a lot of money. Yeah, that’s a good market. I know Atlanta very well.

01:03:32

Donald Klip

You just have to I mean, hard to tell you that they’re sort of full-time experts at this and we’re all part of this Singapore consortium to preach the benefits of investing in US real estate. You look at these UK properties and Australian properties. Australia may have made a little bit of money but none of these UK properties make money. Singapore is so expensive, it’s easier because you can drive there, but the entry point and the yield are really low.

01:04:20

Audience

So I think Steve made a very good point that I resonate with always live where you want to live and invest where it makes the most sense. Invest where it’s decent enough for you and there’s enough appreciation that there’s to be whatever that you project to, and that’s when you make the most money as opposed to investing where you live when the numbers don’t make too much sense. Like, maybe California, or Singapore.

01:04:49

Steve Kim

I knew Columbus was good. I’m always looking at comparing. I don’t think Columbus is as good as Atlanta, except it’s a smaller area. It’s not going to appreciate as much as Atlanta. Because Atlanta is going to be a major city. But in the short term, the next five years, depending on where you buy in Columbus, where you buy in Atlanta is also very important. So, real estate is very local. I know it’s a good market, but not everywhere. You have to know the insight. Remember I told you the 285? No one’s going to know. I don’t know some things and I don’t know much about Columbus. I was in Columbus for my brother’s wedding. That’s it.

01:05:37

Audience

So usually the south has a lot more population growth because the weather is a lot better. And on top of that, Atlanta is business-friendly. The government promotes businesses to go to Texas and Atlanta. The governments proactively go to other states and pitch to them to set up businesses in the city itself. So that when the company sets up the businesses there, they will hire people either from abroad or locally. But when they hire people from another state, they will come in with a higher income. So this pushes up the income level, which Donald said, that it’s population growth, job growth, and wage growth. So that’s when you bring in high value-added jobs, and that’s when the wage grows a lot. And then this has a lot of collateral trickle-down effect because when these rich people spend, they spend, they buy Starbucks, they buy all the different stuff. There are a lot of benefits because the local economies also benefit from these high-income wages spending. Then the whole neighborhood just gets better and better. So just now Steve mentioned the circle People don’t like it in the middle because it’s older stock and people like the newer property. So, they moved out. But with whatever’s happening right now, people want to live near the city like Singapore, Tanglin, and Orchard Road. People want to live near the city. It’s very chic. And the properties are so cheap, so people just buy the older properties, renovate them, and force the appreciation. And that’s when there’s a lot of wealth that’s being built. You could buy the property, do the renovation, or get a loan. You can get a red coal loan. And then after that, do cash up, refinance, and take out your initial capital investment from the property. The property is free, and it’s free because there’s no money in it anymore. You did not put any more money into it because you took it out from a loan. And then after that, it is still generating rental income for you. And that’s what we managed to do in Columbus. But Atlanta has a lot of opportunities for that.

01:08:06

Steve Kim

A lot of people know, but they call the BR method (buy, renovate, rent, refinance, repeat method). It’s not as good as before because the interest rate is high. But don’t worry about the interest rate. The reason I say this is no one remembers if you bought a house in San Francisco 30 years ago. Doesn’t matter what the interest rate was. You would have made money. The thing is, you have to find the three things. Job growth, population growth, wage growth. Those are the three. If those are not there, I don’t care if the cash flow is great because it’s going to be stagnant.

01:08:55

Audience

30-year mortgage, 8% interest.

01:08:58

Steve Kim

But you can refinance.

01:09:01

Audience

When rates go down, you can refinance.

01:09:02

Donald Klip

Just give an example, California launched something like the Home Buyers Assistance Program. The state was helping first-time buyers with the down payment, and it wasn’t much. It was a $300 million program. It was taken up in a week and a half. Everybody could have qualified for a mortgage to buy it, but they were waiting just for a 5%. If you look at cash flow, why do we buy Apple Computer at 35 times earnings? Because it’s growing. But if you think about property, if the interest rates are at 8%, it’s expensive. We all agree. But I bought my first house when interest rates were at 7% in 2005. Yeah, refinanced on the way down or whatever.

If interest rates go from 8 to 7 to 6, prices are going to go up because there’s a lot of people on the sideline. So if you go from $100,000 home, 8%. In 2005, if it goes to 6%, and the property goes to 120, you’re paying more in your mortgage payments. And you can refinance down. During COVID, just like in Singapore, you couldn’t buy the house you wanted because. We always say you date the rate, but you marry the property. You find the property that you want, because of the rates, you can always refinance, and there’s no penalty. I mean, there’s a little bit of administrative stuff, but there’s no prepayment penalties.

01:11:14

Steve Kim

Think about this. Do you think one dollar now is going to be the same ten years later? It’s going to be worth less.

But your payment is the same.

01:11:29

Donald Klip

Apple Computer has so much cash on the balance sheet, but they decided to raise debt financing last year. Why didn’t they do that? Because they know at 5% inflation, their debt is that if you raise $100 million, next year, that debt is worth $95 million. Because inflation will erode it. We saw a little bit of this in Singapore. During COVID, we experienced a lack of supply, and a lot of people coming in. What happened in Singapore is the same on a not-so-aggressive scale in the US. It’s happening everywhere.

01:12:17

Audience

One more thing. When you borrow, you have interest expenses, which can reduce your taxes.

01:12:24

Audience

I think there are two types of mortgages, adjustable rate and fixed rate. I think most Americans currently have a fixed rate.

01:12:43

Donald Klip

Right now, we’re still seeing more fixed rates from foreign buyers just because they know they can refinance. When interest rates were low, people wanted that adjustable rate. They wanted the max because they were looking to buy and sell in five years. To be fair, you should not look at property like equity. That’s not normal behavior. Some people did well, but the way to look at property is more like fixed income. It’s it gives you some cash, and it goes up in value slowly.

01:13:32

Steve Kim

Does anyone else have some questions? I have a question. What keeps you from starting? is it hard to start? I guess it is hard to start.

01:14:01

Donald Klip

I started something new this year, which was short-term investing I started with my sister, but it took me a long time. Buying property, you buy and it’s easier to start. But if it’s such a foreign concept, you need people like Hahn, Tracy, and myself, to walk you through, and educate you. Where do I set up an LLC? Which is a good accountant? What type of insurance deposit? It’s like anything like going to the gym or learning a language. Everything takes about six months, and then you get used to it. Okay, I get it. I know the lingo. We found that everybody understands the UK, and Australia because it’s a Commonwealth system, commonwealth law. If you are investing, you should be irrational about where the opportunities are. Like, I hate guns, and I’m very anti-guns, but would I buy Smith & Wesson stock? Of course, I would. I don’t have an emotional connection to making money. I still wouldn’t buy the stock.

01:15:38

Steve Kim

Remington just started to move the headquarters to LaGrange, Georgia, near Atlanta. I think even UPS didn’t start in Atlanta. By the way, Hahn probably knows it’s not 100% passive. It is some work. Don’t think like I bought it, show me the money. No, you’re going to have some problems. Can you find the right tenant? I work with you after you buy the site. That’s why I can’t do Columbus because I don’t know. On the Atlanta side, you can do it. Property management, something’s going to break. For some reason when you buy a new house for you, something always breaks at the very beginning. For some reason, something goes wrong. Inspection, everything’s fine. You buy the house, pipe breaks. I have to pay money to fix it. But it’s not like we’re buying a stock. But again, if you buy an Apple stock, you can’t call Tim Cook and say, “Hey, I have an idea.”

You can control your property so you have more control of your investment. But don’t think it’s 100% passive. Unless you’re doing a fund or a syndication, it’s not 100% passive. But you learn. Like you said, you have to learn. You don’t have to quit your job. But it will take a little bit of time. But it’s not rocket science. People do it. But some people think I buy a house, give me the money. But there is a little bit of work.

01:17:27

Audience

And the good thing is, for example, he has a property management company. So as long as you do your math properly and you account for paying the property manager to do the work, you have even less work to do. But like what he said correctly, it’s not entirely passive. But if the rent is 4000, how much do you have to pay and work for a $4,000 job per month compared to buying a property that pays you $4,000? It is not entirely passive, but it is an upgrade compared to a job.

01:17:59

Steve Kim

The tenant is paying your mortgage. Then if it appreciates, you make more cash flow or you can refinance, take some of the money out, and buy another house. These past two years have been unusual. It’s gone up too fast. Normally, think of it steady. Even though Atlanta with the soccer company, and soccer federation coming in is going to bring in a huge number of people, and run up the World Cup. But I don’t tell people that. I want to find out where that soccer field is being built. My job is to find it. I went to Korea. I met with SK Battery. I met with many people to find out where they were coming from. It’s inside knowledge. Because I speak Korean, I was in Korea for a whole month.

I want to find out where they’re building, the economic development of Georgia. I met with the office in Korea and also in Japan. I’m friends with Japan, so I want to know where they’re coming from. But remember, it’s going to be one year later. So don’t think the best time to buy is not when cash flow is great. Best time to do it right before cash flow is low. If you can just wait two or three years. If you’re buying just too quickly and want cash, then it’s not a good way. It’s not a good mentality. Remember what Warren Buffett said. He doesn’t care about stock price. He buys companies for the long run. If it’s a good company, it’s going to make. Just because the stock price is lower, he doesn’t buy it on the dips. He buys companies. And that’s the way I think. If you buy real estate, you have to think like him. You buy good property and just wait and take care of it.

01:19:55

Donald Klip

There are also so many tax loopholes in the US. If you spend time researching, you’re learning something new every day.

01:20:05

Audience

So I think on our side, we spent almost two years researching before we even bought our first property. It’s so niche in Singapore. Nobody else is doing it. So we learned from nobody. And we were still working full-time at the time.

01:20:44

Donald Klip

Congratulations. Free from the employer.

01:20:51

Audience

Yeah. And, it’s not 100%, especially in the first year, I think were so happy that we bought our first house, but I think we made no money. Because we made mistakes, chose the wrong tenants. We had evictions, we repaired everything. We repaired the whole house to put a tenant in. It was a bad tenant, and then he wrecked the whole house, and we repaired everything again. So, these are our lessons.

01:21:21

Steve Kim

No, I had to get a broker’s license. For all my clients, I had a property manager I introduced, but they always came back to me because they were not in Atlanta. I have to do all the work that the property manager doesn’t do. So they said, “Can you become property manager, please? Because you’re doing it anyway.” But I had to get a special license. I’ve passed my license, so I’m going to start because something goes wrong, who are you going to call? The property manager or the agent. You’re going to call the agent. You are going to call him first. But whoever is closest to me. I’m not glad she didn’t make money. But people, it takes time. It’s like anything. It’s easy. Everyone can do it. But the thing is, I hope that you guys develop a meetup of real estate so you can share stories.

Because a lot of people make money in the US. I know a lot of people overseas who do it. But as you said, it depends on trust. There are some scammers. So at least you met me and Donald. So if something goes wrong, you can complain to him. Complaining is important. If there is no person to complain to, they can scam you.

All the good things come to me. It’s easy to make money if you’re just patient. And it’s going to be a little bit hassle. Even right now, we’re evicting a person and I have to go to court. And then they’re not still living. They’re not leaving. I’m not saying that’s good, but it’s not like you’re buying a stock. You’re buying a place for people to live.

01:23:18

Donald Klip

there’s so much information. You can find out where Starbucks is in the US. Ordering furniture in the US is super easy. It’s all so streamlined that it actually can be done remotely. You just have to get used to searching for stuff. But there’s just so much information.

01:24:11

Steve Kim

I like Savannah. But Costco came this year. If Costco has put a store there, I know they’re much smarter than me. Some people say Starbucks is there, and it’s still weak. But Starbucks is a little bit late. It’s already very nice.

01:24:36

Donald Klip

I know a little about this because my friend ran a company in Asia and I went into his office. He was in Hong Kong and he had math on his whiteboard. I was like, “What’s this? You sell like cheap toys and stuff?” And they calculate how much foot traffic the population is. Starbucks has more foot traffic. But these guys use a lot of math.

01:25:21

Audience

They know the income level also. They do it in the best neighborhood.

01:25:26

Steve Kim

I knew the son of the Costco founder. I was friends with him in Tokyo. We went traveling together. He told me, “Why did you start your first Costco in Japan, in Tokyo?” No, I’m going to start in but they made the first Costco in too. But most American companies go straight to Tokyo. They want to go straight to LA or New York. I think it’s a big mistake. Because it’s sexy. I have my first store in New York in Times Square. That’s what most people do. They don’t go to Alabama or Tampa first. It’s a little bit ego. I don’t know anyone who said, I bought a lot of property. I didn’t have much money. I invested in New York and made a lot of money. Those are rich people already. Unless you have $100 million to invest now, don’t go to the big market. We have a lot of competition. There are a lot of Chinese investors already during this. I was in Toronto last year. Toronto is more expensive than New York. I love it. But the average price is 1.6 million.

01:26:49

Donald Klip

During winter, it’s cold.

01:27:01

Steve Kim

If you have a chance to visit Atlanta, I can show you. Just come. Because for the money you’re investing, you should come and I’ll show you around. You have to buy your flight ticket. I’ll show you the different areas, the good areas, and the bad areas, and why I think it’s growing.

01:27:23

Donald Klip

So you have to tell me what is the best Chinese restaurant in Atlanta. And how do you think you have an interest in Atlanta? You’ve been there, right?

01:28:16

Audience

I’ve been there a long time ago.

01:28:24

Donald Klip

I don’t know if I told you this, but when we first started, one of my friends in Hong Kong, through a family office, bought 400 homes in Atlanta. This was after the financial crisis. They bought 400 homes after the financial crisis. He was a client of mine, a junior guy. He called me, and he said, “I have some friends who want to refinance their properties.” I’m like, “What are you doing owning property in Atlanta?” And then we met him, he coupled up some money and bought 400 homes. And they put it and he didn’t even put it into a fund. He went out and bought it, but he did all the work. Those things probably went up five times.

01:29:44

Steve Kim

No, not five times. I have a listing agent I work with, and she bought a house back in 2016. That’s not that long ago. She bought it for less than $4,000. She bought the house with a credit card, and it was liveable. This wasn’t that long ago. The house you could buy for $20,000, I just closed on many of them. They were $280,000. They bought it for 20,000 in this area. They sold it for $280,000. It’s a German lady. It’s duplexes and great cash flow. And I said, “But the thing is, we can’t buy that now.” But even then, they told her she was crazy in this bad neighborhood, with a lot of crime. One person bought it for less than $4,000. I said, ”How did she buy a house with a credit card?” She bought it with a credit card. And rent is over $1,000 now. But the thing is, you have to think ahead. You miss that. I mean, no one’s got that after all.

When they crashed, the thing with every fund was about appreciation. It’s like the bubble in Japan, where the Imperial Palace was worth more than California. When it crashed, not everyone switched. No more appreciation, only cash flow. And it has become too much cash flow. But now I think cash flow will come with an appreciation market as long as it’s decent cash flow. But don’t go for the best cash flow, because you have to think of it ten years from now. I also look at the buyer’s age. Your age is very important. If you’re 70, go for cash flow. How old are you?

01:31:50

Audience

Close to 40.

01:31:52

Steve Kim

Really?

01:31:53

Audience

Yeah.

01:31:54

Steve Kim

Anyway, good for him. He can wait ten years. If you wait in real estate, if you have time to wait, then it’s great.

Ten years. Don’t look from ear to ear.

01:32:10

Donald Klip

Do you know why he looks so young?

01:32:15

Audience

Because I have Tracy.

01:32:15

Audience

I have more property.

01:32:22

Steve Kim

Where do you have it?

01:32:25

Audience

Columbus, Cincinnati.

01:32:26

Steve Kim

Columbus is good.

01:32:28

Audience

We went in before all those booms before the COVID happened, so were pretty lucky. We went in because were going for cash flow only. And we know that the Midwest doesn’t appreciate but it’s because of the reshoring of manufacturing.

01:32:47

Steve Kim

Columbus is different. Even Cleveland is good because they have the medicine. So you have to know the companies that you’re investing in. My brother lives in Cleveland. His wife works for Cleveland Clinic. It’s not going to grow like the southeast. No way. It’s too cold and it’s bad weather. The roads are all broken apart because it rains, snows, cracks. I don’t know why people live there, but the jobs are there. North Carolina is also very good, the Southeast is the best place. Beautiful Blue Ridge mountains. You don’t even need air conditioning in some places. It’s so beautiful. They have humidity.

01:34:12

Steve Kim

Commercial aspect, but because nature commercial depends on they have triple net means you pay for the property tax, the insurance and the commonplace. You can also have growth day paper, but commercial generally, but more packages you.

Disclaimer: This transcript is AI-generated, so kindly pardon any transcription or grammatical errors that may be present.