06:50

Robert Chadwick

Hi, everybody, this is Robert Chadwick with America Mortgages. Thank you always for joining us for our regular webinars. Today we have something special. My co-founder, Donald Klip will be joining us. We will be talking in this webinar about the strategies that will come into effect if interest rates get reduced. And we do think that interest rates will be reduced in the U.S. as we come closer to the elections. Donald will also cover what the market trends are for the U.S. as a U.S. real estate investor. This is our first masterclass. We’re pretty excited about it and we’re going to try to continue this as a series as we go. So with that, Donald, thank you for joining today. It’s been a while since we’ve partnered up on a webinar.

07:45

Donald Klip

Thanks, Robert. It’s good to be a part of the action here. It’s been a while since we co-hosted one of these events, and I’m excited to kind of share our findings with the audience. There’s been a lot of anecdotes in the news about how unaffordable housing is. It’s going to play into a topic in the upcoming elections. But I want to lay the foundation for how we’re thinking about the U.S. real estate market and why structurally, we don’t see that prices and rental yields can fall. We’re expecting them to increase quite a bit. And there’s a structural reason for this and I don’t think it’s something that can be fixed anytime soon. So I’ll go through some of the slides on what we’re thinking.

08:42

Donald Klip

We’ll showcase some rental yield comparisons with global cities and it’s going to be interesting. Stay tuned. At the end, there’s going to be some Q&A. Ask us about anything. But in particular, if you want to ask us about U.S. real estate and investing, we’re here to answer any questions. So stay till the very end. Is this the best time to invest in U.S. real estate? And the answer is yes. And we’re going to lay down a systematic approach to explain why we think that is the case. In any investment, there’s always a reason. It could be your friend giving you a hot tip. You like to buy Apple because you like the phone. You like Bitcoin and gold because of certain reasons. Whatever it is, we need to apply the same approach to real estate.

09:46

Donald Klip

So with U.S. real estate, we need to go a little bit, not too long, a little bit back to see the sequence of events leading till now, which has created this dislocation in supply and demand, which makes it the investment opportunity that it is now. I hope most of you in the audience are old enough to remember the dot-com bubble. That was the late nineties, early two thousands. So the dotcom bubble burst. There was a global recession, and then there was an unfortunate event, September 11. But two things happened at the same time or close to each other. One, China entered the WTO in 2001, so China entered the global marketplace. And two, over the next two to three years, the Fed lowered interest rates steadily to 1%. So, low rates, while China entered the global marketplace.

10:44

Donald Klip

We all know what that did to asset prices worldwide till now. There was a big push for government homeownership at the time. And home prices in the U.S. rose on average 55% between the years 2000 and 2007. That’s a national average in some places, like LA and some other markets, Seattle, I mean, home prices doubled, tripled as well. So this started to lay the foundation of when things were about to go, as I say, nuclear. Now, that was a bubble, we can kind of agree. Now, in every bubble, there tend to be three consistent things. There’s greed, which gives fruit to bad actors. So bad actors are born to take advantage of greed. And then there’s usually a lack of compliance. Now, classic examples. Recently, FTX, Sam Bankman Fried, was a bad actor.

11:50

Donald Klip

And some other people in the industry have been taken out of the system. And now Bitcoin, for example, is something that people feel a little more comfortable with. Now, in the U.S. real estate, the same thing happened. There was greed, there was over-leverage, and there was fraud. And the last thing is, that regulations always move slower than greed. Here’s where it gets really interesting. So home prices fell only 8%, actually, in 2008. A lot of people kind of lost their houses. If you worked at Bear Stearns and Lehman Brothers, obviously that wasn’t good. But generally speaking, things could have been a lot worse. But what the Fed did at the time was they put the problems on their balance sheet using various tools.

12:47

Donald Klip

Another thing that happened was the government instituted a bank regulation that made it restrictive for bank lending. A typical scenario would be like, listen, we don’t want this to happen again, so we’re going to implement this regulation so that doesn’t happen. But with interest rates so low, market forces still wanted to buy property, right? So that grew something called wholesale lending. It always existed. But this gave birth to this new growth of wholesale lending, which is a bank, that doesn’t take depositors say, doesn’t have savings accounts or checking accounts. And because the role offering mortgages is in the hands of a private institution, they’re just a lot more common sense with how they offer their mortgages. So the fraud is taken out of the system, that is bad actors.

13:37

Donald Klip

Interest rates are still low and this is where this asset price inflation starts to take off. And this is where you’ll read things like the debasement of currency and those types of things. And in a debasement of currency world, you want to own scarce assets. What are scarce assets? That’s gold, real estate, and bitcoin or crypto. And you see these things kind of playing out at the moment. But why is real estate scarce? You can just build whenever you want. But that’s not the case. There’s a massive dislocation in the supply of U.S. homes in the U.S. Now why is that? Unlike Singapore where housing is subsidized by the government, in the U.S., the major home builders are listed companies.

14:29

Donald Klip

They have CEOs that fly around in private jets and they get paid and compensated by how their share price performs. So imagine you’re this listed company. The world exploded, and housing prices collapsed. The last thing you’re going to do is go to your board and say hey listen, I want to build 1000 homes. So that took a little while to play catch up. But with low rates, China coming into the market, demand was high and a lot of smart people came in and bought homes at low levels and home prices rebounded. Now, so since then, till now, home builders are still playing catch up. So there’s an incredibly severe housing shortage in the U.S. So these are, this is factual information from 2012 to 2022. Last ten years, more or less, 6.5 million households were formed.

15:29

Donald Klip

And this is according to the Census Bureau, were formed versus homes built. 6.5 million more homes were created versus homes built. There’s a current 5.5 million home shortage just to meet demand. Now there are all sorts of things that play into account. There are labor costs and raw material costs. It’s really difficult to get zoning done in the U.S. so home builders can buy. And that just causes a tight supply. And of course, we all want to fix this problem, but we think that this problem isn’t going to get fixed anytime soon, which creates an unfortunate opportunity for renters, but an incredible opportunity for investors. So, more on supply. So there are two types of supply. New homes are being built and there are existing homes. We’ll start with existing homes.

16:27

Donald Klip

So of all the existing homes in the U.S., 80% of the ones with the mortgage have their mortgage rates fixed for 30 years under 5%, and 40% of all mortgages are fixed for 30 years under 3%. So what that means is that up to 80% of all mortgages in the U.S., they’re not selling their homes, because if they want to buy a new home, the rates are going to be higher. And if they sell their home, they’ll have to pay capital gains or they’ll have to buy a more expensive home using the 1031 exchange and pushing out your capital gains. In a nutshell, those existing homes are stuck. They’re squeezed. Nobody’s moving. And then the new homes, as I said earlier, there’s a big shortage because home builders aren’t building.

17:18

Donald Klip

If you Google institutional buying of single-family homes, you’ll see a laundry list of articles that seem to not make it to mass media, which is institutions like Blackstone and Blackrock, which we can argue are fairly good at what they do, and classic Blackstone real estate playbook and they’ve said this, is that they identify supply-demand imbalances like single-family homes. They invest billions to create ginormous landlords, charge fees, and dictate rental. You can Google, all the information is there. So we think, isn’t it smart to invest alongside these institutions? Because they seem to have a pretty good track record of getting it right. So you’ve got this happening in the background. So now we go to demand. Work from home was already happening.

18:18

Donald Klip

10, 20, 30, 50 years from now, none of us are going to be going to the office. Work from home was growing at 2.5% to 5% per annum. Now, what COVID did is that went to 100% overnight. And it’s hard to scale back that once you reach 100%, work habits are not going to reverse. Now, of course, companies want you to go back to the office, and that is happening at the moment. That’s one. There’s a big demand to kind of find a place that’s maybe close to driving distance from your office where you can rent and live. One of the most underappreciated aspects of the U.S. is the ease at which you can gentrify state to state.

19:02

Donald Klip

If you can’t afford to live in California, you can rent a U-haul, drive to Texas, start a new life, get a job, and kids, go to public school, and make it work. These tend to be states with lower cost of living and lower state taxes. And that’s what’s happening now. If you think about all the cool and exciting companies that we hear about whether that’s Tesla, Nvidia, Facebook, or Amazon, they were all created in the coastal states. And once those companies get big and hire tens of thousands of people, nobody can afford to live in those states. And they all kind of migrate to places like Texas, Florida, and Georgia, which we’ll talk about in a bit because those are just cheaper to live.

19:45

Donald Klip

And there’s no surprise that Dallas, Texas is the headquarters of the most Fortune 500 companies in the world. I mean, Tesla just moved there, I think, two or three years ago. It’s the who’s there, right? Another thing that through our research we found is that there is a new movement to earn side income, side hustles, the gig economy, whether that’s drop shipping on Amazon or doing stuff on TikTok or whatever it is. But now when a small couple or two roommates say, let’s rent a place for 1000 sqft, they say, well, let’s add 200 more square feet so we can set up lighting and a camera. And that additional square foot demand is causing this increase in demand. All these factors are causing this massive increase in demand, especially in these lower-cost-of-living states.

20:42

Donald Klip

At the same time that supply is severely constricted. So we all know what happens when demand outstrips supply, right? Prices go up. Here’s where it gets super interesting. Like, so this is a snapshot of where people live in the world. Now, if you look at the G7, it’s kind of known as G20, but say the biggest countries in the world, you look at the rental yields, not that exciting, 4%. Japan is popular right now, but the rental yields are very meager. You look at the Asian nations, including Australia, also barely above 4%. Indonesia is 4.5%, but they have to deal with currency issues. You look at Vietnam and the Philippines. These are the two hottest real estate markets in the world over the past few years.

21:36

Donald Klip

Just because price appreciation goes up doesn’t mean that rental yields go up. In fact, quite the opposite, because there is a theoretical cap on how much you can charge somebody for rent in countries. UAE is a unique situation. It offers low inventory. A lot of people are trying to move there because of the ease of immigration, and low taxes. A lot of emerging countries are moving there. So, it ticks all the boxes. You get rental yield and price appreciation. That market hasn’t been around for a long time. The U.S. on average 8%, mind-boggling, ranked 12th in the world between one and twelve is very not insignificant, but smaller countries in Latin America that nobody buys property to invest in anyway. The point is 8% us dollar growth, market supply shortage, and massive demand, I’ll take that any day.

22:32

Donald Klip

That was surprising when our research team unveiled the results of the work that they did. Here’s where it gets super interesting. Look at the rental yields of these cities. Detroit, 32%. Now these are city center rental yields. So this is a real shock when people see this, they can’t believe it, but it’s public information. Just go on Zillow and you can find all this information. Now all of these cities represent something different. Detroit is kind of more industrial, some of these are college towns. Miami is just a lot of people moving there because it’s kind of a cool place to live. Atlanta is a place that I like, which I’ll talk about in a little while. And all of these cities have different price points.

23:27

Donald Klip

Miami is a higher price point and maybe, I don’t know factually, but let’s just say New Orleans might be lower. Ann Arbor, obviously that’s a college town. Las Vegas, a lot of expo traffic is going there. So in the U.S., it’s something for everybody. You’ve got trophy assets in Miami, Beverly Hills, and Park Avenue in New York, and you’ve got affordable investment starter homes that you can buy and earn rental income. And there are also different strategies. The BRRRR method, which I’m going to talk about student housing, you can bet on this new trend in EV factories being built in the southeast corridor. So, I’m going to talk about it in a moment. Okay, so the BRRRR method. This has been popular recently and the numbers here are an actual client of ours who used our loans to achieve these economic outcomes.

24:32

Donald Klip

In fact, in three short years, they own 15 homes, quit their job traveling the U.S., and live the dream and we help them to achieve that dream. So I’ll give you an example. I’m going to speed this up a little bit so you don’t get inundated with the numbers, but from 2021 to 2023, they bought three homes, $85,000, $182,000, and $125,000. And the cumulative rent for these three units is about $4,300. Okay, so the BRRRR method is you buy them, you can use various ways. You can use our loans, you can use a bridging loan, but the key is to find a somewhat mispriced home in an area with transparent pricing. So if all the homes are $200,000 and this one’s $100,000, $125,000. You’re like, that’s interesting.

25:26

Donald Klip

So you go in, you get your contractor, and you’re on the ground team, and you say, hey, listen, if we put 20,000 into this, could we reappraise it up? And that is what they did, they put a little bit of money, $20,000 to $30,000 max, in these properties. Just two months ago, these were all appraised. So the cumulative purchase price is $390,000. It reappraised for two years. Less than two years at $570,000. So you can see the average increases there. So what they did then was they used our loans to refinance 60% of the $569,000 for $341,000. Okay, so this means that 390-340 is $50,000, which means their net outflow is $50,000 and they’re earning $4,300 in rent a month. That’s gross.

26:25

Donald Klip

you take off half a mortgage, tax, and all that kind of stuff, you’re still at $2,500, which means if you annualize this, you make your money back in two years, and then it’s all upside. This is how you use debt to your advantage. I mean, there’s a famous book called Rich Dad, Poor Dad, and he talks about smart debt. Because in the U.S., the system allows you to use debt. It’s not taxed. There’s a lot of benefits. So this is the BRRRR method. It’s super popular, and we have a lot of information on this, on how to achieve this when you’re ready. So the next one is student housing. Our friends at Blackstone are kind of onto this idea. But if you think about it, over the past 2030 years, how many four-year university universities have been built?

27:15

Donald Klip

No new universities are being built. There’s been additional facilities being built, but student housing isn’t being built like the facilities. So you have China, a lot of these countries, over the last 20 years, a lot more applicants have, in fact, 15 times more applicants since 2000 till now, applying to U.S. four-year universities. But the supply of these universities and housing hasn’t moved. So a lot of demand, and supply hasn’t changed. Student housing has to go somewhere. The schools don’t have enough, so they have to find off-campus housing. So our friends at Blackstone are onto this. In 2022, they spent $13 billion to purchase off off-campus community near Austin. And these are dorms, with no rooms, or beds. And these things are going for $1,300 a month. So the top college towns that we think are good for these are listed.

28:16

Donald Klip

Austin, Ann Arbor, Provo. I’m not going to go through all of them. You can have the slide later. But again, you know Blackstone’s real estate playbook, you find out where there are supply-demand problems. You own as many as you can and you ride the trend. Now, this is a little more old-fashioned investing. I like Atlanta. Atlanta is the busiest airport in the world. Many people don’t know that, but it’s geographically situated in the area of the United States, where it’s just easy to get around. It’s a beautiful city, but it’s benefiting from three things aside from the low cost of living and people moving there for the reasons I mentioned in the previous slides. One, U.S.

29:01

Donald Klip

So when they host the World Cup, I think 2026, maybe the U.S., it’s going to add to all the excitement for obviously Messi has put the U.S. on the map, but that’s a big event. The second is it’s the Hollywood of the south. You’d be shocked at how many Hollywood movies are being produced in Atlanta. They have tax incentives for more movies being produced there. It’s a low cost, good transportation. People can fly back to their fancy places in New York and Beverly Hills very easily. And last but not least, nine EV factories are being built in the southeast corridor. So that’s Georgia, Louisiana, Tennessee, and the Carolinas. And each one of these EV plants hires thousands and thousands of people. And when I look at it is, these are thousands and thousands of potential renters.

29:55

Donald Klip

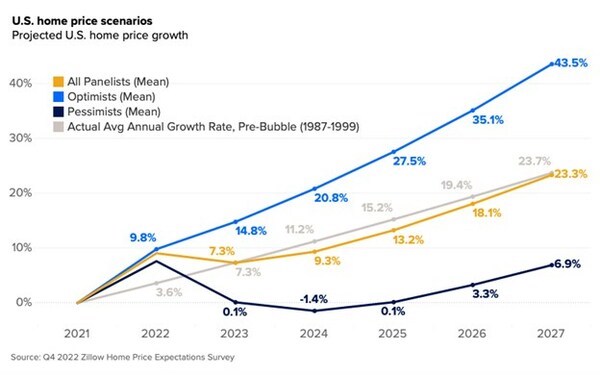

So Atlanta gives a good combination of capital appreciation plus rental yield. Plus you’ve got these macro drivers of people potentially moving there for Airbnb and living there and moving there from the other cities. That’s Atlanta. This is almost the most popular question that we get asked. Like, should I buy now? And I always say the same thing. If you can make the numbers work now, they’re only going to get better. So here’s an example for illustrative purposes. So say you see a house that you like, it’s $500,000. You come to us for a mortgage, and we give you a 75% loan to value, even as a foreign national living overseas. So the loan is for $375,000. You put down $125,000. This is just an example. It’s fixed for 30 years at 8%.

30:54

Donald Klip

So your mortgage payments are $2,500. It rents for $4,000. So you’re making a gross $1,500. You knock off half of that 800 and some change times twelve. It’s a decent cash flow. All right, so the numbers work in 2024. In 2026, let’s just assume that home increases 5% per annum. And we all know that actually, it’s going to go up more than that because, because of all the reasons I just said in the previous slides, 5% per annum is the historical average. So that home now is $550,000. Now, what you do is you refinance that new price of $550,000. 75% loan to value. So you’ve refinanced $412,000. But the rate now is 6% for 30 years. So we assume that rates fall over the next two years.

31:46

Donald Klip

So now your mortgage payment is $1,800, and rents are going up for the reasons I just mentioned previously. Unless, for argument’s sake, let’s say they go up 10% per annum. So now it’s renting for $4,800. So now your gross rental income is $3,000. Now, that’s the game that we’re playing. So you can wait for the interest rates, but if you can make it work, you should pull the trigger, because prices are not staying where they are. I think it, for me, from my slides, I think the next portion, Robert, will talk about the mortgages, different strategies, how to qualify, all that stuff. Then at the end, we’ll just open it up for anything you want to ask us, specifically with real estate or other things, and look forward to hearing all of your questions.

32:39

Robert Chadwick

Thank you, Donald. Super, super insightful. I know you spent a lot of time doing this research along with our team, so thanks to everybody involved. Just to kind of touch on a few things that you talked about. When do you think U.S. interest rates will go down, especially as we near the elections? And what do you think rates will come down to?

33:05

Donald Klip

Yeah I mean, there’s should they be lowered, and will they be lowered? Like the U.S. economy is gangbusters. A lot. A lot of that was COVID rebound, but it is accelerating. But there’s an election coming, and there’s all sorts of things happening behind the scenes that that are in play. Do I think they’re going to cut? I do. I think they’ll cut no more than two times in the second half of this year. Or maybe it’s just one. It’s quite well-telegraphed by Jerome Powell. But you get the benefits. The underlying issue is that people are unhappy because they can’t afford anything.

33:56

Donald Klip

If you’re a wage earner, you can’t afford your rent and you’re kind of forced to rent, but this is, you have to put on a different lens to say, actually that means it’s a good time. That means you can’t buy. The average person can’t buy, he has to rent, and landlords will have the pricing power in this new world.

34:19

Robert Chadwick

I think you’re spot on. And I find our more sophisticated investors tend to be buying now because they do realize that when interest rates go down, people are going to start rushing back into the market, especially the owner-occupied borrowers that have just been sitting on the sideline like you mentioned, guys that were sitting on sub 4% rates. As soon as rates go down, you’re going to have this frenzy again and I think it’s going to be something similar to COVID. So if the investors buy now, they’re going to almost get instant equity as soon as the market churns. So with that, I will start my slides. We’ll talk about the various loan options that are available to nationals and expats.

35:04

Robert Chadwick

And after we will do a question and answer session so you can drop your questions into the chat and we’ll address them towards the end. Also, keep in mind there is a link in the chat that will allow you to book an appointment with one of our loan officers. We have loan officers all around the world who speak a variety of languages. So the calendar is open. Twenty-four-seven at your convenience. So U.S. mortgage loans for international clients. As a company, our only focus is providing U.S. mortgages for foreign nationals and expats. 100% of our clients fit this criteria. There truly is nobody that does this better. In all of our loan programs, no U.S. credit is required. We prefer if you have credit from your home country. Makes things a lot easier. But in the event, in certain countries such as.

36:11

Robert Chadwick

UAE now has a credit reporting agency, but prior we would have alternative means for that. No AUM is required. And what exactly does that mean? We do not require you to fund a U.S. bank account with a certain amount of money that needs to be held in that account for that term of the loan. Which one of the major banks that also does international mortgages is a requirement? So you can use your money at will without any requirement for this. Foreign income is allowed. Whether you’re a U.S. expat or a foreign national. We have loan programs in all 50 states, so regardless of where you choose to invest, we will be able to assist. If you’re a foreign national, we can get up to 75% financing on a purchase and if it’s a refinance, we can get up to 70%.

37:04

Robert Chadwick

So pulling cash out, you can get up to 70%. If you’re a U.S. expat, we try to make it exactly as if you’re walking into a U.S. bank, living and working in the U.S. No W-2 is required. Same market rates as you would be able to get if you were to go to the big bracket banks. But they cannot help you. Normally once you submit all your documents, we can issue a loan approval in 72 hours. This is a great way if you’re looking for a property to obtain a pre-approval letter, so you have this. When you find that perfect property, you do not have to wait. You can submit it with your offer. The average U.S. closing time is 30 to 45 days and you do not have to travel to the U.S.

37:52

Robert Chadwick

There are at least four different ways that we can sign your closing documents. In the country that you’re living in, we offer purchases, refinances, and equity or cash releases. 30-year amortization regardless of age. Super unique for the U.S. I think it’s probably the only place in the world where you cannot discriminate against age. So the U.S. feels if you’re 19 or 99, you should still have the same benefits and opportunities. So you can still get a 30-year or even we have a 40-year mortgage even if you’re 99 years old. Ten-year interest servicing only loan. This is fantastic what this does, especially now that rates are a bit higher. You can fix your rate for ten years, paying only the interest portion.

38:47

Robert Chadwick

After those ten years, you would expect that rate to readjust to the existing or the current rates at that time. That rate stays fixed at that amount. All it does is turn into a 30-year amortized principal and interest loan. So you have a total 40-year tenure, but you also have 40 years of surety of knowing what that mortgage payment is and what Donald had explained in the previous slides about rents going up. Think of the passive income opportunities you’re going to have if you hold these properties for a long period. We have loan programs that are common sense underwriting. What does that mean? Well, if you’re going to buy a commercial property such as a building, you’re not going to qualify off of your rental income or your income earned.

39:37

Robert Chadwick

What you would qualify for is the cash flow of the property. That’s how we qualify the rental properties. It makes sense. If the rental income qualifies on the property, the loan qualifies. And I’ll go into that in another slide. We are very proud that 97% of our loans get approved. If for some reason it doesn’t get approved, it’s normally because of the property and not the borrower. As we mentioned earlier, our calendars are open 24 hours a day, seven days a week, with 30 loan officers working in 12 different countries, speaking a variety of languages, and working in your time zone.

40:24

Robert Chadwick

No longer do you have to be up at three in the morning to talk to a loan officer in New York and explain why Hong Kong doesn’t have a zip code? That no longer exists. You can work at your convenience. So here are our loan programs. This is our most popular loan. This is what I was talking about earlier. This is just pure common sense underwriting. No personal income is required. What you’re going to qualify on is the rental income. And how that is determined is when we do an appraisal for the property, we also do a supplement for the rent. And just like they would do comparisons of the property value, they do comparisons of the property rent. That is the income that you qualify on. And it’s normally a one-for-one basis.

41:16

Robert Chadwick

We have loan amounts as low as $150,000, and with an LTV as high as 75%, you’re only looking at a $200,000 purchase. This means almost anybody can be a real estate investor in the U.S. with 30-year fixed interest-only programs available, and the average closing time is 30 to 45 days. Now, how this loan program works is if you take the gross expected rental income, and in this example, we use $2,400, the total mortgage payment, which includes the principal, the interest, the tax, and insurance, is $2,400. The loan qualifies. We even have a loan program that dips a little bit below that. There is a premium in the rate, but it allows you to qualify even if the rental income only meets up to 75%.

42:10

Robert Chadwick

So if you have questions on this, we can cover it at a later date, or you can make an appointment to speak with one of the loan officers. Our Investor Plus Mortgages. This uses income and has a little bit better pricing, but there are no tax returns required. I mean, can you imagine? We’re doing loans all around the world. If our underwriting had to go through tax returns from a variety of countries, it would just be a nightmare. So how we do it is we qualify the borrower using an income letter. If they’re employed, it’s from their employer. If they’re self-employed, it’s from their accountant. And that merely states two years of income and the current year to date.

42:51

Robert Chadwick

We have a very easy template that either your employer or accountant can follow, and it’s a very simple, easy way to verify income. Again, no us credit or residency is required. Loan amounts to $150,000, 30-year fix, 75% financing, and a quick 30 to 45-day closing. How this works is we need to be at a debt-to-income ratio of 43% or less. So in this example, we use $10,000 in income. As long as the mortgage payments, principal, taxes, and insurance are below $4,300 or below, the loan qualifies. And again, on any of these programs, if for some reason it doesn’t say it doesn’t meet the debt-to-income ratio, or you don’t have enough rent to cover the property, it doesn’t mean that the loan doesn’t qualify. It just means maybe you won’t be able to get the maximum loan to value.

43:47

Robert Chadwick

So our U.S. expat mortgage is very popular. We do a lot of expat loans. We tend to see a lot of loans where somebody would go to one of the big us banks and they go halfway through the process, and then the underwriter says, oh, wait a minute, you’re earning your income in euros, and we can’t accept that. So we see a lot of fallouts from this. For us, foreign-earned income is allowed. We need two years of tax returns, just as you would file in the U.S. You do not need a W-2, which is a huge thing if you’re a U.S. expatriate, you qualify the same as if you were living and working in the U.S. We do require right now that you have a minimum credit score of 680.

44:34

Robert Chadwick

But that seems to be fairly obtainable these days, so it shouldn’t be too much of a hurdle. Again, the loan amounts from $150,000, and in this case, all the way up to 5 million. How it works is we need a debt-to-income ratio below 43%. So again, in this example, $10,000 total mortgage payments of principal, tax, and interest are $4,300. The loan will qualify. So this is a very interesting loan. We work with a lot of private banks. As wealthy people have very complicated tax returns, multiple jurisdictions, multiple agencies, whatever it may be, we’ve tried with, like, all of our loan programs to simplify this as much as possible. So, for our high net worth program, we do not want your income. So we don’t want your tax returns, we don’t want your pay stubs.

45:34

Robert Chadwick

What we’re going to do is qualify you on a two-month average of your liquid portfolio. That’s cash, bonds, stocks, crypto, etcetera. There’s no AUM required, meaning that you do not need to pledge this portfolio, we can do these loans from $3 million to as high as $100 million. The LTV is probably around 60%. Sometimes we can push it a little bit more. But the fantastic thing about this loan program is you’re using these assets to qualify, but there’s no encumbrance on these assets. This means the day after this loan closes, you can trade it, you can sell it, you can do whatever you want, but the loan qualifies using it. Fantastic program. How this works is we take a two-month average of the portfolio. Say in this example, you have $5 million. We divide it over a fixed period of the loan.

46:35

Robert Chadwick

This certainly could probably go over 30 years, but in this particular case, the client only wanted a five-year fixed, amortized over 30. So we take 60 months. It averages to $83,000, approximately a year, I mean, a month. And we use that as your mortgage payment. So in this case, it’s $80,000. Mortgage payment and loan qualify. This, again, super popular program. A lot of our clients have children that are attending school abroad in the U.S. Often after the first year, they want to buy a property for their child to live in. There’s a variety of reasons, and there’s even a way for them to build U.S. credit, which is paramount if your kids intend to live in the U.S. after graduating.

47:25

Robert Chadwick

The great part of this loan program and what makes this super unique to American Mortgage is you do not have to use your income to qualify. Now, a lot of times on these, when you’re buying a property for your student, it would be treated as a second home, meaning that you would have to carry your local housing debt along with the new housing debt in the U.S. And often it doesn’t work. In this case, we do it just as we would do the rental coverage loan. We’ll get an estimation of what the rent will be. We’ll use that as the income to qualify, even though your child will be the renter. But that’s how the loan qualifies super easy. Again, as low as $150,000, all the way up to $3 million.

48:10

Robert Chadwick

An example of that is exactly what we saw in the rental coverage. So as long as the gross rent can cover the mortgage, the loan will qualify. So that is it for my presentation. If you scan the QR code on there, you can get all of our contact information and information on loan programs. I’ll open this up now to our question and answer. Looks like we already have quite a bit, Donald. So let me read the questions and then pertain to you. Jump in. Pertains to me on the mortgage side. I’ll jump in and then we can kind of exchange some ideas on it. First question, should I wait until interest rates get lower or buy now, Donald?

49:01

Donald Klip

Yeah, so that was one of the slides. Should I buy it now? You should not wait because rates may or may not fall. We think they will, but we can almost be assured and went through the argument that prices are going up. So even if rates quadrupled in the last two years and property prices still went up across the board in the U.S., imagine what happens when rates do go down. So what is that saying you like to say, Robert?

49:38

Robert Chadwick

You marry the property and you date the rate. I mean, it’s very appropriate, especially now. And I think if you look at what our investors that have a lot of portfolios, this is where they’re jumping in. This is where they’re buying, because they know as soon as interest rates do go down, there’s going to be a frenzy. You can always refinance the property, but you’re not always going to be able to get the best purchase price. Okay, next question. Donald, you can take this one again. In your opinion, which areas are great for buying now?

50:19

Donald Klip

Yeah. The answer to that is you have to kind of look in the mirror and do your homework and say, what are you buying the property for? It’s just like any investment. If you’re looking for a place to have so you can go visit your child when they’re in university and using our AM student plus mortgages, that’s a different kind of rationale. If you’re looking for just, I want to buy a place and hope it goes up. Well, Detroit has 30-some percent rental yields. I personally like Atlanta. I’m not saying that’s what you should buy there. You should do your homework. It depends on what you’re looking for.

51:08

Donald Klip

I think the southern states are good. Texas and Georgia are kind of interesting to me just because they’re just cheaper.

51:20

Robert Chadwick

I agree. I think if you look, especially at the global markets, look at Canada, for example, look at how the prices have skyrocketed almost to a point where you really can no longer be a real estate investor, at least without having a big checkbook anyway. Next question. Any risk of waiting for rates to drop? I’ll jump in here, and then, Donald, you can kind of add to it. But I think the biggest risk, and we saw this during COVID when rates were super inexpensive, people were bidding 5, 10, 15, 20% even higher over properties just from this fear of missing out. I think when interest rates drop, we’re going to see this again. Again, everybody waiting on the sidelines. I think the risk is paying more for a property. Certainly, again, marry the property, and date the rate. You can always refinance, but you’re not always going to be able to get the best rate. Donald, do you have any?

52:22

Donald Klip

Yeah, totally agree. Well said. It’s if you do the numbers your net cash expense is more sensitive to the property price than the actual interest rate. By the time you wait for the interest rate to fall to where you want it to, the property price is going to be 20% higher. And that’s what you risk.

52:44

Robert Chadwick

And if you look at our journey with our clients, it’s not a one-time transaction. If rates drop dramatically, we will let you know when is a good time to refinance. And we’ll work out the numbers for you to see when to break even on the cost to refinance. Next question. Are there age restrictions for retirees applying for a mortgage? And I had covered this in one of the slides, and I think a couple of times the U.S. is very unique. Besides the fact that we have very long, fixed tenure opportunities, there are no age restrictions. So again, I’m not sure what age you are retired, but you can go as high as you want. Hopefully, you’re living to 100, still investing in real estate. Next question.

53:42

Robert Chadwick

What are the four different ways of closing on a property? Speaking as an expat in Hong Kong. So it depends on the state, the title company, etcetera. But on average, you can go to the U.S. embassy, which is the easiest. It’s not that easy to get appointments. That can be a little bit challenging, but certainly available. There’s something called a RON, which is a remote online notary, meaning that you’re signing on a Zoom that’s a little bit more iffy. Not all states allow that. Still, you can do a power of attorney again if that is allowed, meaning that you could have a trusted advisor sign on your behalf in the U.S. The most simple way is you fly to the U.S. You fly to the U.S. and sign.

54:39

Robert Chadwick

And there’s even a little bit of tax advantages for that because if you’re using it and buying properties as an investment, there often can be a deduction for the trip. Okay, next question. Does being an expat without a W-2 affect mortgage rates and terms? Fantastic question. We get that all the time. Not. We do not require a W-2 as a us expat. Again, we try to make it look like you living and working in the U.S. and just walking into the bank. Next question. What are the maximum LTV foreign investors? Is it income-dependent? So the maximum loan to value is 75% and it is not income dependent if you qualify on the rental income of the property, which is probably the most common mortgage option or mortgage program that we have. Next question.

55:42

Robert Chadwick

If I want to buy a property for my daughter attending school in the U.S., how would I qualify? Personal income question. This goes actually to the question that we had earlier. We, most of the student loans that we do, the borrowers choose to qualify on the potential rental income of the property. Now, I realize your child is staying there, but this is still used. And I think the reason behind this, I know the underwriting reason behind this is normally you’re not buying a one-bedroom apartment, you’re buying something that can be shared and can be rented out as well. Next question. Are you able to connect foreign investors with local realtors in a support network, i.e., contractors, property managers, and insurance to invest in the U.S. market from a distance?

56:37

Donald Klip

Yeah for the people that kind of are knowledgeable about the U.S., they have their means, but sort of new investors need a little more handholding and more education. This is where we come in. So we have all the pieces to the puzzle. We have accountants who can help you set up LLCs, and give you tax advice. We have a realtor network in all the major cities that we trust and we use that we can refer you to. And we also have. And this is the key. A trusted property manager that operates in most states in the U.S., and they’re quite reasonable. So we have all the people that you need to develop your on-the-ground team. We have those relationships and we’re happy to share those with you.

57:28

Robert Chadwick

There’s a portion on our [email protected], it’s a concierge section. As Donald mentioned, it’s everything from connecting to a realtor to, if you need proper FX, transferring funds when you’re buying everything that you would need to be able to successfully transact a U.S. real estate transaction. I missed a question. What is the average mortgage rate for foreign buyers of U.S. properties at 75% loan to value through America Mortgages? This is a really good question. It’s normally approximately 1% higher than what a us citizen would pay. So right now, if you’re looking at U.S. citizens with excellent credit buying an investment property, they’re going to be in the sevens. As a foreign national, you’re going to be in the 8% range.

58:28

Robert Chadwick

Now, again, we do expect these rates to come down, but when you factor in programs such as a ten-year fixed interest only, it brings the interest rate down, especially, as the property values go up. Not the interest rate. The mortgage payments. Next question. Does the rental coverage plus program require tax returns?

58:51

Donald Klip

It does not. What makes this program super simple and very easy to qualify for is it qualifies only on the rental income of the property, which, if you think about when you’re buying an investment property, is the proper way that you should qualify for an investment property. So to answer your question, no. Next question. Do you provide loans to renovate and flip properties? It’s a question we get often, and it’s a very good question. Yes and no. Yes, we provide, but it’s very difficult for a foreigner to qualify unless they have extensive experience. So I think they need to have done this, I think five times to qualify for a fix and flip.

59:47

Robert Chadwick

So there’s not a lot of investors, maybe the Canadian or the Mexican investors may have that option, but in general, it’s very difficult to obtain those loans. Next question. How do some recent changes in the commission laws impact the whole process? I’ll answer this, and Donald, if you have anything you want to add, but the commission laws impacted the realtors. It doesn’t impact the mortgage lenders at all. I believe it’s state-specific. I know in California it’s caused quite an uproar, but when it comes to obtaining financing, it won’t affect your mortgage or the loan programs that we offer, if you have anything.

01:00:41

Donald Klip

That’s good. There’s one on the bottom. Do you have any thoughts on investing in Durham, North Carolina, in terms of rental yield? Again, anything I say does not constitute a reason to be buying in these places. I just wanted to get it out there, but the thinking is sound. North Carolina, is part of that southeast corridor 40% of it is Charlotte. Of the top cities in North Carolina, 40% are our renters because it’s a market where people want to live. It’s a good quality of life. It’s a higher standard of living, but nobody can afford to buy, so they have to rent. And in fact, Durham gets the flow down from Charlotte and Raleigh.

01:01:39

Donald Klip

So those places, it’s kind of like you can’t afford to live in San Francisco, in Los Angeles, so you kind of move down to San Diego, which is also expensive. So Durham is interesting. There’s a big population growth in Durham because people just can’t afford to live in the bigger cities. So, yeah. It’s interesting. I think the rental yields, if I had to guess, probably 15. It’s just a guess, but information is readily available. So if you google rental yield, Durham, North Carolina, I’m sure it’ll just pop out.

01:02:13

Robert Chadwick

And we’re coming up with a report. You can download it from our website or our weekly mailers if you’re receiving them, and it’s going to cover all 50 states and our opinions on the various states where rental yields are and why we think it’s a good state to invest in. The minimum loan amount is $150,000. Can it be lower? Yes and no. On special occasions, we can get maybe an exception to go as low as 100,000. But if you own multiple properties, we can group the properties to be able to meet the minimum loan amount on a portfolio loan. So that’s something we can look at. I would highly recommend making an appointment with one of our loan officers.

01:03:12

Robert Chadwick

And again, the link for that is in the chat, so you can go and book a meeting again twenty-four seven. And I think besides the questions that came up, there’s probably a lot more questions. Getting pre-approved for a loan is free. So if you are considering buying a property, the most important thing is to get pre-approved for a mortgage, get that pre-approval letter, and then once you have that letter, you can go shopping. So it looks like that’s all the questions. Donald, I don’t know if you have any closing remarks.

01:03:47

Donald Klip

No. We act as a financing partner for your journey into U.S. real estate investing. But use us for information, for a sounding board, for tips. Aside from the financing, we’re trying to educate the people outside the U.S. on how amazing this opportunity is that we’ve been given, and let’s take advantage of it. Make some money.

01:04:15

Robert Chadwick

Fantastic. Thank you, everybody, for attending. Our next webinar, I think will be in three weeks. I’m not exactly sure who it’s with yet, but it will be with a very exciting partner. So again, thank you, everyone, for your time. Good evening, good day, good morning, wherever you may be. Thank you.

Disclaimer: This transcript is AI-generated, so kindly pardon any transcription or grammatical errors that may be present.