Our client was a self-employed U.S. expat living in London wanted to buy a property for his daughter attending school in Boston. After his daughter finished her first year of school, he wanted to buy an apartment near the university where should could live and split the costs with her school friends. He wanted to give his daughter a nice, safe place to live and invest in an income producing property.

How We Helped

Our America Mortgages loan officer based in London structured our AM Student+ loan, which allowed the client to qualify based on the proposed rental income and not the client’s personal income. As a self-employed business owner that had a difficult time showing his true debt servicing ability, this was an ideal solution.

The client purchased the property, and her daughter moved in and rented the other two rooms to her friends, who paid 80% of the mortgage payment. This was a smart investment with a well-structured U.S. mortgage program.

As savvy investors already know, U.S. real estate investment has long been considered a fantastic opportunity for building wealth and ensuring financial stability. Until this week financing for foreign nationals and U.S. expats has been mainly limited to 1-4 unit properties. America Mortgages is proud to announce that we have made these mortgage loans available to all our clients regardless of their residency or passport!

“These types of properties present another opportunity for U.S. expats and foreign national investors seeking to invest in U.S. real estate, and America Mortgages is thrilled to introduce our newest mortgage program, AM MultiUnit+, designed specifically for non-resident investors looking to acquire 5-8 units,” states Nick Worthing, Vice President of Residential Lending.

In this article, we explore why multifamily homes stand out as an excellent investment opportunity.

Why Invest in Multifamily Homes?

Steady Cash Flow: Multifamily properties provide several rental income sources from each unit, making sure that investors have a steady and reliable cash flow. This reduces the risk of losing all rental income in the event that one unit is vacant, unlike single-family homes where vacancy results in a complete loss of rental income.

Cost-Effectiveness: Managing multiple units within a single property is often more efficient and cost-effective than managing multiple single-family homes spread across different locations. Consolidating expenses such as maintenance, property management, and renovations can lead to lower per-unit costs and an increase in profitability.

Appreciation and Value:Multifamily properties typically appreciate in value over time due to the increasing demand for rental housing and strategic property improvements. Investors can boost their property’s value through renovations, leading to significant long-term capital gains.

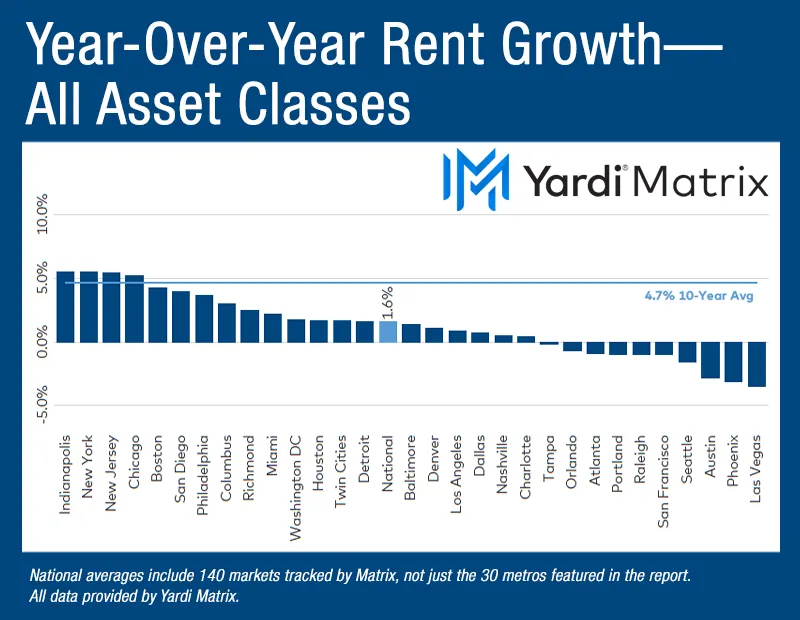

Year-over-year multifamily rent growth, all asset classes. Yardi Matrix

Types of Multifamily Homes

There are various kinds of multifamily homes to consider, each offering different layouts and living spaces.

Apartments: Apartments are owned by a single entity and rented out to residents. They offer a range of affordability, from budget-friendly options to upscale and luxurious living. Some apartments have amenities like community pools, theatres, exercise facilities, gardens, or game rooms catering to various lifestyle preferences and budgets.

Condominiums: Condominium ownership is divided by each unit, with buyers sharing ownership of communal spaces. These units are designed to appeal to specific buyer markets, such as working professionals or seniors. Condominium communities offer the benefits of homeownership along with amenities and low-maintenance living, making them an attractive option for many.

Mixed-Use Developments: Mixed-use developments combine residential units with commercial, retail, entertainment, or cultural spaces. These developments offer residents convenience, with everything from grocery stores to public transit stations within close proximity. Living in a mixed-use development provides a blend of urban living and access to various amenities.

Student Housing: Modern student housing goes beyond basic dorms, offering luxurious amenities and contemporary designs. These spaces are located near university campuses and cater to the lifestyle preferences of today’s students. Many student housing developments feature amenities like spas, game rooms, and fitness centers, enhancing the overall living experience for residents.

Age-Restricted Communities: These neighborhoods are typically limited to residents aged 55 and older, focusing on social engagement and lifestyle amenities. Lifestyle directors, fitness classes, and social clubs are common features, providing ample opportunities for residents to stay active and engaged. Age-restricted communities offer a sense of community and camaraderie for those in the same stage of life.

Low-Income Housing: Government programs aim to make housing affordable for low-income families and individuals. Subsidized housing options are integrated into multifamily developments, providing essential support for millions of households. These units are often indistinguishable from market-rate units, offering affordable housing options without compromising on quality.

Benefits of Owning Multifamily Homes

Diversified Risk: Owning a multifamily property spreads the risk across several units. If one tenant moves out, the loss of income is less impactful compared to a single-family rental. This diversification makes multifamily homes a more stable and secure investment.

Scalability: Multifamily properties provide an excellent opportunity for investors to quickly expand their real estate portfolio. By acquiring a multifamily property, investors can increase their rental units and income potential without the need to purchase multiple single-family homes.

Community and Management: Multifamily properties often creates a sense of community among tenants, leading to higher tenant retention rates. As an investor, managing multiple units in one location simplifies property management tasks, making it easier to maintain the property and address tenant needs promptly.

AM MultiUnit+ Loan Program

At America Mortgages, we provide mortgage solutions for U.S. expats and foreign national investors. AM MultiUnit+ is designed to make the process seamless and accessible, especially for non-residents and U.S. expat investors.

Loan Highlights:

5-8 units

Minimum loan amount: US$250,000

Loan-to-Value: up to 75% for purchase & 70% for cash-out

Underwritten on Property cash flow

No U.S. credit required

No personal income required

Our seasoned mortgage advisors specialize in navigating the complexities of securing financing for multifamily properties. With personalized guidance from pre-qualification to closing, we ensure a seamless and hassle-free experience every step of the way.

Experience the simplicity of our streamlined approval process, specifically designed to meet the unique needs of foreign national investors. We consider factors such as projected rental income, making it easier than ever for investors to qualify for a mortgage.

With nationwide availability across all 50 states, you can confidently invest in the best markets for multifamily properties, whether bustling urban centers or high-growth suburban areas. Let America Mortgages be your partner in unlocking the potential of your multifamily investment journey!

The U.S. is one of the most sought-after countries in the world to invest in real estate mainly because it caters to a wide range of needs, which is why, as a U.K. Citizen, this is the right time to move the needle on obtaining a mortgage in the U.S.

In this guide, we will explain how to get a U.S. mortgage as a U.K. citizen. Whether it is for a new home, an investment or a commercial property.

Can U.K. Citizens Obtain a Mortgage in the U.S.?

Yes, U.K. Citizens can obtain a mortgage to buy real estate in the U.S. The U.S. does not restrict any non-citizens from owning property in the country.

As long as you meet the criteria for owning a property in the U.S., you are free to do so. These criteria are rather simple; you don’t even need a credit history in the U.S. to own property there!

However, it is important to note that you do not receive residency rights by owning a property in the U.S. you can stay there for as long as your visa permits.

Documents Needed to Get a Property in the U.S.?

Here’s a list of documents needed for a U.K. citizen to obtain property in the U.S. However, note that some additional documents may be required on a case-to-case basis.

Proof of your income, your last three years of tax returns, or a letter from your employer – Documents proving your creditworthiness.

Documents proving that you can afford the monthly payments, such as household cash flow statements, utility bills, or bank statements – Documents proving the mortgage’s affordability.

Personal identification documents (passport).

Proof of legal status in the United States as a Foreign National.

Who is eligible for a U.S. mortgage?

While everyone can obtain a mortgage in the U.S. there are specific differences based on immigration status. Let’s look into each scenario further to understand how a U.K. citizen obtains a U.S. mortgage.

U.K. Nationals Without Residency

As a U.K. citizen who doesn’t have permanent residence (a green card) in the U.S. or a work visa, you will not be eligible for a government-backed loan. But you are still eligible for a foreign national loan.

You must establish that you live and earn in a foreign country to obtain this loan.

Permanent Resident With Green Card

As a permanent resident with a green card, you are eligible for the same loan as any U.S. citizen which is – a Fannie Mae or FHA loan. Additional eligibility for such a loan includes a 2-month bank statement, 2 years credit history in the U.S. and 2-3 years of tax return.

Temporary Residents With a Work Visa

Everyone working in the U.S. on a work visa is eligible for the loans, as is any permanent resident. In addition to the usual documents, you may be asked to provide a letter from your company.

What are the differences between getting a mortgage in the U.K. versus the U.S.?

Both U.K. and U.S. mortgage systems have gone through years of upgrades and are very well organised. Yet, there are some differences. If you are a U.K. citizen keen on buying a property in the U.S., read through these differences.

1. Interest Rate

The U.K. follows a variable mortgage rate, wherein the interest rate varies with the market condition. While one can take advantage of the change in the interest rate when they are low, it is equally challenging to keep up when the interest rate is on the rise. The average mortgage term in the U.K. is a short 3.5 years.

The mortgage rate in the U.S. is fixed. This means the interest rate remains constant throughout the term, no matter how long or short. A standard rate of interest helps monthly financial planning. Owing to the fixed rate, the average mortgage term in the U.S. ranges from 15 years to 30 years.

2. Credit Scoring

In the U.S., lenders rely on credit reports from these three agencies: Equifax, Experian, and TransUnion. The credit score is determined based on the credit report and ranges from 300 to 850. FICO scores are the most commonly used credit scores in the U.S.

Unlike the U.S., where FICO scores are used, the U.K. uses credit scores provided by credit reference agencies. These scores vary depending on the agency and range from 0 to 999.

3. Taxing

U.K. citizens are exempt from paying taxes on the sale of primary residence. Whereas an American citizen is liable to pay capital gains up to 24%

How Can U.K. Citizens Obtain a U.S. Mortgage?

America Mortgages can help you obtain a U.S. mortgage. If you’re interested in learning more, reach out to us at [email protected] or visit our website at www.americamortgages.com. Additionally, if you’d like to schedule a commitment-free meeting with one of our U.S. loan officers to explore your U.S. mortgage options further, you can do so using our 24/7 calendar link.

What is an LLC or Limited Liability Company

Investing in U.S. real estate can be an amazing opportunity for non-U.S. residents, offering opportunities for substantial yields, capital appreciation, stability and portfolio diversification. However, navigating the complexities of the U.S. tax system and legal environment requires expert advice, and America Mortgages, besides being your mortgage partner, is there with you at every step of the process. One of the most common and effective strategies for foreign national investorsis to use a U.S. Limited Liability Company (LLC) combined with smart and logical tax planning. Here’s why;

1. Liability Protection

An LLC offers liability protection, meaning that investors are typically not personally responsible for the debts and liabilities of the company. This is crucial for foreign investors who may not be familiar with U.S. litigation risks. Should any legal issues arise, the LLC structure can help shield personal assets from lawsuits or creditors.

2. Flexible Tax Treatment

LLCs provide flexible tax options. By default, a single-member LLC is treated as a disregarded entity for tax purposes, meaning income is reported on the investor’s personal tax return. Multi-member LLCs are treated as partnerships. However, an LLC can also elect to be taxed as a corporation. This flexibility allows foreign investors to choose the tax treatment that best suits their financial situation and goals.

3. Simplified Estate Planning

Every investor should be aware of U.S. estate tax laws, especially in the event of the property owner’s death. By holding property through an LLC, foreign investors can structure ownership in a way that may mitigate these estate tax implications. For example, ownership interests in the LLC can be transferred more easily than direct ownership of property, simplifying estate planning and succession.

5. Operational Efficiency

Owning U.S. real estate through an LLC can simplify the daily operations, especially if the LLC holds multiple properties. This centralization can streamline property management, accounting, and tax filing processes, making owning and managing real estate from abroad as easy as owning it in their home country (maybe even easier).

6. Proper Tax Planning

While an LLC offers numerous benefits, proper tax planning is essential to maximize those benefits and ensure compliance with U.S. tax laws. America Mortgages works with professionals who understand the complexities of foreign-owned or U.S. expat-owned real estate. Here are key considerations for foreign investors:

7. Understanding U.S. Tax Obligations

The U.S. tax filings are not as complicated as many people believe. It is important that foreign national investors understand their U.S. tax obligations, including federal, state, and local taxes. Engaging a tax professional experienced in international taxation can help navigate these obligations and identify opportunities for tax savings.

8. Utilizing Tax Treaties

The U.S. has tax treaties with many countries that can provide benefits such as reduced withholding rates on dividends, interest, and other income. Investors should review applicable treaties and incorporate them into their tax planning strategy.

9. Structuring Investments

Proper structuring can minimize tax liabilities. For example, layering LLCs or using a combination of LLCs and other entities, like corporations or trusts, can provide tax advantages and additional asset protection.

10. Consulting with Experts

Given the complexity of U.S. tax laws, consulting with legal and tax professionals who specialize in real estate and international taxation is essential. They can provide tailored advice, ensuring compliance and optimizing the investment’s tax efficiency.

In conclusion

For foreign nationals, investing in U.S. real estate through an LLC offers significant advantages, including liability protection, flexible tax options, and simplified estate planning. However, these benefits can only be fully realized through careful tax planning and compliance with U.S. tax laws. By leveraging the expertise of professionals and utilizing strategic planning, foreign investors can navigate the complexities of the U.S. real estate market effectively and achieve their investment goals.

Contact us today at [email protected] for a seamless investment experience.

Want to learn more?

We are excited to invite you to our month-long webinar series, offering a wealth of information on U.S. real estate investment.

First, join us for an informative session on Why and How to use an LLC for U.S. Real Estate Investing. Discover the benefits of forming an LLC for overseas property investment, including legal protection, asset security, tax advantages and cost of set-up.

Webinar: Why and How to Use an LLC for U.S. Real Estate Investing

Date and Time: June 7, 2024, 07:30 AM SGT

Registration Link: Register here

Next, don’t miss our session on “3 Tax-Smart Strategies for U.S. Real Estate Investing” Learn how strategic tax planning can enhance rental income for overseas investors, offering insights into U.S. tax strategies that reduce liabilities and boost cash flow.

Webinar: 3 Tax-Smart Strategies for U.S. Real Estate Investing

Date and Time: June 13, 2024, 6:30 PM SGT

Registration Link: Register here

Get ready to elevate your investment game! We can’t wait to see you there.

If you are a Canadian looking to diversify your real estate investment portfolio or simply make the right move by investing in the U.S. property market in 2024, you are at the right place.

But can Canadians buy property in the U.S.? Absolutely Yes! – Canadian Citizens can get a U.S. mortgage through America Mortgages.

What is the eligibility for Canadian citizens to qualify for a U.S. mortgage?

While Canadian citizens can get a U.S. mortgage, what is the eligibility for Canadians to get a U.S. mortgage?

This list is simple: you are eligible if you have a good Canadian credit history (no U.S. credit is required), sufficient proof of income in Canada, and a completed mortgage application. After lenders review your documents, if you qualify, a Pre-Approval Letter will be issued. Although the application and pre-approval can be completed quickly, the entire mortgage process, from application to signing, may take up to 30-45 days.

What are the differences between getting a mortgage in Canada versus the U.S.?

While one can obtain a U.S. mortgage, some differences are worth noting. Knowing these differences will help you level the playing field and better navigate the documentation.

Here are the key differences between getting a mortgage in Canada versus the U.S.:

Mortgage Processing and Approval Times:

In Canada, mortgages are processed and approved within 5 to 10 working days. In the U.S., the average processing time is 30 to 45 working days or longer.

Documentation:

In Canada, there is an extensive requirement for documents if you’re buying a second home or an investment property. Applications for U.S. mortgages require far less. Especially if you’re buying an investment property, you can often qualify only on the rental income of the property, meaning there is no requirement to provide your personal income documents for Canada. If you think about it, it actually makes much more sense since the property will be utilized as a rental and should qualify based on the rental income debt servicing capability.

If you’re looking to buy a holiday home that you will not rent out, you will be required to provide two years of your Canadian tax returns, pay statements, and the other standard requirements for a loan in Canada. Unlike an investment mortgage, which qualifies on only the rental income, you’d need to be able to carry your Canada housing debt along with your U.S. housing debt within a certain debt-to-income ratio.

Mortgage Interest:

This is one of the most significant differences and one of the key reasons why the U.S. property market is an important investment for Canadian citizens. Mortgage interest in Canada isn’t tax-deductible, whereas, in the U.S., it may be deductible against rental income tax.

In addition, fixed-rate mortgages in the U.S. are compounded monthly, whereas in Canada, they can be compounded semi-annually.

Down Payment:

Down payments in the U.S. are higher, with a standard requirement of at least 20% of the home value for a U.S. passport holder and 25% for a Canadian passport holder. Canadian applicants can expect similar down payment requirements for conventional mortgages. However, mortgage insurance allows for down payments as low as 5%.

Amortization:

In Canada, the offer terms range from 1 to 5 years, whereas in the U.S., mortgages can be as long as 30 years with a locked-in rate. There are even options for 40-year amortization, which can not only give you the assurance of how much you’re paying for the next 40 years but also give you the best yield opportunity with a long tenure.

Closing Costs:

Closing costs in Canada are driven by land transfer taxes and legal fees and range from 2.5% to 3% of the purchase price. In the U.S., closing costs vary more widely and often include state taxes, title insurance, and a 1% to 2% origination fee.

Benefits of U.S. Mortgages for Canadians

Now that we are clear on the eligibility of Canadian citizens to get a U.S. mortgage and some of the key differences between the mortgages in Canada and the U.S. let’s understand some of the benefits of obtaining a U.S. mortgage as a Canadian citizen.

Lower and Flexible Interest Rates:

In many cases, U.S. mortgage interest rates are lower compared to Canadian rates, offering the potential for reduced borrowing costs over the life of the loan.

In addition, Canadians will find more favorable terms, such as fixed-rate mortgages and adjustable-rate mortgages, both of which offer the flexibility to choose the repayment option that best suits their financial goals.

Great Investment Potential:

The U.S. property market is a great way to diversify your investment portfolio. The real estate scenario in the U.S. is vast, offering opportunities for capital gain and great rental income. Moreover, such diversification potentially increases overall portfolio health.

Tax Benefits:

The interest paid on a U.S. mortgage may be tax-deductible against the U.S. income tax, which in itself is a great benefit for Canadian investors.

How Can Canadian Citizens Obtain a U.S. Mortgage?

Join thousands of other Canadian investors who have used the services of America Mortgages. If you’re interested in learning more, reach out to us at [email protected] or visit our website at www.americamortgages.com. Additionally, if you’d like to schedule a commitment-free meeting with one of our U.S. loan officers to explore your U.S. mortgage options further, you can do so using our 24/7 calendar link.

FAQs Around Obtaining a U.S. Mortgage as a Canadian

Do I need a U.S. credit history to get a mortgage in the United States as a Canadian?

No, as a Canadian citizen, you don’t need a U.S. credit history to qualify for a mortgage.

Can Canadian citizens buy property in the United States without being residents?

Yes, Canadian citizens can buy property in the United States without being residents.

Are there any special considerations or challenges for Canadian citizens applying for a U.S. mortgage?

The major challenge when applying for a U.S. mortgage is to understand the differences in the process, especially the cross-border tax implications. Working with America Mortgages can help you ease this process a great deal.

Why are foreign real estate investors choosing the U.S. over every other country in the world? Is it the world’s largest real estate market, with over $2.3 trillion transacted last year alone? Perhaps the staggering $53 Billion of U.S. residential homes purchased by foreign nationals in 2023? Maybe they are following Blackstone’s playbook as they also purchased more than $6 Billion in single-family homes across the U.S. My guess is it’s a combination of everything amongst the standard appeal of high returns, diversification, and a stable environment. Let’s dig into the reasons behind this intriguing trend and uncover the answers.

Huge Market Potential

There is a wide range of investment opportunities, including commercial and residential properties and real estate investment trusts (REITs). Foreign investors are motivated by a variety of factors when investing in U.S. real estate. These include the potential for high returns, diversification of their investment portfolio, and the stability and security of the U.S. political and economic environment. Let’s take a look at why these facts attract foreign investors to residential real estate in the U.S.

Capital Appreciation and Cash Flow

The benefits of investing in U.S. real estate are often undervalued. You can make money by renting out your property, and over time, your property’s value can increase. Even though home values have had their ups and downs, here’s the bottom line: in the last 20 years, the average home price in the U.S. has gone up from roughly $140,000 to around $340,000 as of April 2023. So, when you combine rental income and property value appreciation, foreign investors have the chance to see a solid return on their investment.

Diversification

The most important concept in investing is diversification, which helps reduce risk and increase returns over time. Investing in U.S. real estate can help foreign national investors diversify their real estate investment portfolios by spreading their investments across different countries. By reducing risk and increasing returns through diversification, non-resident investors can achieve their investment goals more effectively.

Secure and Stable Investment

The stability of the U.S. political and economic environment makes it an attractive destination for foreign investors seeking security. This is further enhanced by its legal framework and property rights protection. These protections include the right to own, use, and dispose of property and the right to exclude others from the property.

Tax Benefits

Certain tax advantages exist when investing in U.S. real estate, such as deductions for mortgage interest payments and property taxes. However, tax regulations can be complex, so it is important to consult with tax professionals to ensure that foreign investors take advantage of all available tax benefits. Consulting with tax professionals can help foreign investors gain clarity on tax regulations and ensure that they are making informed investment decisions.

No Stamp Duty

The U.S. is one of the few countries that does not have stamp duty for both foreign and U.S. citizen investors. This factor can potentially save you tens of thousands of dollars when compared to markets such as the U.K. or Australia.

Factors to Consider When Buying Real Estate

Regardless of the market, as most people are aware when making investment decisions, it is important to consider personal goals and risk tolerance. With real estate, each property presents a unique set of variables. Here are some important factors to consider:

Market Trends: Research current and historical market trends in the area of investment property. Understanding supply and demand dynamics, price trends, and rental market conditions can help make informed decisions.

Location: Location, Location, Location. It’s often considered the most crucial factor in real estate investing. A desirable location can lead to higher property values, rental income, and demand. Consider factors like proximity to schools, workplaces, amenities, and the overall neighborhood’s reputation.

Budget and Financing: Determine the budget for the investment, including purchase price, property taxes, and ongoing expenses. Explore America Mortgages’ financing options, such as LTV and qualifying criteria.

Property Type: Decide whether to invest in single-family, multi-family, condos, townhomes, or apartment buildings. Each property type has its own set of considerations and advantages.

Property Condition: Assess the condition of the property. Renovations and repairs can significantly impact investment costs and potential returns.

Cash Flow: Calculate the potential rental income and expenses associated with the property. Ensure that the property’s rental income covers all costs and leaves room for a positive cash flow.

Property Management: Decide whether the property will be directly managed by you or by a property management company. Explore property management companies that allow you to live and work abroad from where the property is located, stress and hassle-free.

Ready to Make a Move?

Investing in the largest and most stable real estate can provide foreign investors with a wide range of benefits, including high returns, diversification of their investment portfolio, and the stability and security of the U.S. political and economic environment. By generating cash flow through rental income and capital appreciation, foreign investors can achieve their investment goals more effectively. America Mortgages has one focus: providing market-rate mortgages for non-U.S. citizens, foreign nationals, and U.S. expats. This is 100% of our clients; no one does it better. If you’d like to find out more, please register to speak with one of our U.S. mortgage specialists today.

Our client was a Hong Kong businessman who had acquired more than 400 residential properties in the state of Georgia, all with private bank financing from HK. He had an entire administrative team just to keep up with the mortgage payments, insurance, and property taxes. He wanted a simple solution that would reduce overhead administrative costs and simplify his life without selling properties.

How We Helped

Our America Mortgages loan officer based in Hong Kong structured a refinance into four separate portfolio loans, placing an equal number of properties in each portfolio based on various factors, such as value, time owned, and rental income. These loans not only consolidated the monthly payments but also included impound (internal escrow accounts) to pay the property taxes and insurance when due.

The client was able to reduce his staffing costs by more than 50%, increasing the overall yield on the portfolio significantly while also simplifying his life.

The Federal Reserve raised rates 11 times in 2022 and 2023 but are now hitting pause. The decision comes as inflation has risen. The Fed is holding steady, waiting for inflation to ease closer to the target before making any changes.

The Federal Reserve’s decisions have a significant impact on the housing market. When they adjust interest rates, it directly influences mortgage rates. At the same time, the recent hikes in interest rates were aimed at cooling down the economy after the COVID-19 pandemic.

While higher rates can pose initial challenges for homebuyers, it’s worth noting that mortgage rates have seen a slight decrease from their peak of 8% last fall. As of May 1, the average 30-year rate was 7.39%, according to a survey by Bankrate. This downward trend indicates a positive shift in the market, providing some relief for buyers and sellers alike.

The current market conditions present numerous opportunities. Despite the slowdown in home sales, prices remain stable, with the nationwide median existing-home price almost reaching $400,000 in March.

Savvy investors will understand that purchasing U.S. real estate now means avoiding the buying frenzy and escalating property prices that often accompany decreased interest rates. Additionally, if the Fed decides to reduce rates, you can always refinance later.

Zillow’s expert panel expects home prices will grow at a steady pace in 2024.

Savvy Real Estate Investors Use This Program

Most savvy real estate investors will take advantage of interest-only loans. Interest-only loans increase cash flow and cash-on-cash returns. The first impact that an interest-only period can have on a real estate deal is that it can increase cash flow on the project and cash-on-cash returns as a result.

Improved Cash Flow: Interest-only loans result in lower initial repayments, which can free up cash flow for other investments, property upgrades, or unforeseen expenses.

Tax Efficiency: For investment properties, loan interest can often be claimed as a tax deduction. This means the larger interest payments in an interest-only loan may provide significant tax advantages.

Strategic Investing: With the flexibility of lower initial repayments, savvy investors may be able to diversify their portfolio or strategically invest in higher yield opportunities.

America Mortgages has one of the best interest-only mortgage options in the market! Think about this – a FIXED 10-year interest-only product that converts to a 30-year fixed at the end of 10-years with no adjustment in rate. The only difference is that the loan now becomes a principal and interest payment. This loan is available to all clients regardless of their age. You have the certainty of knowing exactly what your mortgage payments are for 40-years. If interest rates go down, refinance into another 10-year program. It’s that simple.

At America Mortgages, we recognize the complexities of the U.S. housing market. That’s why we’re here to provide expert guidance. Whether you’re a foreign national investor or a U.S. expat, our team can assist you in finding the right mortgage for your needs. Offering up to 75% LTV in all 50 U.S. states for Foreign Nationals and 80% for U.S. expats, America Mortgages is your trusted source for dependable, flexible, market-rate U.S. mortgage loans.

For any questions or personalized assistance, our committed team at America Mortgages is here to support you along your real estate investment journey. Reach out to us at [email protected]. If you’d like to schedule a no-obligation meeting with one of our U.S. loan officers to explore your U.S. mortgage options, use our 24/7 calendar link. Don’t wait; take the next step towards owning your investment home in the U.S. by contacting us today!

Top 5 Foreign Buyers of U.S. Residential Real Estate*

China 13% of total = $13.6B

Mexico 11% of total = $4.2B

Canada 10% of total = $6.6B

India 7% of total = $3.4B

Colombia 3% of total = $900M

Top 5 States for Foreign Buyers*

Florida 23%

California 12%

Texas 12%

North Carolina 4%

Arizona 4%

US$53.3 billion*

The total value of foreign buyers of U.S. real estate

$639,900*

The average purchase price by a foreign buyer

*National Association of Realtors, year ending March 2023

Contents:

Average purchase price of top 5 foreign buyers

Top 5 states buyers from China, Mexico, Canada, India and Colombia are choosing, respectively

Top 5 origin of foreign buyers in Florida, California, Texas, North Carolina and Arizona, respectively

What surprised us from our research!

TOP 5 FOREIGN BUYER ANALYSIS

Asian buyers continue to lead the charge as the largest group of buyers, with a 38% market share. Going forward, we expect to see increased demand from SE Asia as growth in this region continues to exceed expectations.

LATAM was the runner-up with a 31% share of total foreign buyers, not far behind China. We are very excited about the growth outlook for LATAM as the reshoring of manufacturing to The Americas, and the growth outlook improves. One interesting point is that Colombia replaced the United Kingdom as the 5th largest international buyer, proving the growth of LATAM at the moment. We have recently set up an office in Panama and are looking to rapidly expand our footprint here.

European buyers accounted for 14% of foreign buyers, while Canadian buyers alone accounted for 10%.

Chinese buyers continue to have the highest average purchase price at $1.2 million, as buyers purchased in expensive states: 33% of Chinese buyers purchased a property in California, and 6% purchased in New York. This makes sense since California and New York have better-known schools, and a big driver in this decision is education. See our Deep Dive on The Best U.S. High Schools.

Mexican buyers typically purchased the least expensive properties, with Texas as the preferred destination. This can be explained by the geographic proximity.

Average purchase prices for Foreign Buyers

China $1.2M

Mexico $449K

Canada $779K

India $577

Colombia $355K

Buyers from China – Top 5 Destinations

California 33%

Florida 16%

Texas 8%

Colorado 6%

New York 6%

Buyers from Mexico – Top 5 Destinations

Texas 48%

California 18%

Ohio 6%

Arizona 4%

Florida 4%

Buyers from Canada – Top 5 Destinations

Florida 55%

Arizona 14%

California 4%

Louisiana 4%

Montana 4%

Buyers from India – Top 5 Destinations

California 20%

Pennsylvania 14%

Texas 11%

Alaska 9%

Illinois 9%

Buyers from Colombia – Top 3 Destinations

Florida 80%

California 13%

Illinois 7%

TOP 5 DESTINATION ANALYSIS FOR FOREIGN BUYERS

Florida is the top destination for foreign buyers with 23% market share, mostly coming from LATAM 46%, Canada 24%, Europe 16% and Asia 14%. Florida has the best combination of vacation home, investment property and also luxury homes.

California has the 2nd largest market share of foreign buyers at 12%, mostly coming from Asia. Direct flights, temperate weather, and well-known universities make it an obvious destination for Asian buyers. See our California Report.

Texas was the 3rd top foreign buyer destination, with a 12% market share. Texas is one of our top 3 choices for pure real estate investments. The zero-state tax rate will always generate an incoming population from gentrification and also companies setting up their headquarters. For example, Dallas is the headquarters for the Fortune 500 companies in the world!

North Carolina was the biggest surprise to me as the 4th-highest destination for foreign buyers. One of the prettiest and underappreciated states, North Carolina, deserves more research on what is driving the interest of foreign buyers. We will keep you posted.

Arizona has always been a popular destination for foreign buyers and is the 5th-most popular destination, with 4% of all foreign buyers.

Share of Top 5 State to Total Foreign Home Buyer Purchases

Florida 23%

California 12%

Texas 12%

North Carolina 4%

Arizona 4%

Florida – Origin of Foreign Buyers

LATAM/Caribbean 46%

Canada 24%

Europe 16%

Asia/Oceania 14%

California – Origin of Foreign Buyers

Asia/Oceania 61%

LATAM/Caribbean 22%

Europe 7%

Africa 7%

Canada 3%

Texas – Origin of Foreign Buyers

LATAM/Caribbean 55%

Asia/Oceania 25%

Europe 11%

Africa 5%

Canada 4%

North Carolina – Origin of Foreign Buyers

Asia/Oceania 50%

Europe 22%

LATAM/Caribbean 22%

Canada 6%

Arizona – Origin of Foreign Buyers

Canada 37%

Africa 26%

Asia/Oceania 16%

Europe 11%

LATAM/Caribbean 11%

What surprised us from our research?

The average price for a Chinese buyer is $1.2M

North Carolina, the 4th most popular state for foreign buyers

Asians are the largest foreign buyers of North Carolina real estate

Indian buyers prefer Pennsylvania as their 2nd most favorite state

Canadians are the largest foreign buyers in Arizona

Africa, the 2nd largest foreign buyer of Arizona real estate

Our analysis reveals fascinating trends in the U.S. residential real estate market driven by foreign buyers. While China remains a major player, Asian buyers take the lead overall. Florida stands out as the top destination, but California, Texas, and even a surprising North Carolina, all attract significant foreign investment. The data highlights the diverse motivations behind these purchases, with factors like education, investment potential, and proximity influencing location choices.

Ready to explore your U.S. real estate opportunities? Contact us today at [email protected] or schedule a call with our loan officers and schedule a commitment-free meeting with one of our U.S. loan officers to explore your U.S. mortgage options further, you can do so using our 24/7 calendar link. Our team can help you navigate the intricacies of financing your U.S. investment property.

America Mortgages Inc. is a direct lender and leading mortgage broker specializing in financing solutions for U.S. Expats and Foreign Nationals living overseas. We provide access to over 150 U.S. bank and lender programs, delivering tailored mortgage options directly to our international clients. America Mortgages is wholly owned by Global Mortgage Group Pte. Ltd., an international mortgage specialist based in Singapore.