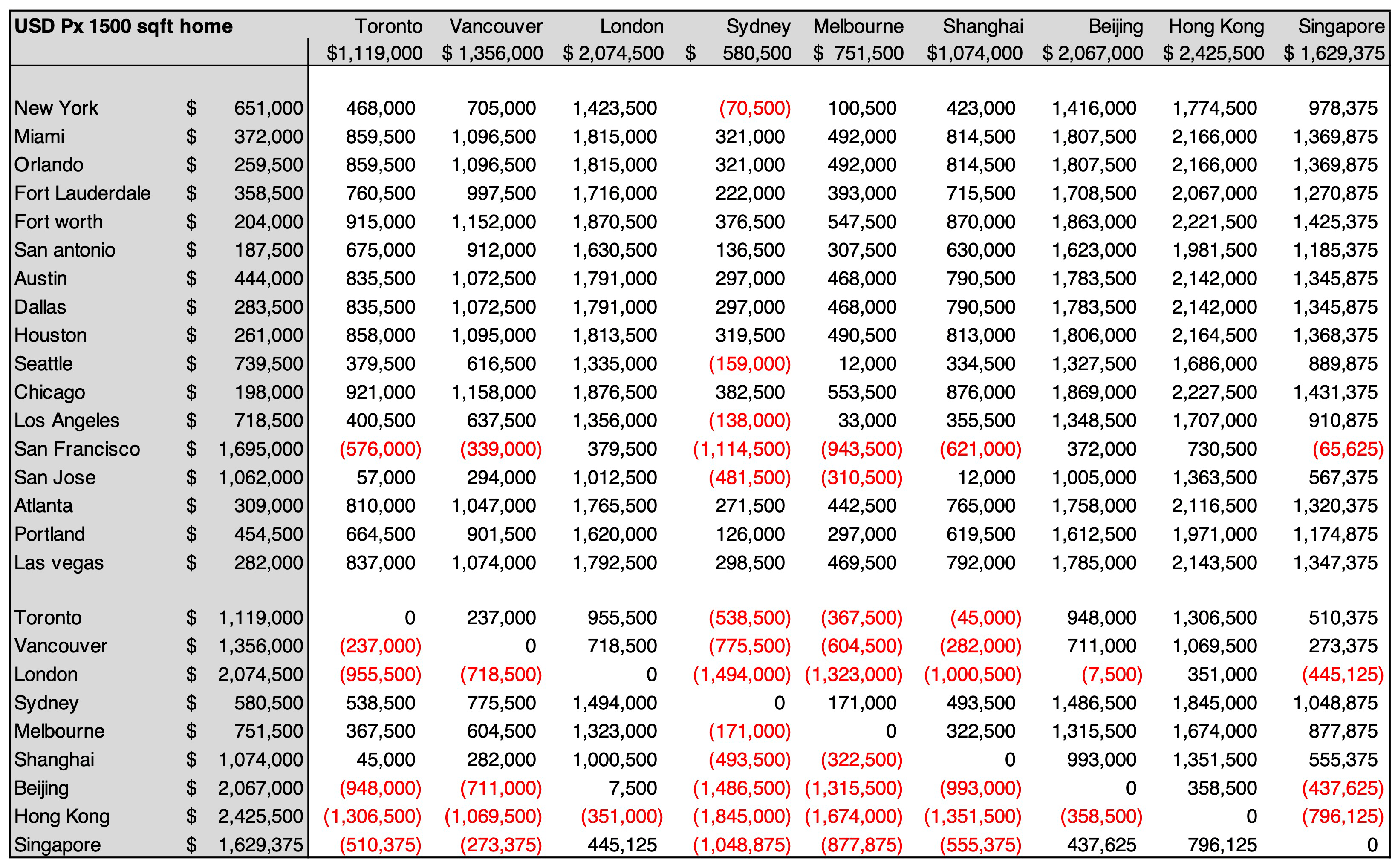

Making a case for U.S. Residential Property Investment

“Let’s Look Under the Hood”

In the previous 2 weeks, we have discussed U.S. real estate investment’s relative affordability and income potential.

In this week’s Deep Dive, we will look at what the Key Drivers of Property Prices are and make an argument on which U.S. cities represent the best projects for future price appreciation.

The utility of owning a home is greater than any other possession – a roof over your head, it provides a sense of security for present and future generations, the sense of incredible accomplishment that “I have MADE IT in life,” and the list goes on.

However, as an investment, we need to think about its ability to produce income (dividends/rental income, etc.) and future price appreciation.

We start this discussion by digging into what factors drove property prices in the past, what ‘new’ factors exist today, and (drumroll….) we will try to take a stab at where they will be in the future.

We will also introduce a new proprietary index: AM Job Prospect Index

First, what drives property values up?

This is a vast topic that can get very granular – see below for a snapshot of a 2019 article written by the New York Fed about Forecasting Home Prices.

But we will try to keep it simple.

Liquidity is plain and simple. The world has seen an unprecedented fiscal stimulus and monetary easing over the past 20 years.

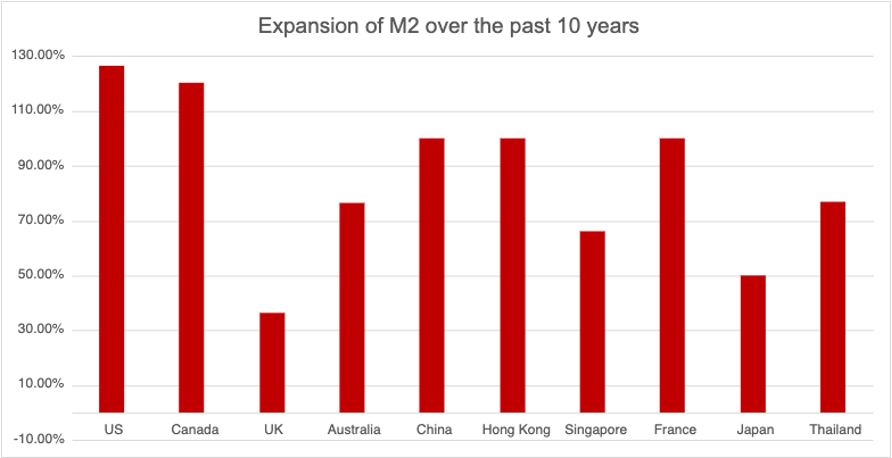

A commonly accepted money base is M2 (Money in circulation, checking deposits, and savings deposits less than $100K).

Let’s look at M2 money supply over the past 10 years. You can see the amount the U.S. has grown its money base dwarfs any other country, and in fact, it is 4x the growth rate of the U.K. In absolute terms, the current M2 supply in the U.S. is almost twice that in Japan.

Now that we have identified the global macro drivers, we can look into where the money is flowing into – specifically real estate and, more importantly, why.

It’s not surprising that the top 5 states in terms are GDP are:

| California | Texas | New York | Florida | Illinois |

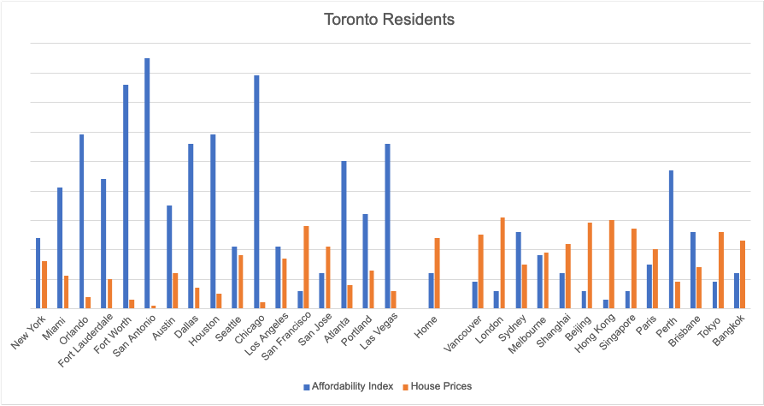

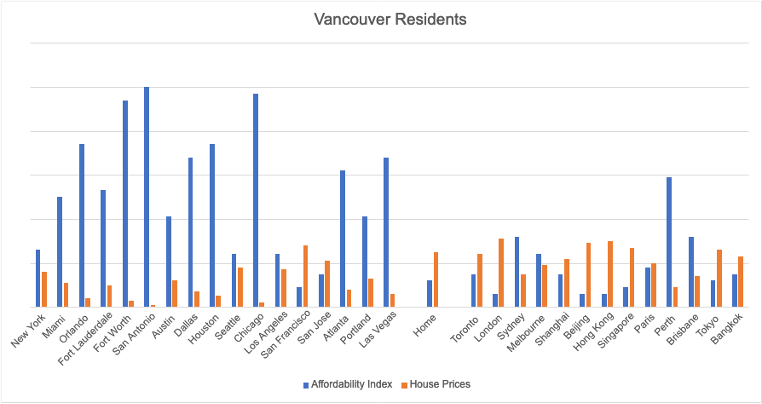

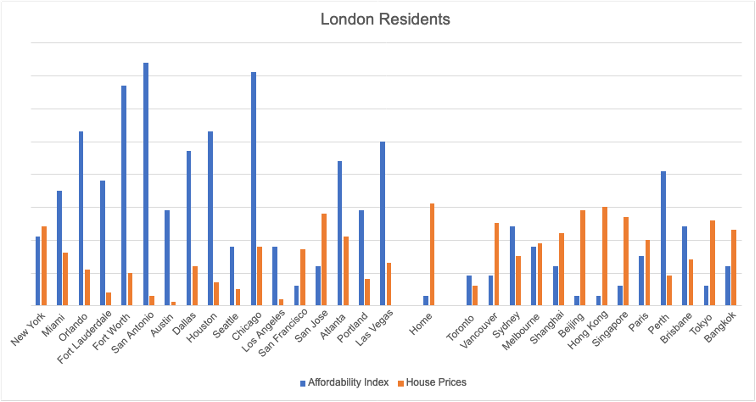

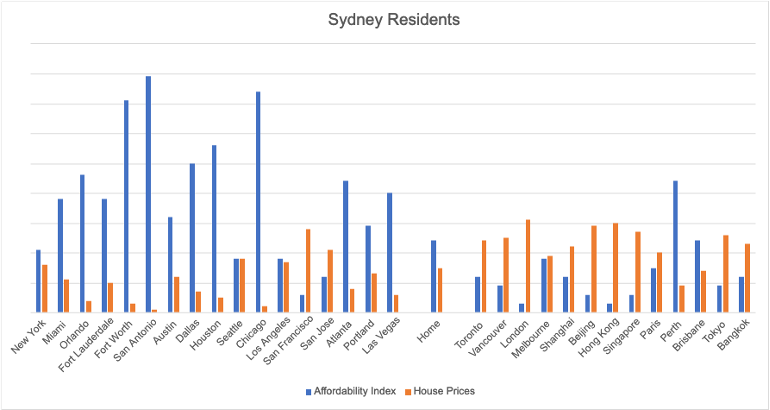

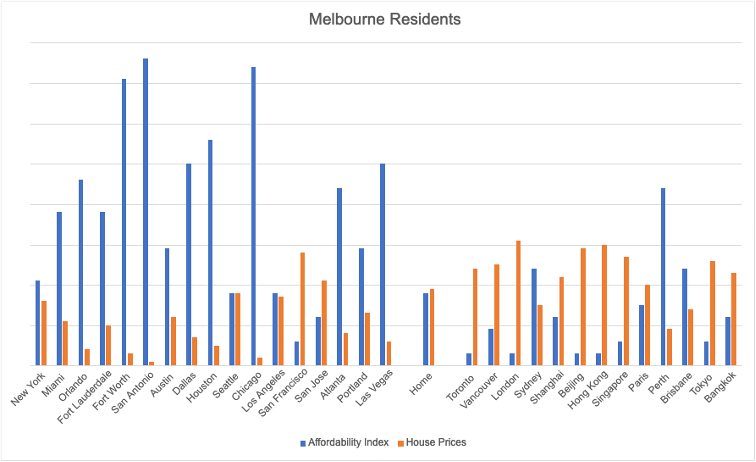

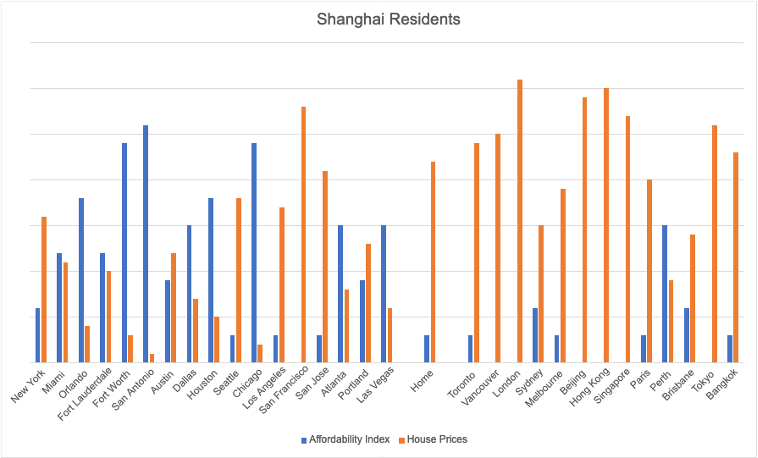

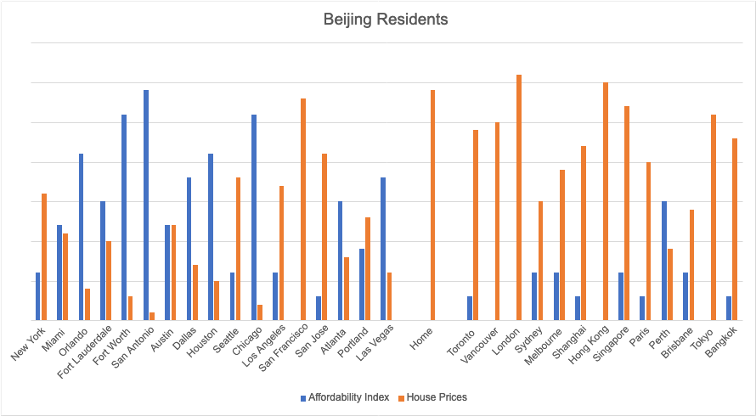

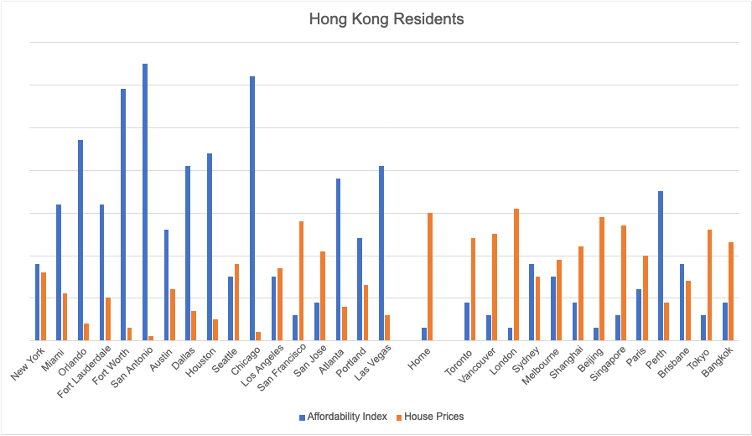

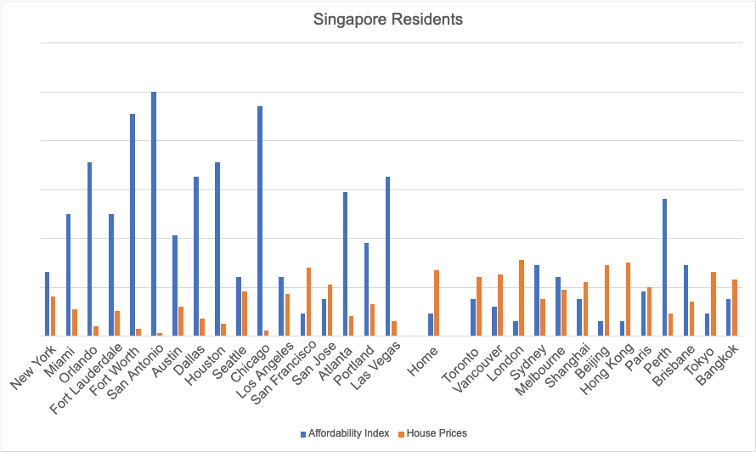

This is consistent with our most popular destinations for real estate investments (see below).

Within this context, we take another cut at the data and look at which cities in those states represent the highest contributors to the overall national economy:

Here are the cities with over 2% contribution to U.S. GDP:

| New York City (8%!) | Miami | Fort Lauderdale | Fort Worth | Dallas | Houston | |

| Seattle | Chicago | Los Angeles | San Francisco | Atlanta | ||

Now we look at cities with the highest GDP growth rates (over 1% y-o-y growth 2018-2019):

| Seattle | Los Angeles | San Francisco | San Jose |

| Austin | San Antonio | Portland | |

You can see that these cities naturally are attractive given the size of the economy; hence the probability of finding meaningful employment is higher. Now, the list likely looks much different 2020-2021, which I’m guessing will magnify the growth potential in the Texas cities even more!

Next, we will look at why these cities.

We have identified 3 main factors that raise the demand for properties in an area – 1) Economic prospects, 2) Gentrification 3) The China Effect

1) Economic prospects

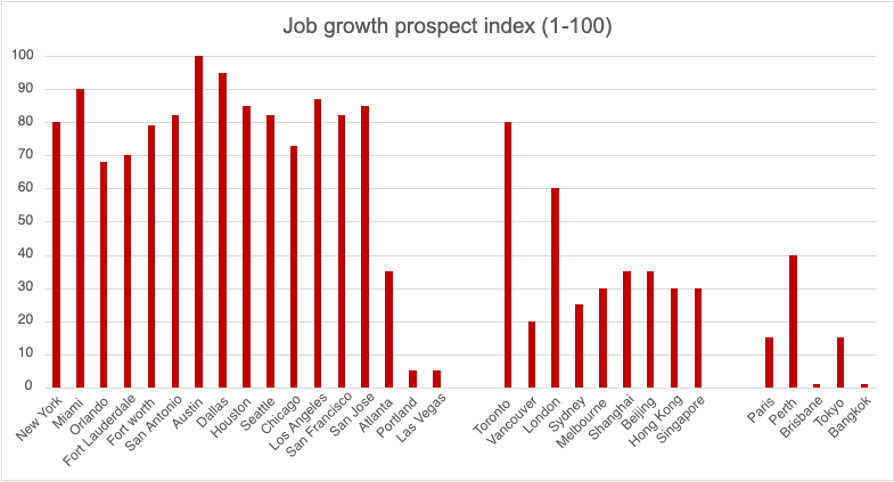

AM Job Prospect Index

Our multifactor algorithm includes factors like the number of big companies moving to these cities, market capitalization of the new companies, new headquarter size, etc.

Using our “AM Job Prospect Index, in general, job prospects of U.S. cities appear to be better than other global cities. The average job prospect index for the U.S. is 70, but only 30 for other cities (the higher, the better). In the U.S., cities with the best job prospects are Austin, Dallas, Miami, Los Angeles. Austin, TX specifically, has the highest value as numerous big companies are setting up headquarters there– Tesla, Google, Amazon, SpaceX are just a few. Tesla’s new manufacturing plant in Austin alone will hire more than 10,000 through 2022. We can expect plenty of people to move to these cities, meaning increased demand and elevated home prices in these areas.

2) Gentrification

Gentrification is the process of changing the character of a neighbourhood through the influx of more affluent residents and businesses. When wealthier residents move into a neighbourhood, they often renovate homes, making them more aesthetically appealing and equipped with better facilities, which increases the value of the property. The addition of new and more “hip” businesses in the city also aids in job creation and can attract more people, increasing the demand and prices of homes.

According to the NCRC Research report, taking into account the number of neighborhoods gentrified and the intensity of gentrification, New York, Los Angeles, San Francisco, Houston, Austin, Miami are the most gentrified cities in the U.S. (arranged in order). Therefore, we can expect home prices to appreciate in these cities.

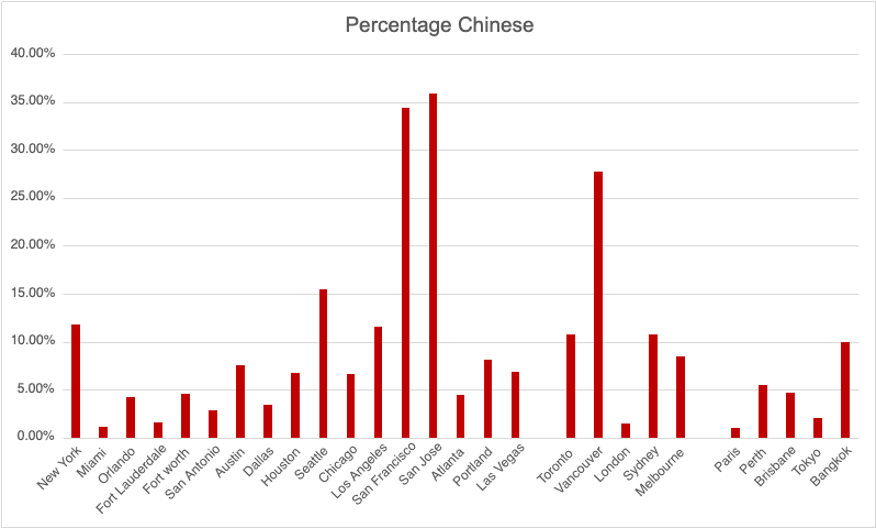

3) The China Effect

Instead of the usual demographic factors like immigration, we’ll look at the percentage of the population who are Chinese. Why do we do so? China has experienced rapid growth in recent years, and its people have gained a significant amount of wealth. It’s no surprise that according to the National Association of Realtors annual report of International Buyers of U.S. residential real estate, China was ranked #1 for the past 5 years.

Excluding predominantly Chinese cities, we see that the average percentage of Chinese the U.S. cities (9.85%) is higher than those in other major cities (8.25%). Thus, we can expect Chinese investors to be more inclined towards U.S. cities, demanding more houses and driving up prices in U.S. cities more than other cities. They will typically choose areas with a significant Chinese population as it offers a sense of familiarity. U.S. cities with the highest percentage of Chinese population are Los Angeles, San Francisco, New York, Seattle.

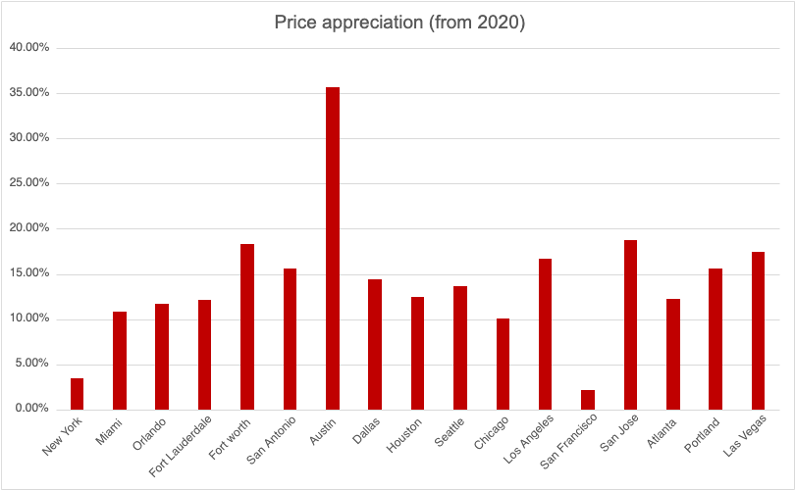

Based on the abovementioned factors and looking at the “top performers” in each category, prices will likely appreciate the most in Texas, Los Angeles, Miami. This is also in line with the price appreciation data provided by Case-Shiller Home Price Index and Zillow. Prices appreciated by 35.07% in Austin last year!

In summary, the conclusions in this report are consistent with our previous 2 reports. There is a tremendous amount of value in the Texas cities, with its abundant jobs, high wage growth, low taxes, easy of travel, strong ethnic mix, and the list goes on.

New York will always have a premium, and Los Angeles and San Francisco will always have specific attributes which make them unique.

HOWEVER, the high cost of living, home prices, and state taxes are quickly driving residents to other states. Almost every metric we see supports this argument. Gentrification in the U.S. is real and is happening much faster than we can imagine. Just look at new home sales from the largest home building company Lennar. They cannot sell enough homes, and it’s the Gentrification Effect we discuss above.

One area that the U.S. has lagged behind its low-cost international peers over the past 10 years is the vocational workforce – smartphone manufacturing, assembly, etc. This was a growth engine in the 80s before the Japanese began their auto manufacturing dominance. But slowly, the U.S. economy retooled and prospered again. Then in the early 2000s, the steel industry lost millions of jobs to low-cost manufacturers overseas, and those jobs have not returned.

The current trend of technology companies moving major offices inwards (See Texas) not only helps the local economies but it reflects a bigger theme – vocational employment. It may not be assembling smartphones, but it will be something else – smart cars, smart cities, smart grids, distribution centers, cloud kitchens, drone deliveries, and so on. Technology is clearly the growth driver going forward, and if you are thinking of real estate as an investment, you should look at states that offer this type of value. Right now, it is clearly Texas, and I suspect there is still more room to go here.

In next week’s Deep Dive, we will be bringing in a U.S. Tax Accountant who focuses specifically on U.S. Expats to explain how the tax regime on owning U.S. property is not as bad as you think and, in fact, could be the easiest and most flexible in the world!

Keep your eyes peeled and subscribe to our newsletter, so you don’t miss out! www.americamortgages.com