When you acquire a mortgage, the lender divides the repayment schedule into several monthly installments over a fixed period. Amortization is the process of spreading out the mortgage over multiple years and into a series of fixed payments. The total mortgage amount, including the principal balance and interest, is supposed to be paid off with the last installment.

As a borrower of an amortized mortgage, you need to repay a specified monthly amount that pays off a portion of both the principal and interest. After every installment, the total loan balance decreases and finally gets paid off with the last payment.

For example, if you obtain a $20,000 amortized mortgage for five years, the lender will divide it into 60 monthly installments, including the principal and the interest amounts. Presume you need to pay approximately $377 per month and respectively $294 and $83 go into squaring off the principal and interest. Then, it will be $295 and $82 respectively in the next month. Over the loan term, the amount of principal payment will increase, and the interest will decrease (although the monthly installment will be the same).

At America Mortgages, you can enjoy an amortization period longer than the mortgage term in the case of commercial loans. For instance, if you take a loan for ten years, the amortization period could be 30 years meaning the monthly installment amount will be similar to a 30-year loan.

If you are to repay this amount over 120 months at $1,000 per installment, the rate will continue for 119 months. In the last month, you will pay the remaining balance ($81,000 in this case) by one balloon payment.

Amortization is available on fixed-rate mortgages and home equity, personal, and auto loans. You won’t get this facility on credit cards and interest-only loans.

Assets refer to a wide variety of items you own that have a monetary value. When you apply for a mortgage, the lender looks into your asset inventory and determines their cash value to make sure that you are capable of returning the loan despite facing financial hardship, such as a job loss, during the repayment period.

There could be various asset types, including: ● Money, savings and checking accounts, certificates of deposit (CDs), and other similar sources — cash and equivalent to cash ● Tradable stocks, bonds, or something that can be converted to cash without dropping their actual price — liquid assets ● Lands, vehicles, antiques, business property, and anything that has monetary value but cannot be converted into cash quickly and may lose some of their value in the conversion process — fixed assets ● Investment money that is lent for interest, including government bonds, securities, and any type of investment money that yields interest — fixed-income assets ● IRA, 401(k) accounts, mutual funds, or anything that secures your ownership in a company — equity assets

You can also categorize them into tangible (physical) and intangible (nonphysical) assets. The lender assesses your positive net worth, indicating your assets have more value than your liabilities. It also helps establish your debt-to-income ratio.

As a U.S. real estate investor, investment mortgage loans can be very beneficial to you. America Mortgages focuses specifically on these types of mortgage loans. There are several programs on hand that make it possible for borrowers to get a mortgage to invest in real estate.

Some of them are better than others, but they can all help you out in some way. If you are considering getting a mortgage, here are a few advantages that you can get from an investment mortgage loan.

Advantages

Use other people’s money – The biggest advantage of using investment mortgage loans is that you get to use other people’s money. Many financial experts have said that you should use other people’s money whenever you can. When you get a mortgage, you only have to put up a certain percentage of the property’s money, but you still get to benefit from owning the whole property. You get to take advantage of the property’s appreciation, and you get to use it for whatever you want. This allows you to hang on to your capital and use it for other investments.

Reasonable interest: With most mortgages, you will be able to get a very affordable interest rate as long with or without a U.S. credit score (FICO). When you get a low-interest rate like you can with an investment mortgage, it can save you a substantial amount of money. For the cost of the loan, it is usually well worth it to get a mortgage instead of using your funds. Hang on to your cash and use it towards additional investments.

Easy approval: With an investment mortgage, you will usually be able to tell whether you are approved relatively quickly. America Mortgages has pretty cut and dry standards when it comes to getting you approved for an investment mortgage. America Mortgages has loan programs for U.S. Expats with or without U.S. credit. We understand that living abroad often changes factors and your ability to borrow in the U.S. Our loan programs are tailored towards your exact situation.

Not a U.S. citizen, Foreign National, or considering relocating abroad for work or school? We can help. Our Foreign National / Non-U.S. citizen mortgage loans were created for these situations. Qualify with No U.S. credit. No U.S. residency. No income verification. It’s not simple, but we have it down to a science with our expertise in this market. You will know where you stand and if you will qualify within a reasonable amount of time.

Increase your reach: With the use of investment mortgages, you can increase your investment power. As you grow, you can keep buying more and more property. In Asia, where property prices have increased, and square footage and yield have decreased, finding an affordable investment outside your home country makes sense. Many people would not be able to purchase property otherwise as it usually takes a significant investment. You can keep picking up more and more stuff as you go.

Build your net worth: Hong Kong, Singapore, Shanghai, and other large Asian cities have cooling measures to stabilize a fast appreciating Real Estate market mainly due to outside investment and the lack of affordable Real Estate options. Being able to build your net worth on a global scale gives with a reasonable mortgage loan that eventually you will have all of the property paid off gives you the same opportunity as anyone else regardless of your passport. You are free to do what you want with all of the property. If you had to rely on your funds for all of this, much of it would not be possible.

The Verdict

Using an investment mortgage can be a great way to get involved in the real estate investment market. Many people have gained considerable amounts of wealth through the use of real estate investment. Therefore, if you are considering getting involved in the field, you should definitely take advantage of investment mortgages. The advantages that you will receive as a result of using them will help you in a number of ways. If you can qualify for one, it makes a lot of sense financially. America Mortgages’ primary focus is helping non-U.S. citizens and Expats obtain prime, quality investment mortgage loans not only in the United States but on a global scale.

This client was the General Manager of the top luxury hotels in Toronto. Like any hotelier, he’s been away from home since his university days.

How We Helped

Our client had a decent FICO score for someone that’s been away from home for 30 years. That’s because he has used his only credit card regularly for the past 20 years. However, his breadth of credit was not sufficient to carry a mortgage.

We put our client on a 3-month Credit Enhancement Program where our team walks you through a specific process to build, maintain and strengthen your credit profile.

Our client has a FICO score of over 800 and qualified for the cheapest ‘Prime” loan available.

Loan Details

Nationality

Property Value

Loan Amount

LTV

Rate

U.S. Citizen

$335,000

$268,000

80%

3.35%

Term

State

Property Type

Purpose

Loan Type

30 year fixed

Austin, Texas

Single-Family Residence (SFR)

Purchase

Residential

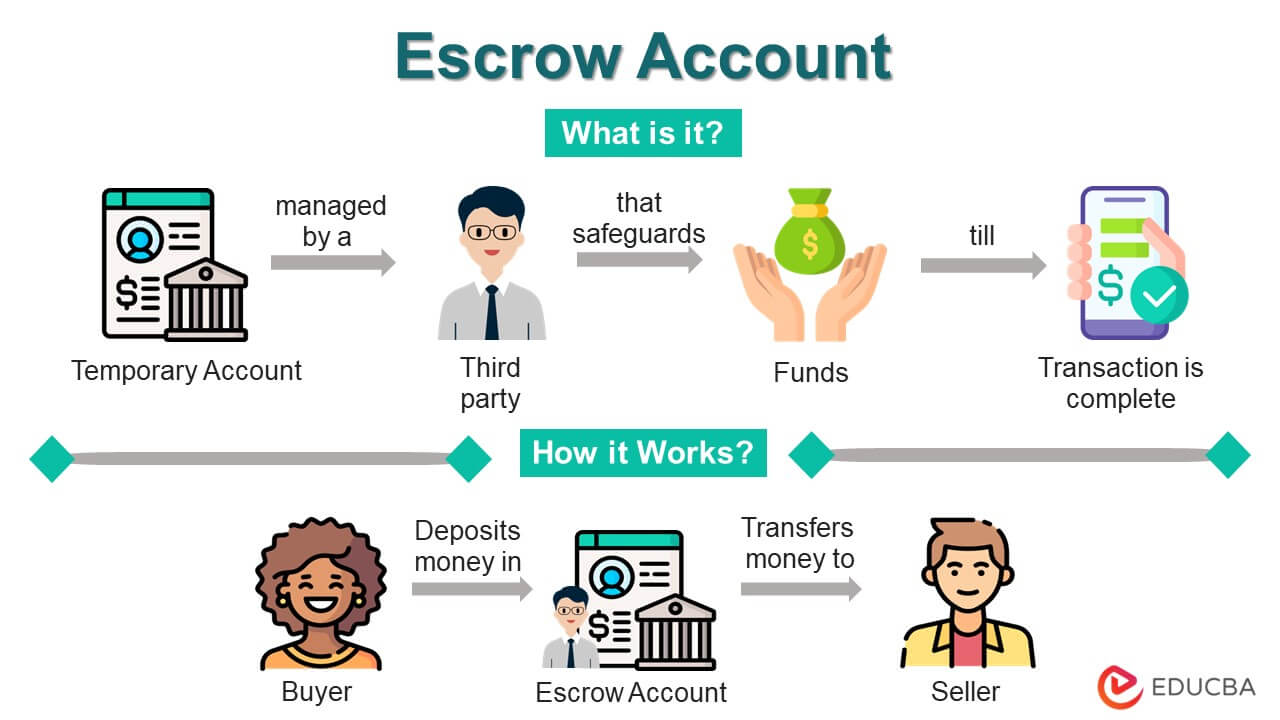

Escrow is one of the most important concepts in real estate transactions, yet many first-time homebuyers are unfamiliar with how it works. Whether you are purchasing a property, making an earnest money deposit, or managing property taxes and insurance through a mortgage lender, an escrow account helps ensure that funds are handled securely and released only when specific conditions have been met.

Understanding escrow can help buyers and homeowners navigate the homebuying process with greater confidence and avoid surprises during a real estate transaction.

What Is Escrow?

Escrow refers to a financial arrangement in which a neutral third party holds funds, documents, or assets on behalf of two parties involved in a transaction.

The escrow agent may be an escrow company, title company, attorney, or another authorized third party. Their role is to safeguard the funds and ensure that all agreed-upon terms have been satisfied before money is released.

Escrow is commonly used in real estate transactions because it helps protect both buyers and sellers. However, escrow accounts may also be used in other situations where funds need to be securely held until contractual obligations are fulfilled.

How Does an Escrow Account Work?

A third-party holding account acts as a secure place to store funds during a transaction.

For example, when purchasing a home, a buyer often submits an earnest money deposit to demonstrate a serious intention to purchase the property. Instead of giving these funds directly to the seller, the money is placed into escrow.

The escrow agent holds the funds until all conditions of the purchase agreement have been met. Once the transaction successfully closes, the funds are released according to the terms of the agreement.

If certain contractual conditions are not satisfied, such as a failed home inspection or appraisal contingency, the buyer may be entitled to receive the deposit back depending on the terms of the contract.

Why Is Escrow Important in Real Estate?

This arrangement helps create trust between parties involved in a transaction by ensuring that funds are protected throughout the process.

Some key benefits include:

Protection for buyers and sellers

Secure handling of funds

Reduced risk of fraud

Verification that contract conditions have been satisfied

Improved transaction transparency

Timely payment of property-related expenses

Because real estate transactions often involve significant sums of money, escrow serves as an important safeguard for everyone involved.

During the Home Buying Process

For many homebuyers, the first interaction with escrow occurs when making an earnest money deposit.

This deposit demonstrates a commitment to purchasing the property and is generally held by a neutral third party until closing.

In some situations, buyers may be able to recover their earnest money if specific contingencies outlined in the contract are not satisfied. Examples include:

The property appraises below the purchase price

Significant issues are discovered during a home inspection

Financing cannot be secured under approved contract conditions

The exact terms vary depending on the purchase agreement and local regulations.

Managing Taxes and Insurance Payments

This process continues to play an important role even after a home purchase has been completed.

Many mortgage lenders require borrowers to maintain an escrow account for property-related expenses. Each month, a portion of the mortgage payment is deposited into the escrow account along with principal and interest payments.

The lender then uses these funds to pay:

Property taxes

Homeowners insurance premiums

Flood insurance premiums (if applicable)

Because insurance costs directly affect the amount collected in the account, it’s important to understand homeowners insurance and its role in the mortgage process.

Account Shortages and Overage

Property taxes and insurance premiums can change over time. Because of this, lenders perform an annual escrow analysis to determine whether the account contains enough funds to cover future expenses.

An escrow shortage occurs when there are insufficient funds available to pay projected expenses.

An escrow overage occurs when more funds than necessary have accumulated in the account.

Following the annual review, the lender will typically send a statement outlining the account status and any required payment adjustments. In some cases, excess funds may be refunded to the homeowner. Homebuyers can learn more about escrow requirements through resources provided by the Consumer Financial Protection Bureau (CFPB).

Benefits of This Arrangement

These accounts provide several practical advantages for homeowners and buyers.

Benefits include:

Simplified budgeting

Automatic payment of taxes and insurance

Reduced risk of missed deadlines

Greater transaction security

Improved financial organization

Peace of mind during the homeownership process

For many borrowers, escrow offers a convenient way to manage recurring housing expenses throughout the year.

Summary

Escrow plays a critical role in both real estate transactions and ongoing mortgage management. By using a neutral third party to hold and distribute funds, escrow helps protect buyers, sellers, lenders, and homeowners throughout the process.

Whether you are purchasing your first home or managing an existing mortgage, understanding how escrow works can help you make more informed financial decisions and navigate the homeownership journey with confidence.

Frequently Asked Questions

Q1. What does escrow mean?

A: Escrow is a financial arrangement in which a neutral third party holds funds or assets until all conditions of a transaction have been completed.

Q2. Is this type of account required for every mortgage?

A: Not always. Some lenders require escrow accounts, while others may allow qualified borrowers to waive escrow requirements under certain conditions.

Q3. Who manages the account?

A: Escrow accounts are typically managed by escrow companies, title companies, attorneys, or mortgage lenders depending on the stage of the transaction.

Q4. What happens if there is a shortage?

A: If an escrow shortage occurs, the lender may increase monthly payments or require an additional payment to cover the difference.

Q5. Can I remove escrow from my mortgage?

A: Some lenders allow escrow waivers for qualified borrowers, although specific requirements vary by lender and loan program.

Q6. Does money in the account earn interest?

A: This depends on state laws and lender policies. Some escrow accounts may earn interest, while others do not.

The Client

Our client was a former doctor at John Hopkins but moved back to Edinburgh, Scotland. He saw firsthand the number of international students applying to the university and the lack of housing.

How We Helped

Our client identified a cash-flow positive property that was currently rented to students. As he used to live and work in the U.S., he assumed he could call the local bank he used while living in the U.S. Even though he still maintained a checking and savings account with the local bank in Baltimore, they were unable to offer him a mortgage for the purchase. He came across our company online, was pre-approved in one week, and closed the transaction within a month.

Loan Details

Nationality

Property Value

Loan Amount

LTV

Rate

U.K. Citizen

$810,000

$567,000

70%

6.125%

Term

Address

Property Type

Purpose

Loan Type

Home use

5/1 ARM

Baltimore, Maryland

Three-unit triplex

Purchase

Residential

Rental apartments for International Students

The Client

A married Singaporean couple in their early 70s living in Singapore with a small portfolio of U.S. investment property. The wife works and owns a small marketing company while the husband is retired. In addition to their home, the pair also own two rental properties.

How We Helped

On advice from their trusted attorney, they were also hoping to increase their LTV to mitigate U.S. inheritance tax and convert their current rental mortgage into an interest-only to increase their yield.

The property was an impressive six-bed family home in Vail, Colorado. The couple had purchased the house over 20 years ago when living and working in the U.S.

The pair were looking to reduce their credit card debt and help their son purchase a home in Singapore.

In total, they were looking to raise $300,000. They had requested a five-year fixed rate on interest-only terms. The clients felt that their advanced age and low income would decrease the finance options available.

The clients were not current on their U.S. tax filings for their rental property, were in their late 70s, and had sufficient but not well-documented income.

As a significant amount of their income was based on future contracts, but their cash-flow was sufficient to service their debt, we suggested our FNStated program, enabling the borrowers to qualify for a higher LTV based on projected income and net rental income from the property.

Age wasn’t a factor, as it is illegal to discriminate against age in the U.S. America Mortgage was able to structure a 30 year amortized mortgage with a 5-year interest-only period giving the needed $300,000 cash in hand and reducing their monthly debt servicing by 13%, thus increasing their yield.

Loan Details

Nationality

Property Value

Loan Amount

LTV

Rate

Singapore Citizen

$1,600,000

$323,000

20%

5.75% interest only

Term

Address

Property Type

Purpose

Loan Type

10/1 ARM

Vail, Colorado

Single-Family Home

Purchase and Refinance

Residential

An appraisal is simply an ‘official’ assessment of a property value. It is an integral part of a home-buying process since the mortgage lender expects the correct valuation of the property you will be purchasing.

When you apply for a loan for buying a house, the mortgage lender will require a report from the appraiser about the market price or a possible selling price of that house. These will be ordered by America Mortgages at the Processing Stage of your loan – on your behalf and will be the only time we will ask for any form of payment.

It’s a rough estimate that the lender uses to determine the mortgage rate. The principal or loan amount will be lower than the appraised value of the property. America Mortgages loans out 75% (for Foreign Nationals) to 90% (for U.S. citizens) of a home’s appraisal value.

The appraisal must be done by a person or an organization with the required licenses in that jurisdiction.

A licensed professional appraiser will work without any bias and make sure that the estimation is fair. When the lender requests the appraisal during the mortgage approval process, it will be randomly selected from a panel of reputable companies to ensure an unbiased opinion.

So, what features of the house matter to the appraiser? Some people have the misconception that eye-catching decoration and luxurious furniture increases the price. In fact, these things add value during other steps of home buying and selling, not in the appraisal process.

A home’s value will depend on its current condition, square footage, number of bedrooms, location, neighborhood, and a handful of other things. Appraisers will also note the views, which means overlooking a beach, lake, or the city. A property in a prime location or a prestigious neighborhood will qualify for a higher loan than those located in a less desirable area.

Normal appraisals range between $500-800 depending on State and location. If a lender requires a Rental Comparison, it may add $100-200 more.

The Client

Our client is a British Marketing Director living in Hong Kong. He owns 15 small properties in the Atlanta area and wanted to add to his holding in U.S. real estate.

How We Helped

The client needed to release equity from two of his existing properties in Atlanta to get the down payment for the purchase of a new Orlando, Florida property (4 bedrooms, 3 baths, 3200 sq. ft home with a pool).

The main challenge we had was the client was already in contract, and the loan was declined by an international bank two weeks into the process due to DTI (debt to income) issues.

Our Loan Specialists were able to immediately see the issue and discuss the client’s options on affordability. Once it was understood the client intended to use this property as an investment, America Mortgages was able to structure the loan using only the rental income to service the debt. The existing two rental properties were refinanced in sync with the closing of the purchase.

America Mortgages Inc. is a direct lender and leading mortgage broker specializing in financing solutions for U.S. Expats and Foreign Nationals living overseas. We provide access to over 150 U.S. bank and lender programs, delivering tailored mortgage options directly to our international clients. America Mortgages is wholly owned by Global Mortgage Group Pte. Ltd., an international mortgage specialist based in Singapore.