Escrow is one of the most important concepts in real estate transactions, yet many first-time homebuyers are unfamiliar with how it works. Whether you are purchasing a property, making an earnest money deposit, or managing property taxes and insurance through a mortgage lender, an escrow account helps ensure that funds are handled securely and released only when specific conditions have been met.

Understanding escrow can help buyers and homeowners navigate the homebuying process with greater confidence and avoid surprises during a real estate transaction.

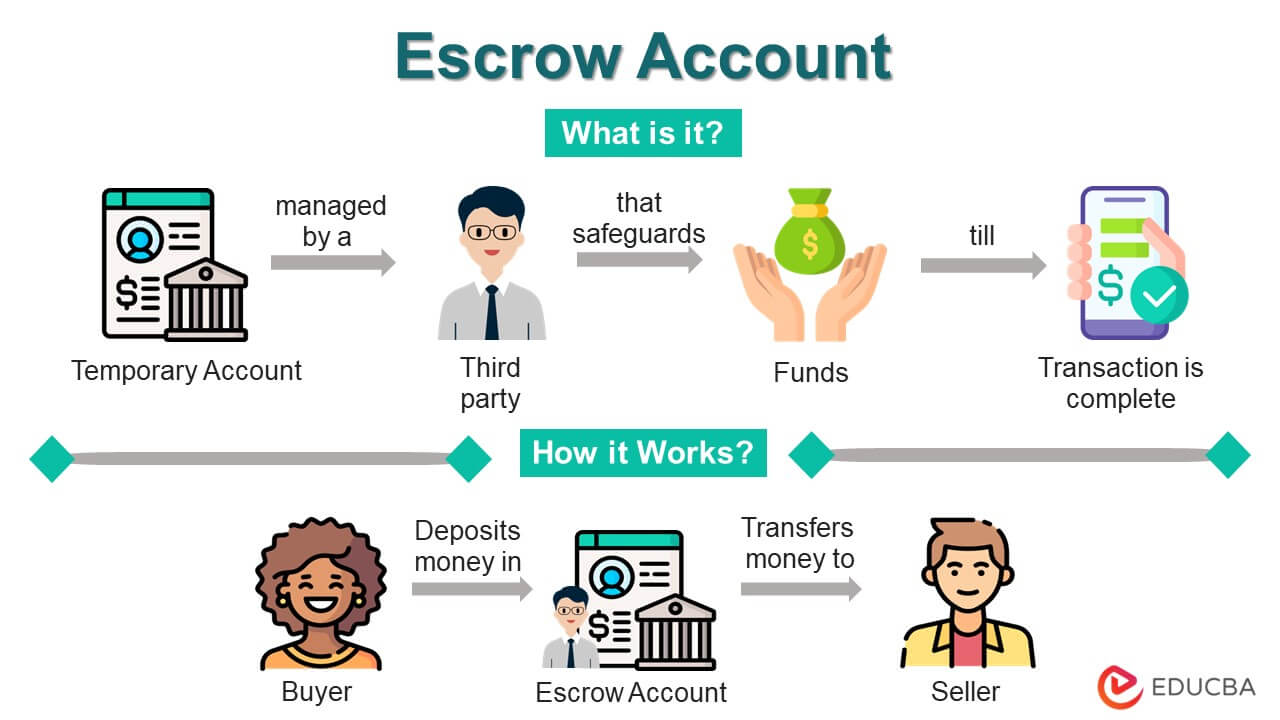

What Is Escrow?

Escrow refers to a financial arrangement in which a neutral third party holds funds, documents, or assets on behalf of two parties involved in a transaction.

The escrow agent may be an escrow company, title company, attorney, or another authorized third party. Their role is to safeguard the funds and ensure that all agreed-upon terms have been satisfied before money is released.

Escrow is commonly used in real estate transactions because it helps protect both buyers and sellers. However, escrow accounts may also be used in other situations where funds need to be securely held until contractual obligations are fulfilled.

How Does an Escrow Account Work?

A third-party holding account acts as a secure place to store funds during a transaction.

For example, when purchasing a home, a buyer often submits an earnest money deposit to demonstrate a serious intention to purchase the property. Instead of giving these funds directly to the seller, the money is placed into escrow.

The escrow agent holds the funds until all conditions of the purchase agreement have been met. Once the transaction successfully closes, the funds are released according to the terms of the agreement.

If certain contractual conditions are not satisfied, such as a failed home inspection or appraisal contingency, the buyer may be entitled to receive the deposit back depending on the terms of the contract.

Why Is Escrow Important in Real Estate?

This arrangement helps create trust between parties involved in a transaction by ensuring that funds are protected throughout the process.

Some key benefits include:

- Protection for buyers and sellers

- Secure handling of funds

- Reduced risk of fraud

- Verification that contract conditions have been satisfied

- Improved transaction transparency

- Timely payment of property-related expenses

Because real estate transactions often involve significant sums of money, escrow serves as an important safeguard for everyone involved.

During the Home Buying Process

For many homebuyers, the first interaction with escrow occurs when making an earnest money deposit.

This deposit demonstrates a commitment to purchasing the property and is generally held by a neutral third party until closing.

In some situations, buyers may be able to recover their earnest money if specific contingencies outlined in the contract are not satisfied. Examples include:

- The property appraises below the purchase price

- Significant issues are discovered during a home inspection

- Financing cannot be secured under approved contract conditions

The exact terms vary depending on the purchase agreement and local regulations.

Managing Taxes and Insurance Payments

This process continues to play an important role even after a home purchase has been completed.

Many mortgage lenders require borrowers to maintain an escrow account for property-related expenses. Each month, a portion of the mortgage payment is deposited into the escrow account along with principal and interest payments.

The lender then uses these funds to pay:

- Property taxes

- Homeowners insurance premiums

- Flood insurance premiums (if applicable)

Because insurance costs directly affect the amount collected in the account, it’s important to understand homeowners insurance and its role in the mortgage process.

Account Shortages and Overage

Property taxes and insurance premiums can change over time. Because of this, lenders perform an annual escrow analysis to determine whether the account contains enough funds to cover future expenses.

An escrow shortage occurs when there are insufficient funds available to pay projected expenses.

An escrow overage occurs when more funds than necessary have accumulated in the account.

Following the annual review, the lender will typically send a statement outlining the account status and any required payment adjustments. In some cases, excess funds may be refunded to the homeowner. Homebuyers can learn more about escrow requirements through resources provided by the Consumer Financial Protection Bureau (CFPB).

Benefits of This Arrangement

These accounts provide several practical advantages for homeowners and buyers.

Benefits include:

- Simplified budgeting

- Automatic payment of taxes and insurance

- Reduced risk of missed deadlines

- Greater transaction security

- Improved financial organization

- Peace of mind during the homeownership process

For many borrowers, escrow offers a convenient way to manage recurring housing expenses throughout the year.

Summary

Escrow plays a critical role in both real estate transactions and ongoing mortgage management. By using a neutral third party to hold and distribute funds, escrow helps protect buyers, sellers, lenders, and homeowners throughout the process.

Whether you are purchasing your first home or managing an existing mortgage, understanding how escrow works can help you make more informed financial decisions and navigate the homeownership journey with confidence.

Frequently Asked Questions

Q1. What does escrow mean?

A: Escrow is a financial arrangement in which a neutral third party holds funds or assets until all conditions of a transaction have been completed.

Q2. Is this type of account required for every mortgage?

A: Not always. Some lenders require escrow accounts, while others may allow qualified borrowers to waive escrow requirements under certain conditions.

Q3. Who manages the account?

A: Escrow accounts are typically managed by escrow companies, title companies, attorneys, or mortgage lenders depending on the stage of the transaction.

Q4. What happens if there is a shortage?

A: If an escrow shortage occurs, the lender may increase monthly payments or require an additional payment to cover the difference.

Q5. Can I remove escrow from my mortgage?

A: Some lenders allow escrow waivers for qualified borrowers, although specific requirements vary by lender and loan program.

Q6. Does money in the account earn interest?

A: This depends on state laws and lender policies. Some escrow accounts may earn interest, while others do not.