Great news! America Mortgages is proud to announce that we are now a direct mortgage lender. Whether you’re a foreign national, U.S. expat, new to real estate investing, or a seasoned investor, this means faster processing times, better rates, and more control over the loan process.

One of our key offerings is our improved cash flow loan, the AM Rental Coverage+ loan program.

How it Works

If you were to buy a commercial building that relied on cash flow, you wouldn’t qualify using your personal income. That just wouldn’t make sense. That is how we look at buying an investment property which has or will have cash flow. That makes sense!

Our rental coverage loan is a straightforward way to evaluate a property’s ability to generate enough rental income to cover its mortgage payments. At America Mortgages, we offer rental coverage loans designed specifically for investors, removing the need for personal income documentation. Instead, we focus on the property’s ability to generate rental income, simplifying the approval process. Common sense underwriting!

How to Qualify Without Showing Personal Income

At America Mortgages, we understand that real estate investors want smarter ways to obtain mortgage financing. The old days of translations of tax returns, conversions of funds, Requirements for a U.S. bank account, U.S. footprint, etc., are no longer required!

Regardless if you’re a foreign national or U.S. expat, the AM Rental Coverage+ loan program gives you the flexibility of fast underwriting, quick decisions and a variety of terms.

What is needed to qualify:

- No income tax returns or pay statements required: Instead, qualification is based on the projected or current rental income of the property using a 1:1 ratio.

- Focus on property income, not personal income: You don’t need to provide proof of personal income, making it easier for foreign nationals and U.S. expats with foreign-earned income.

- No U.S. credit required: If you’re a U.S. Expat, you’ll need to have U.S. credit. If you’re a non-U.S. citizen / Foreign National – No U.S. credit is required!

- Proof of funds: Provide two months of bank or financial statements showing you have sufficient funds for your down payment and closing costs. Foreign banks allowed.

It’s that simple!

Why U.S. Real Estate?

The U.S. real estate market is the largest and the most resilient in the world. Every year, non-U.S. residents purchase a minimum of $50B worth of U.S. residential properties. What do they know?

Here are a few key reasons:

- No Stamp Duty: Unlike many other countries, the U.S. does not impose stamp duty on property purchases, lowering your upfront costs.

- Favorable Tax Laws: The myth that U.S. taxes eat up all property yield is exactly that, a myth. In fact, it is the exact opposite. For U.S. Expats and Foreign Nationals, U.S. tax regulations are designed to benefit real estate investors, including favorable depreciation and deduction rules.

- Ownership Flexibility: Investors can choose to own properties individually or through entities such as LLCs, which provides flexibility in management, liability, and tax advantages.

- Stable Market: The U.S. real estate market remains a reliable investment, known for its stability and long-term growth.

- Top Rental Yields: U.S. real estate offers some of the best rental yields globally, making it an attractive option for investors.

- 30-Year Fixed Loans: The U.S. is one of the only countries that offers 30-year fixed-rate loans, giving investors long-term security and predictability, regardless of the borrower’s age.

- Interest Only: You have the option to choose between a traditional principal and interest loan or the flexibility of an interest-only option fixed for 10 years—a powerful way to optimize yields.

- Low Barrier to Entry: With loan amounts as low as $100,000 and LTVs as high as 80%, anyone can build wealth as a U.S. real estate investor.

What Does This Mean for You?

With America Mortgages now lending, we can provide even better loan options for global investors. Our AM Rental Coverage+ loan program is designed to give you the flexibility and ease you need when investing in U.S. real estate.

Key Loan Program Details:

- Property Type: 1-4 unit properties.

- Minimum Loan Amount: US$100,000.

- Loan-to-Value: Up to 80% for purchases and 70% for cash-out refinances.

- Underwriting: Based on the property’s rental income, with no personal income required.

- Credit Requirements: No U.S. credit required.

- Closing Time: Quick, with closings in 30-45 days.

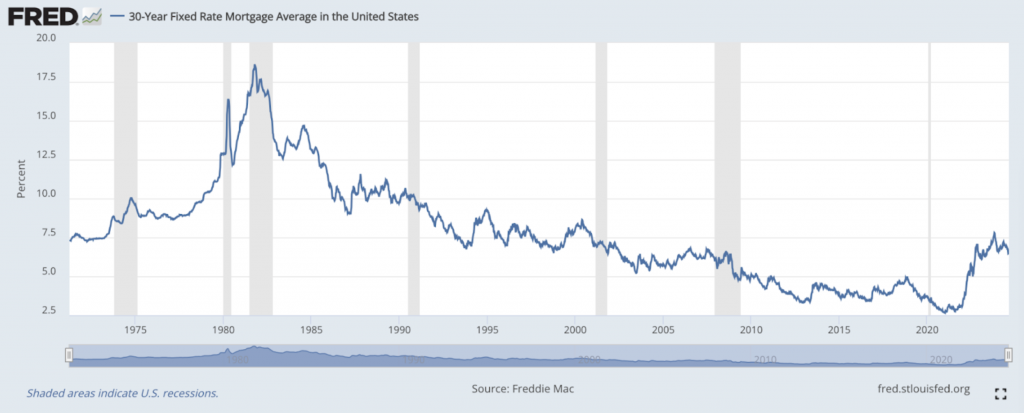

Is Now the Time to Invest or Wait for Further Rate Cuts?

Everyone is aware of the recent 50 basis point cut on September 18th. It’s likely rates may decrease further. If you’re waiting for additional rate cuts, you’ll likely be joining the millions of U.S. owner-occupied borrowers who are also waiting. In our opinion, with America Mortgages’ creative loan programs, very favorable current rates and the fact it is still a “Buyer’s Market”, now is the time to strike. If rates decrease again, it will likely trigger the pent-up demand which has been brewing amongst all buyers. Once owner-occupied and investor buyers flood back into the market, it will likely increase prices, limit availability and turn the market back into a “Seller’s Market”.

America Mortgages has one job – helping foreign nationals and U.S. expats secure U.S. mortgages. To learn more, feel free to contact us at [email protected], visit our website at www.americamortgages.com or if you are ready to apply for a U.S. mortgage, you can use our secure application to apply.

If you’d like to discuss U.S. mortgage loans in more detail, you can reach a U.S. loan officer 24 hours a day, 7 days a week at +1 845-583-0830 or schedule a no-obligation meeting using our 24/7 calendar link.