When foreign nationals are looking to purchase property in the United States, securing a mortgage can feel like a complex and challenging task. The U.S. mortgage system differs significantly from what international buyers may be accustomed to, and without expert guidance, the process can be overwhelming. This is where U.S. loan specialists come in. America Mortgages, a leading lender for foreign national mortgages, understands the intricacies of financing real estate for international buyers. In this article, we’ll explore why working with a U.S. loan specialist is crucial for foreign nationals and how America Mortgages provides a seamless, expert-led experience.

The Challenges Foreign Nationals Face When Securing a U.S. Mortgage

Foreign nationals face unique challenges when trying to secure financing for U.S. real estate, including:

No U.S. Credit History: Foreign nationals may not have a credit history in the U.S., making traditional loan approval more difficult.

Different Tax and Financial Systems: International buyers often have different tax laws, currencies, and financial systems to navigate, which can complicate the loan application process.

Language and Time Zone Barriers: Foreign nationals may have trouble communicating with lenders who are based in different time zones or don’t speak their language.

Why Expertise Matters in Foreign National Mortgages

Working with a U.S. loan specialist who understands the unique needs of foreign nationals can make all the difference. Here’s why:

1. Understanding Complex Financial Documents:

U.S. loan specialists have the expertise to help foreign nationals navigate the paperwork involved in securing a mortgage. They understand how to evaluate foreign income, assets, and credit history, ensuring the application is processed smoothly.

2. Tailored Mortgage Solutions:

Every foreign buyer has different financial goals and investment plans.

Global borrowers need global mortgage expertise

When it comes to securing a mortgage in the U.S. as a foreign national or U.S. expat, expertise matters. America Mortgages specializes exclusively in providing tailored mortgage solutions for individuals just like you—whether you’re looking to purchase, refinance, release equity, or explore bridge and portfolio loans. We understand the unique challenges non-residents face and offer personalized guidance every step of the way. With our dedicated focus on foreign nationals and U.S. expats, we ensure you receive the best options available, backed by deep industry knowledge and a commitment to your success.

Understanding DSCR: How Foreign Nationals Can Use It to Secure a U.S. Mortgage with America Mortgages.

Introduction

If you’re a foreign national looking to invest in U.S. real estate, securing a mortgage might seem like a complicated process. However, with the right guidance and mortgage options, such as the DSCR mortgage, buying U.S. property can be an achievable goal. America Mortgages, an expert lender specializing in foreign national loans, has a wealth of experience in navigating the complexities of real estate financing for non-residents. This article explores what DSCR (Debt Service Coverage Ratio) means, how it works, and why it is a crucial metric for foreign investors securing a U.S. mortgage. Plus, we’ll discuss the importance of working with U.S. loan specialists who understand the needs of international clients.

What is DSCR (Debt Service Coverage Ratio)?

Debt Service Coverage Ratio (DSCR) is one of the most important metrics used by lenders when evaluating the financial viability of a borrower—especially for real estate investments. In simple terms, DSCR measures your ability to cover the debt obligations of a loan (typically through rental income or other revenue generated from the property).

The formula for DSCR is:

DSCR=Net Operating Income (NOI)Debt ObligationsDSCR=Debt ObligationsNet Operating Income (NOI)

For example, if a property generates $100,000 in rental income per year and your debt obligations are $80,000 annually, your DSCR would be 1.25 ($100,000 ÷ $80,000). A ratio greater than 1 means the property generates enough income to cover the mortgage and more.

How Does DSCR Help Foreign Nationals Secure a U.S. Mortgage?

For foreign nationals, securing a U.S. mortgage can be difficult due to factors like a lack of U.S. credit history or income documentation. However, with a DSCR mortgage, the focus shifts away from personal credit scores and income verification to the property’s income-generating potential. This is especially useful for investors looking to purchase rental properties or commercial real estate. Here’s why DSCR loans are a perfect solution for international buyers:

1. Focus on Property Income:

Instead of focusing on the borrower’s credit score, DSCR loans assess the property’s ability to generate income. This is particularly beneficial for foreign nationals who may not have an established U.S. credit history.

2. Flexible Loan Terms:

America Mortgages offers DSCR loan programs that allow for a range of flexible terms, including fixed-rate and adjustable-rate mortgages (ARMs), giving foreign nationals the ability to choose the best option based on their financial goals.

3. No U.S. Credit History Required:

Traditional U.S. mortgages require a good credit score, but for foreign nationals with no U.S. credit history, this can be a major obstacle. DSCR loans, however, are primarily concerned with the income generated by the property, making them an ideal solution for foreign investors.

Why Expertise Matters in Securing a DSCR Loan

Choosing the right lender for a DSCR loan is crucial, especially when navigating the complexities of U.S. mortgage options for foreign nationals. America Mortgages stands out for its deep expertise in offering DSCR loan solutions, helping foreign buyers efficiently secure financing.

1. Specialized Knowledge of Foreign National Mortgages:

America Mortgages is not just another lender; it is an expert in foreign national mortgage products. The company understands the unique challenges international buyers face, from differences in credit systems to the intricacies of U.S. real estate laws. This expertise allows them to offer tailored advice and loan products that are specifically designed for foreign nationals.

2. Understanding Your Investment Goals:

As a foreign investor, your goals for purchasing U.S. property may vary—whether you’re looking for a long-term investment or seeking to generate rental income. America Mortgages takes the time to understand your unique goals and offer personalized financing options that align with your strategy.

3. No Language or Time Zone Barriers:

America Mortgages has loan specialists based around the world, ensuring that you can always speak with someone who understands your needs, no matter where you are. This is especially important for international clients who may have concerns about time zone differences or communication barriers. Whether you’re in Asia, Europe, or the Middle East, America Mortgages is available in your time zone, ensuring seamless communication throughout the mortgage process.

Why Choose America Mortgages for Your DSCR Loan

When choosing a mortgage lender, you want to work with a company that is both knowledgeable and experienced. Here’s why America Mortgages is the best choice for securing a DSCR mortgage:

1. Expert U.S. Loan Specialists:

America Mortgages employs U.S.-based loan specialists who are experts in DSCR mortgages for foreign nationals. They understand the challenges faced by international buyers and work closely with you to ensure you get the best financing options available.

2. Global Reach with Local Expertise:

With specialists in multiple countries, America Mortgages can provide you with the best of both worlds: global reach and local expertise. You’ll be working with U.S.-based professionals who are familiar with the real estate market in the U.S. and can provide specialized advice tailored to your needs.

3. Streamlined Application Process:

America Mortgages simplifies the application process for foreign nationals. With a straightforward online application system and a team that helps you every step of the way, the entire process becomes much easier for international buyers.

Conclusion

Securing a DSCR mortgage as a foreign national can be a game-changer for those looking to invest in U.S. real estate. With the right lender, like America Mortgages, you can navigate the complexities of financing with ease. Their specialized expertise, combined with a global presence and a deep understanding of foreign national loans, makes them the ideal choice for international buyers looking to secure U.S. property. Contact America Mortgages today to explore your options and get started on your U.S. real estate investment journey.

Global borrowers need global mortgage expertise

When it comes to securing a mortgage in the U.S. as a foreign national or U.S. expat, expertise matters. America Mortgages specializes exclusively in providing tailored mortgage solutions for individuals just like you—whether you’re looking to purchase, refinance, release equity, or explore bridge and portfolio loans. We understand the unique challenges non-residents face and offer personalized guidance every step of the way. With our dedicated focus on foreign nationals and U.S. expats, we ensure you receive the best options available, backed by deep industry knowledge and a commitment to your success.

Connect with us today for expert support, and take the first step toward your U.S. homeownership goals. Reach us 24/7 at +1 845-583-0830, via email at [email protected], or on WhatsApp at +1 830-217-6608.

A Guide for Foreign Nationals and U.S. Expats Investing in U.S. Real Estate

Whenever geopolitical tensions rise, global investors begin searching for stability.

Conflicts in the Middle East particularly those involving Iran can disrupt global energy markets, increase inflation, and create volatility across financial markets. During these periods of uncertainty, international capital often moves toward safe-haven assets.

One of the most consistent safe-haven investments over the past several decades has been U.S. real estate.

For foreign nationals and U.S. expatriates, American property offers a unique combination of stability, strong legal protections, rental income potential, and long-term appreciation.

As geopolitical tensions reshape global markets, many investors are asking an important question:

What does a conflict with Iran mean for U.S. real estate and global property investors?

A conflict with Iran can increase global economic uncertainty, particularly through disruptions to oil supply and rising energy prices. These shocks often create inflation and market volatility across financial markets (Source: J.P. Morgan)

During such periods, many global investors shift capital toward stable economies and tangible assets. As a result, U.S. real estate can become more attractive because it offers strong property rights, dollar-denominated assets, and long-term stability for international investors. (Source: The Investor)

Does war increase real estate investment in the United States?

Often, yes.

Historically, geopolitical instability has pushed global investors toward the United States because of its economic stability, strong currency, and deep property markets.

When global uncertainty increases:

• International investors seek stable jurisdictions • Capital moves toward the U.S. dollar • Hard assets like property become attractive inflation hedges • U.S. real estate demand from foreign buyers often rises

This trend has been observed during multiple global events, including the Gulf War, the Iraq War, the Global Financial Crisis, and major geopolitical conflicts.

Why the Iran Conflict Matters to Global Markets

Iran sits near the Strait of Hormuz, one of the most strategically important shipping lanes in the world.

Approximately 20% of global oil supply moves through this narrow waterway.

If tensions disrupt energy supply, oil prices could rise significantly.

However, these same conditions can make real estate more attractive as a long-term store of wealth.

Why U.S. Real Estate Is Considered a Global Safe Haven

International investors often view U.S. real estate as one of the safest property markets in the world.

Several factors contribute to this reputation.

Strong Property Rights

The United States offers some of the strongest legal protections for property ownership globally. Investors benefit from transparent property records, stable courts, and predictable regulations.

Deep Mortgage Markets

The U.S. has the largest mortgage financing system in the world, allowing buyers to access financing options not available in many countries.

Global Reserve Currency

The U.S. dollar remains the world’s dominant reserve currency. During periods of global uncertainty, the dollar often strengthens by making dollar-denominated assets like U.S. real estate particularly attractive.

Housing Supply Shortages

Many U.S. cities face long-term housing shortages, which helps support property values and rental demand.

Best U.S. Cities for International Real Estate Investors

Certain U.S. real estate markets continue to attract significant foreign investment.

These markets offer strong rental demand, population growth, and long-term economic expansion.

Miami, Florida

Miami has become one of the most important international real estate markets in the United States.

Key reasons include:

• Strong demand from Latin American and European investors • Favorable tax environment • Global financial hub status • Luxury waterfront real estate

Miami is often considered the gateway city for foreign real estate investors entering the United States.

Texas: Austin, Dallas, and Houston

Texas continues to attract businesses and residents from across the United States.

Advantages include:

• Rapid population growth • No state income tax • Lower property prices compared to coastal cities • Strong job creation

Houston may see additional benefits if global energy prices increase.

Orlando and Tampa

Florida’s secondary markets are becoming increasingly popular with global investors due to strong rental yields and population migration.

Vacation rentals, long-term rentals, and new development projects continue to drive demand.

New York and Los Angeles

Major global cities often experience renewed interest from international investors during times of geopolitical instability.

Luxury real estate in these cities is frequently used as a long-term wealth preservation asset.

Scenario Analysis: How the Conflict Could Affect Real Estate

Scenario 1: Conflict Ends Quickly

If tensions with Iran resolve relatively quickly, the long-term economic impact on U.S. real estate will likely be minimal.

Possible outcomes include:

• Stabilization in energy prices • Improved global investor confidence • Continued demand for U.S. property

Short periods of uncertainty sometimes create temporary buying opportunities before markets regain momentum.

Scenario 2: Prolonged Conflict

If geopolitical tensions persist for an extended period, several longer-term economic trends could emerge.

Higher Inflation

Energy disruptions may increase inflation globally.

Real estate historically performs well in inflationary environments because property values and rents tend to rise over time.

Slower Construction

Higher material and transportation costs may reduce new housing supply.

Limited supply can strengthen existing property values.

Increased Global Capital Flows

Investors seeking stability may increase their allocations to U.S. assets.

This often includes residential and commercial real estate investments.

Investing in U.S. Real Estate as a Foreign National

Foreign nationals can legally purchase property in the United States even if they are not residents or citizens. This makes the U.S. one of the most accessible real estate markets in the world for international investors.

Many foreign buyers invest in U.S. property for a variety of reasons, including income generation and long-term wealth building. Common investment types include:

• Rental properties • Vacation homes • Long-term capital appreciation assets • Short-term rental investments

Can Foreign Nationals Get a U.S. Mortgage?

Yes. Many international investors finance U.S. property purchases using foreign national mortgage programs. These specialized loan programs allow non-U.S. residents to purchase American real estate without relying on traditional U.S. income documentation.

Typical requirements may include:

• Larger down payments • Asset verification • International credit review • Property appraisal

These financing programs allow investors to leverage their capital while maintaining global liquidity and flexibility across their international assets.

Why U.S. Expats Are Also Investing

U.S. citizens living abroad are also increasingly purchasing property in the United States. Many expats view U.S. real estate as a way to maintain financial ties to the country while building long-term assets.

Common reasons include:

• Building long-term wealth • Purchasing future retirement homes • Generating rental income • Maintaining assets in U.S. dollars

To support these goals, many borrowers use U.S. expat mortgage programs designed specifically for Americans living overseas. These programs allow qualified expats to finance U.S. property while earning income abroad.

The Long-Term Outlook for U.S. Property

Despite periodic economic cycles, the long-term fundamentals supporting U.S. real estate remain strong. Several structural factors continue to support property values and investment demand.

Key drivers include:

• Population growth • Housing supply shortages • Strong domestic demand • Continued international investment

Even during periods of geopolitical uncertainty, these long-term trends continue to support the market. For global investors, this is why U.S. property is widely viewed as one of the most resilient long-term investment assets.

Final Thoughts

Global uncertainty often reminds investors of the importance of stability.

For decades, the United States has provided one of the most stable and transparent real estate markets in the world.

Whether tensions involving Iran resolve quickly or continue longer than expected, the long-term fundamentals supporting U.S. real estate remain strong.

For foreign nationals and U.S. expats seeking stability, diversification, and long-term growth, U.S. real estate continues to stand out as one of the most compelling global investment opportunities.

About America Mortgages

America Mortgages is the Leading Experts in Foreign National and U.S. Expat Mortgage Loans, specializing in U.S. mortgage financing for foreign nationals and U.S. expatriates worldwide. Our team helps international buyers purchase investment properties, vacation homes, and income-producing real estate across the United States while navigating cross-border income documentation, international credit considerations, and underwriting guidelines designed for global borrowers.

To learn more about foreign national and U.S. expat mortgage programs, contact us to speak with a specialist about your situation. You can also reach our team directly by email at [email protected] or by phone at +1 (845) 583-0830 for guidance on financing U.S. property as an international investor.

Frequently Asked Questions

Q1. Does geopolitical conflict usually increase foreign investment in U.S. real estate?

A: Yes. During periods of global instability, investors often move capital into stable economies and tangible assets. Historically, geopolitical tensions have increased international demand for U.S. real estate because of the country’s strong legal system, transparent markets, and stable currency.

Q2. Why is U.S. real estate considered a safe-haven investment?

A: U.S. real estate is viewed as a safe haven because of strong property rights, deep mortgage markets, a stable legal framework, and the global strength of the U.S. dollar. These factors make the U.S. property market attractive to investors seeking long-term security.

Q3. How could rising oil prices affect U.S. real estate markets?

A: Higher oil prices can increase inflation and construction costs, which may slow new housing development. Reduced housing supply combined with continued demand can support property values and rental prices over time.

Q4. Which U.S. cities tend to attract the most international real estate investors?

A: Major global cities such as Miami, New York, and Los Angeles frequently attract foreign capital. Growing markets in Texas, including Austin, Dallas, and Houston, along with Florida cities like Orlando and Tampa, are also popular because of population growth and strong rental demand.

Q5. Can foreign nationals legally buy property in the United States?

A: Yes. The United States allows foreign nationals to purchase residential and investment property without needing U.S. citizenship or residency, making it one of the most accessible real estate markets for international buyers.

Q6. What types of U.S. properties do international investors usually buy?

A: Foreign buyers commonly invest in rental properties, vacation homes, multifamily housing, and long-term appreciation assets located in growing metropolitan areas with strong economic fundamentals.

Q7. Are mortgage options available for non-U.S. residents purchasing property?

A: Yes. Specialized foreign national mortgage programs allow international investors to finance U.S. property purchases. These programs typically evaluate assets, down payment levels, and property value rather than relying solely on traditional income documentation.

Q8. Why are U.S. expats investing in American real estate while living abroad?

A: Many U.S. expats purchase property in the United States to build long-term wealth, generate rental income, maintain assets in U.S. dollars, and secure future retirement or relocation housing.

Q9: Can foreigners buy property in the United States?

A: Yes. Foreign nationals can legally purchase property in the United States without citizenship or residency requirements.

Q10: Is U.S. real estate a good investment during geopolitical conflict?

A: Historically, U.S. real estate has remained stable during global conflicts because investors often move capital into stable economies and tangible assets.

Q11: Can non-residents get a U.S. mortgage?

A: Yes. America Mortgages offers specialized foreign national mortgage programs that allow international investors to finance property purchases.

What Is the European Investment Shift Toward U.S. Real Estate?

The European investment shift toward U.S. real estate refers to the growing trend of capital from Europe moving into American property markets. This shift includes both foreign investors and Americans living overseas who continue to invest in property within the United States.

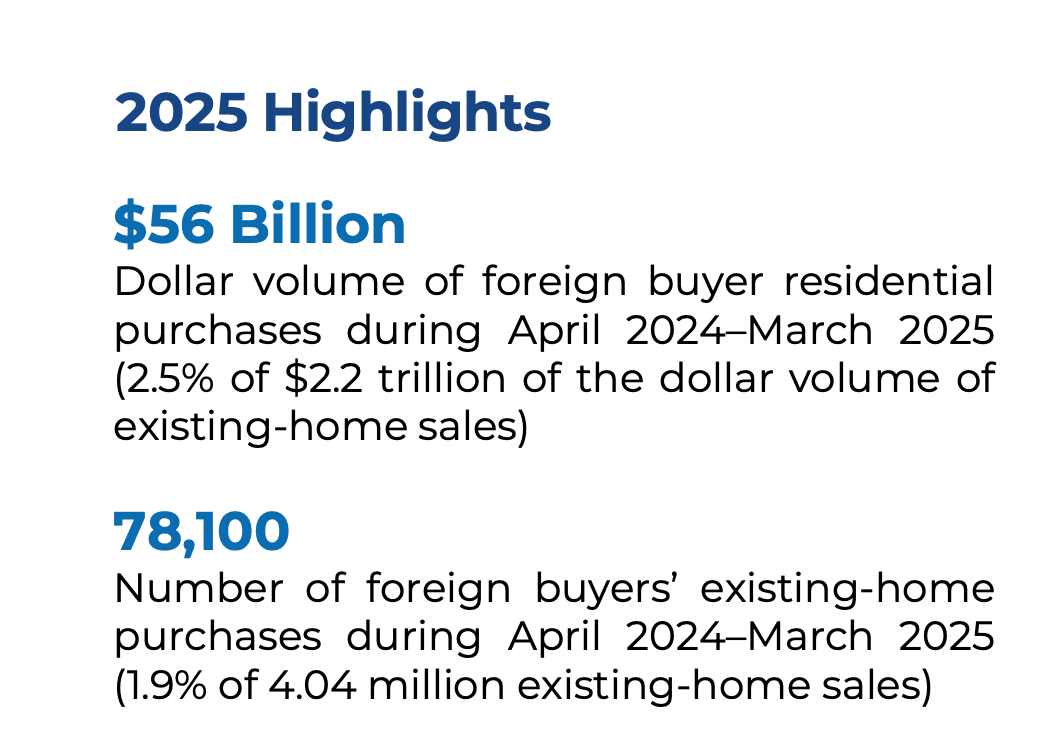

According to the National Association of Realtors international transactions report, foreign buyers purchased approximately $56 billion worth of U.S. residential real estate between April 2024 and March 2025, representing about 78,100 homes. These purchases reflect a broader global pattern in which investors allocate capital toward markets that offer liquidity, transparency, and long-term stability.

Within this trend, the European investment shift toward U.S. real estate is particularly notable because Europe contains both major institutional investors and large populations of American expatriates who maintain financial connections to the U.S. housing market.

Why Is Capital From Europe Moving Into U.S. Real Estate?

The European investment shift toward U.S. real estate is largely driven by economic diversification and the relative stability of the U.S. housing market.

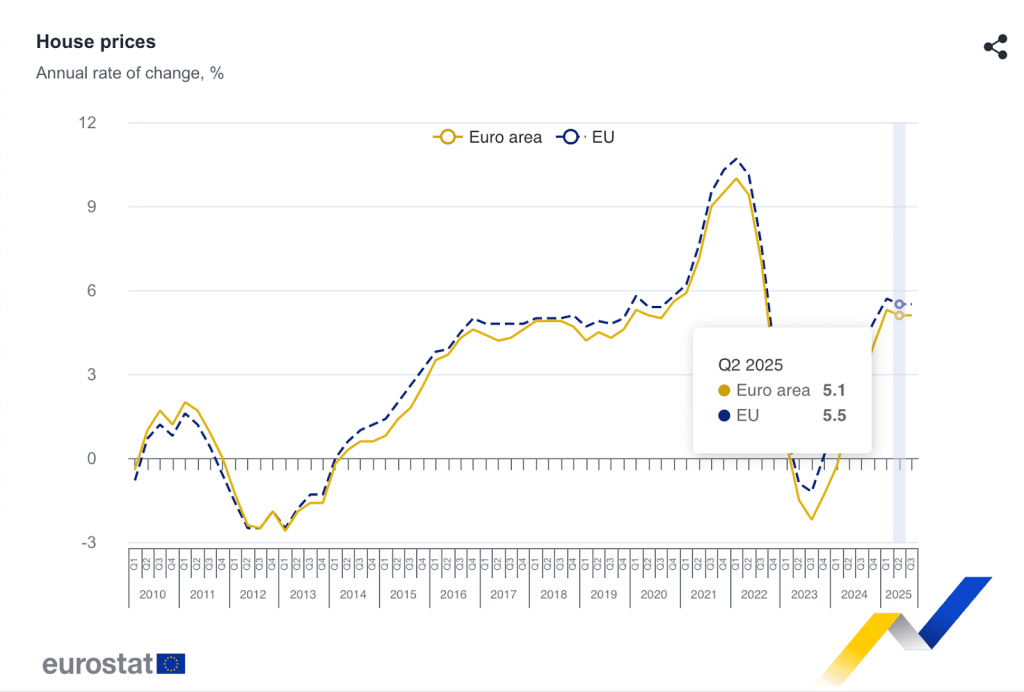

Housing costs across Europe have increased significantly over the past decade. According to Eurostat housing data, residential property prices across the European Union rose 5.5% year over year in 2025, while rental prices have also continued climbing in many urban markets.

At the same time, affordability pressures have intensified. Eurostat reports that a significant share of residents across Europe face housing costs that exceed a large percentage of their disposable income. These pressures have encouraged investors and expatriates to diversify their real estate holdings internationally.

For many investors, the United States offers a unique combination of factors that reinforce the European investment shift toward U.S. real estate. The U.S. market provides deep rental demand, transparent property ownership structures, and access to financing systems that are among the most developed in the world.

Are U.S. Expats in Europe Driving the European Investment Shift Toward U.S. Real Estate?

Yes. One of the most important drivers behind the European investment shift toward U.S. real estate is the population of Americans living abroad.

Millions of U.S. citizens reside overseas, including large communities throughout the United Kingdom, Germany, France, Switzerland, Spain, and the Netherlands. While many of these Americans live and work abroad for years, they often continue to maintain financial ties to the United States.

For these expatriates, purchasing property in the United States serves multiple strategic purposes. Some buyers are planning for an eventual return to the country, while others seek rental income or long-term investment exposure to the American housing market.

This group plays a significant role in the European investment shift toward U.S. real estate because expats typically already understand the U.S. financial system, maintain U.S. tax filings, and often prefer to hold property in a market they know well.

Which U.S. Markets Are Most Attractive to European Buyers?

Several U.S. states consistently attract buyers participating in the European investment shift toward U.S. real estate. These markets offer strong rental demand, economic growth, and global connectivity, making them appealing to both U.S. expats living in Europe and foreign nationals investing in American property.

Florida Florida remains one of the most prominent destinations for European buyers because of its international connectivity, tourism-driven economy, and year-round rental demand. Cities such as Miami, Orlando, and Tampa attract both long-term investors and buyers seeking vacation or second homes.

Arizona Arizona has gained increasing attention among international investors due to strong population growth and expanding technology and logistics sectors. Markets like Phoenix and Scottsdale offer relatively affordable property prices compared to coastal cities while still benefiting from strong rental demand.

California California continues to draw global capital because of the size and liquidity of its real estate markets. Cities such as Los Angeles and San Francisco remain attractive for investors looking for long-term appreciation in major international gateway markets.

New York New York remains one of the world’s most recognized real estate markets and continues to attract European capital seeking stability and global prestige. Investors are often drawn to the city’s large rental market and its status as a financial and cultural hub.

Texas Texas has emerged as a major destination for investors seeking high-growth metropolitan areas and relatively affordable property prices. Cities such as Austin, Dallas, and Houston combine population growth with expanding job markets, making them attractive for long-term real estate investment.

How Do U.S. Expats Living in Europe Finance U.S. Property?

Financing plays an important role in the European investment shift toward U.S. real estate, particularly for Americans living in Europe who earn income overseas but want to invest in property back home.

Many traditional U.S. lenders struggle with international borrowers because they are not structured to evaluate foreign currency income, non-U.S. credit histories, or international tax documentation. As a result, expats often encounter difficulties when applying through standard domestic lending channels.

America Mortgagesspecializes in mortgage programs designed specifically for Americans living abroad. These programs are structured to accommodate international financial profiles while still following U.S. underwriting guidelines.

Key features of expat mortgage programs may include:

Overseas income and credit accepted Salaries paid in foreign currencies and international credit histories can often be reviewed as part of the underwriting process when properly documented.

Up to 80% loan-to-value (LTV) Financing may be available for purchases, refinancing, or equity release depending on the property and borrower profile.

Flexible loan programs Borrowers may choose from 15-year or 30-year fixed-rate mortgages, as well as 5- or 7-year adjustable-rate options, depending on long-term investment goals.

Loan sizes from $150,000 to $5 million Programs are structured to support both entry-level investors and buyers acquiring higher-value properties.

30-year amortization regardless of borrower age This allows expats to maintain long-term financing structures even while living overseas.

Interest-only options available Some programs offer 10-year interest-only structures that later convert to a 30-year principal-and-interest loan, helping borrowers manage cash flow while maintaining rate stability.

For investors purchasing rental property, financing may also be structured around the property itself. Programs such as DSCR loans, explained in this guide on DSCR loans for investment property investors, evaluate the rental income generated by the property rather than relying solely on personal income.

For U.S. expats exploring property purchases from Europe, working with lenders experienced in cross-border mortgage lending can help simplify documentation requirements and provide access to financing programs specifically designed for international borrowers.

Do Foreign Nationals in Europe Also Participate in the European Investment Shift Toward U.S. Real Estate?

While American expatriates represent an important segment, the European investment shift toward U.S. real estatealso includes foreign nationals living across Europe.

Many European investors view U.S. property as a diversification strategy that balances their exposure to domestic housing markets. Rental properties in the United States are often perceived as long-term income assets that can complement investment portfolios containing equities, bonds, or European real estate.

Some international investors also consolidate multiple properties under structured financing arrangements designed for portfolio ownership. A practical example of this strategy can be seen in this portfolio financing case study involving multiple U.S. properties.

Why Is U.S. Real Estate Considered a Global Safe-Haven Asset?

The European investment shift toward U.S. real estate is reinforced by the structural characteristics of the American housing market.

According to the National Association of Realtors existing home sales data, the median price of existing homes in the United States reached approximately $398,000 in early 2026, reflecting the long-term resilience of the housing market despite cyclical fluctuations.

Investors are often attracted to U.S. real estate because of the transparency of property rights, the depth of the mortgage market, and the scale of the country’s rental housing demand. These characteristics create an investment environment that many international buyers view as predictable and stable.

Together, these factors continue to support the European investment shift toward U.S. real estate as part of a broader pattern of global capital allocation.

How Do Investors Move Quickly in Competitive U.S. Property Markets?

Speed can be critical when opportunities appear in competitive markets.

In situations where traditional mortgage underwriting may take weeks, some investors rely on financing structures that prioritize the value of the property itself. Asset-based lending is one such strategy, allowing borrowers to move quickly when acquiring investment properties or development sites.

Explore U.S. Property Opportunities While Living in Europe

For many Americans living abroad and international investors, the European investment shift toward U.S. real estaterepresents an opportunity to diversify globally while maintaining exposure to one of the world’s most established housing markets.

Whether you are considering a rental investment, second home, or long-term property strategy, understanding how financing works for international borrowers is an important first step. Programs designed for U.S. expats and foreign nationals can accommodate overseas income, international documentation, and investment-focused financing structures.

America Mortgagesworks with borrowers worldwide who are exploring U.S. property opportunities from abroad. If you are evaluating potential purchases, refinancing options, or investment strategies while living in Europe, speaking with a lender experienced in cross-border mortgage lending can help clarify the financing structures available to you.

To explore your options or discuss your situation with a U.S. loan specialist, you can visit the our contact page, email the team directly at [email protected], or call +1 (845) 583-0830 to speak with a loan expert. You can also submit your details through the online inquiry form to schedule a consultation and learn more about financing options designed for global borrowers.

Frequently Asked Questions

Q1: Why are European investors buying U.S. real estate?

A: European investors often allocate capital to U.S. property for diversification, rental income potential, and exposure to dollar-denominated assets. The size and transparency of the American housing market make it an attractive destination for global capital.

Q2: Can Americans living in Europe buy property in the United States?

A: Yes. U.S. citizens living abroad can purchase property in the United States and often qualify for mortgages while earning income overseas. Many expats continue filing U.S. tax returns, which helps lenders evaluate their eligibility.

Q3: Do U.S. expats qualify for mortgages while living overseas?

A: Specialized mortgage programs allow U.S. expats to qualify using foreign income documentation, international employment records, and U.S. tax filings. These programs are designed specifically for borrowers who live outside the country.

Q4: Which U.S. states attract the most European buyers?

A: Florida, Arizona, California, Texas, and New York consistently attract European investors because of strong rental demand, international connectivity, and large property markets.

Q5: What is a DSCR loan and why do investors use it?

A: A DSCR loan qualifies borrowers based primarily on rental income from the property rather than personal income. This structure is commonly used by real estate investors who own income-producing properties.

Q6: Do foreign nationals need U.S. credit history to buy property?

A: Not always. Some lending programs evaluate borrowers using international credit reports, bank statements, and asset documentation rather than relying solely on U.S. credit scores.

Q7: Why is U.S. real estate considered a stable global investment?

A: The United States has one of the world’s largest and most transparent property markets. Strong legal protections, deep mortgage financing systems, and consistent housing demand make U.S. real estate attractive to international investors.

Q8: What types of properties do European investors typically purchase?

A: European buyers frequently invest in single-family rental homes, vacation properties, and multifamily buildings. Many investors focus on markets with strong population growth and long-term rental demand.

Q9: Will the European investment shift toward U.S. real estate continue?

A: Most analysts expect the European investment shift toward U.S. real estate to continue as investors diversify internationally. Currency exposure, rental demand, and the scale of the U.S. housing market make it a long-term destination for global property investment.

What Are Asset Based Bridge Loans? (Quick Explanation for Investors)

Asset based bridge loans are short-term real estate loans where approval is primarily based on the value of the property rather than the borrower’s income, tax returns, or credit history.

These loans are designed for situations where speed and flexibility are critical. Instead of evaluating employment records, lenders focus on the real estate collateral, loan-to-value ratio, and the borrower’s exit strategy.

Asset based bridge loans are typically used for:

Time-sensitive property acquisitions

Distressed or off-market real estate deals

Development site purchases

Short-term refinancing or liquidity events

Distressed situations

Releasing equity before a sale closes

Business related expenses

Because underwriting focuses on the asset, these loans can often close in 10–14 business days (or less), compared with 45–60 days for many traditional lenders.

For investors who cannot wait for bank underwriting cycles, asset based bridge loans allow capital to move at the same pace as the real estate opportunity.

Why Do Investors Use Asset Based Bridge Loans Instead of Bank Financing?

Investors use asset based bridge loans when traditional bank financing is too slow or documentation requirements are too restrictive.

Banks typically require:

Multiple years of tax returns

Detailed income verification

Debt-to-income analysis

Extensive credit history review

Asset based bridge loans simplify the process by focusing on three core factors:

Property value

Loan-to-value ratio

Exit strategy

For global investors, this approach is especially helpful because many foreign national borrowers do not have U.S. credit history or domestic tax returns.

The flexibility of asset based bridge loans allows investors to act quickly while arranging long-term financing later.

For example, many borrowers later refinance into long-term programs such as DSCR loans, which qualify based on property income rather than personal income.

Learn more about this type of financing in the America Mortgages guide to DSCR loans.

What Are the Best Uses for Asset Based Bridge Loans?

The best uses for asset based bridge loans involve situations where speed, flexibility, or unconventional borrower profiles make traditional loans difficult.

Below are the most common investor scenarios.

1. Acquiring Distressed or Time-Sensitive Real Estate

Asset based bridge loans allow investors to close quickly on properties that require fast transactions. Often viewed “same as cash”.

In competitive markets, distressed sellers or off-market opportunities often require closing within two weeks.

Because asset based bridge loans evaluate the property rather than the borrower’s tax returns, they allow investors to compete with cash buyers.

This is particularly valuable in major markets such as Miami, Los Angeles, Austin, and New York where real estate opportunities can disappear quickly.

2. Financing Renovations and Value-Add Investments

Asset based bridge loans are frequently used to purchase and renovate properties before refinancing into long-term financing.

Investors may acquire properties that require:

Renovation

Tenant stabilization

Property repositioning

Once improvements are completed and rental income increases, investors often refinance into longer-term financing structures.

This strategy allows investors to capture value appreciation before locking into permanent loans.

3. Development Site Acquisition

Developers often use asset based bridge loans to secure land before construction financing becomes available.

Traditional construction lenders usually require:

Final architectural plans

Permits and entitlements

Pre-sales or lease commitments

Asset based bridge loans provide interim capital so developers can acquire land while preparing full construction financing packages.

4. Accessing Liquidity Without Selling Property

Asset based bridge loans allow investors to unlock equity from real estate without selling their assets.

Investors frequently hold significant capital in property portfolios but require liquidity for:

Releasing equity before the sale of a property

Portfolio expansion

International ventures

Bridge loans allow them to access capital quickly while maintaining ownership of valuable real estate assets.

5. High Net Worth (HNW) Liquidity Solution

Asset based bridge loans allow HNW investors to unlock equity from real estate without selling their assets.

High-net-worth investors frequently hold significant capital in real estate but require liquidity for:

Business opportunity

Expansion of their business

Business acquisition

Why wait to monetize what you own? Bridge loans convert real estate equity into immediate ammunition — fast capital, full control, no dilution.

How Do Asset Based Bridge Loans Qualify Borrowers?

Asset based bridge loans qualify borrowers primarily using property value and exit strategy rather than personal income verification.

Instead of traditional underwriting, lenders evaluate the following components.

Property Value and Market Strength

The property is the most important element of underwriting.

Lenders analyze:

Market location

Comparable property sales

Liquidity in the local real estate market

Appraised value or broker valuation

This evaluation determines the maximum loan amount.

For reference, investors can review broader U.S. housing market trends through sources such as the National Association of Realtors, which publishes regular real estate market data.

Loan-to-Value Ratio

Most asset based bridge loans are structured at up to 75 percent loan-to-value (LTV).

For development or renovation projects, lenders may consider:

Current property value

After-repair value (ARV)

After-development value (ADV)

This helps determine the risk profile of the transaction.

Exit Strategy

Every asset based bridge loan must have a clear exit plan.

Typical exit strategies include:

Refinancing into permanent mortgage financing

Selling the property after stabilization

Transitioning into construction financing

Consolidating assets into portfolio loans

Without a credible exit strategy, most bridge lenders will not proceed with financing.

Real Investor Case Studies Using Asset Based Bridge Loans

Below are two examples illustrating how investors use asset based bridge loans to move quickly on U.S. real estate opportunities when traditional financing is too slow or restrictive.

Case Study 1: Off-Market Hotel Acquisition in Florida

A private investment group based in Toronto identified an off-market boutique hotel in Key West, Florida that the owner needed to sell quickly due to a partnership dispute. The seller required a closing within roughly two weeks, which immediately ruled out most traditional lenders because commercial underwriting often takes several weeks and requires extensive financial documentation.

The investors secured an asset based bridge loan covering approximately 70 percent of the property value, allowing them to close before competing buyers could arrange financing. After acquiring the property, the group upgraded several units and repositioned the hotel to target higher nightly rates. Within a year, the stabilized property qualified for long-term commercial financing, allowing the investors to refinance the bridge loan and retain a significantly more valuable hospitality asset.

Case Study 2: Portfolio Expansion Through Bridge Financing

An experienced investor based in Dubai owned several stabilized rental properties across Phoenix, Arizona and Dallas, Texas. When two multifamily opportunities became available at the same time, the investor needed a fast way to secure both properties without selling existing assets or waiting for traditional loan approvals.

The investor used asset based bridge loans by leveraging equity from properties already held in the portfolio. Because the loans were structured around real estate value rather than income documentation, the financing was approved quickly and both acquisitions closed within weeks. After the properties reached stabilized occupancy, the investor refinanced the bridge loans into long-term portfolio financing, expanding the rental portfolio while preserving ownership of the original assets.

Case Study 3: The London Takeover

A London-based UHNW entrepreneur faced a narrow window to buy out his business partner and claim full control of his company. Traditional lenders demanded months of cross-border verification. Liquidating assets meant catastrophic tax exposure.

His weapon? A Los Angeles property—underleveraged, overperforming, ignored.

America Mortgages moved in 14 days. 60% LTV. Asset-only valuation. No income scrutiny. No jurisdiction delays.

Partner out. Empire secured. California asset untouched.

Bridge financing doesn’t wait for permission—it weaponizes equity.

Who Typically Uses Asset Based Bridge Loans?

Searching for bridge loans USA, real estate bridge financing, or asset-based lending? You’re not alone, and you’re in the right place. America Mortgages specializes in fast bridge loans for real estate investors who refuse to let traditional banking slow them down.

Foreign National Investors Seeking U.S. Real Estate Loans

International buyers acquiring investment property in America face a wall: no U.S. credit history, no domestic tax documentation, endless rejection. Our foreign national mortgage loans and asset-based bridge financing eliminate these barriers. Qualify on property value and exit strategy only—buy U.S. real estate without SSN or ITIN.

U.S. Expats & Overseas Americans

Living abroad? Earning internationally? Traditional lenders can’t comprehend your profile. We specialize in expat mortgage financing and cross-border bridge loans—structuring international borrower loans that turn global complexity into closed deals.

Professional Real Estate Investors & Developers

Fix and flip loans. Rental property acquisition financing. Commercial real estate bridge loans. Speed wins. While banks crawl through income verification, our no-doc bridge loans and stated income real estate loans let you close in 10-14 days—securing off-market deals and distressed property acquisitions before competition mobilizes.

High-Net-Worth Individuals & UHNW Investors

Asset-rich, cash-flow complex? We deliver high-net-worth (HNW) mortgage solutions and liquidity without selling assets. Unlock equity from investment property through portfolio bridge loans—no capital gains tax triggers, no dilution, just immediate capital deployment.

The America Mortgages Difference: AI-Powered, Asset-Focused, Velocity-Driven

Whether you need short-term real estate financing, fast property loans, international investor mortgages, or bridge loans for rental properties—we eliminate friction. No income verification. No employment checks. No DTI restrictions.

Property value. Exit strategy. Execution.

How Asset Based Bridge Loans Fit Into a Long-Term Investment Strategy

Asset based bridge loans are rarely permanent financing. They are tactical tools used to capture opportunities quickly.

Most investors use bridge financing as the first step in a broader strategy that may include:

Refinancing into long-term mortgage loans

Selling the property after improvements

Transitioning into construction financing

Expanding into larger property portfolios

By bridging the gap between acquisition and permanent financing, asset based bridge loans allow investors to move quickly while still planning for long-term capital structures.

Why America Mortgages Is Positioned to Deliver Asset Based Bridge Loans at Scale

While competitors rely on single-source funding, America Mortgages unleashes unmatched global capital firepower through our parent company Global Mortgage Group, a Singapore based industry titan in worldwide asset-based lending.

This alliance transforms your financing advantage:

Global Liquidity, Local Execution

Access U.S. bridge loans PLUS international funding sources—a dual-channel capital engine no standalone lender can match. More liquidity means better rates, higher LTVs, and faster approvals.

Flexible Underwriting Powered by AI

Our asset-based lending algorithms bypass rigid DTI requirements and income verification. We underwrite the property and exit strategy—not your tax returns. Complex financial profile? Global income? No U.S. credit? Approved.

Velocity That Wins Deals

Traditional lenders: 45-60 days. Hard money: expensive. America Mortgages: 10-14 days—because our global funding network eliminates bottlenecks. Time-sensitive acquisition? Off-market opportunity? You close first.

Cheaper Capital, Bigger Margins

Global competition for your loan drives down pricing. Lower bridge loan rates. Reduced origination costs. Your real estate ROI improves immediately.

The Global Capital Edge: Scale, Speed, Certainty

Asset-based bridge loans demand speed, capital flexibility, and real estate underwriting expertise. Most traditional lenders depend on single credit lines or limited funding partners, crippling their ability to structure large or time-sensitive transactions.

As part of Global Mortgage Group, America Mortgages taps institutional capital across Asia, Europe, and the United States. These multi-continent capital relationships enable us to structure bridge loans rapidly and scale seamlessly from $1 million cashout refinance to transactions exceeding $100 million.

Because underwriting focuses exclusively on the real estate asset, financing is streamlined versus traditional bank lending. No personal tax returns. No employment verification. No U.S. credit history required.

America Mortgages Bridge Loan Terms

Feature

Specification

Loan Size

$1 million to $200 million+

Loan Terms

6 to 36 months

Loan-to-Value

Up to ~75%

Interest Structure

Interest-only or rolled-up payments

Closing Speed

10–14 business days

Recourse

Non-recourse available for qualified borrowers

These aggressive bridge loan terms empower investors, developers, and international buyers to strike immediately when time-sensitive U.S. real estate opportunities emerge.

The Bottom Line

Searching for best bridge loan lenders USA, fast asset-based financing, large commercial bridge loans, or international investor real estate loans? America Mortgages isn’t another lender, we’re a global capital ecosystem engineered for elite real estate operators who demand speed, scale, flexibility, and pricing power.

Frequently Asked Questions

Q1: What is an asset based bridge loan?

A: An asset based bridge loan is a short-term loan secured primarily by the value of a property rather than the borrower’s income. These loans are designed for investors who need fast financing for acquisitions, refinances, or development opportunities. The lender focuses on the property value and the borrower’s exit strategy.

Q2: How fast can asset based bridge loans close?

A: Most asset based bridge loans close within 10 to 14 business days, depending on the complexity of the transaction. Because underwriting focuses on the property rather than tax returns and employment documentation, the approval process is typically much faster than traditional bank financing.

Q3: What loan amounts are available for asset based bridge loans?

A: Asset based bridge loans typically start at $1 million and can scale well beyond $100 million, depending on the property value and transaction structure. Large transactions exceeding tens of millions of dollars are common in major real estate markets.

Q4: Do foreign nationals qualify for asset based bridge loans?

A: Yes. Many lenders offer asset based bridge loans to foreign nationals without requiring U.S. credit history. Instead, lenders review the property value, the borrower’s experience, and the planned exit strategy.

Q5: What interest rates apply to asset based bridge loans?

A: Interest rates for asset based bridge loans are typically higher than traditional mortgages because they are short-term and flexible. Rates depend on factors such as property type, loan-to-value ratio, and market conditions.

Q6: What is a typical loan-to-value ratio for asset based bridge loans?

A: Most asset based bridge loans are structured between 60 percent and 75 percent loan-to-value. Lower LTV ratios may qualify for more favorable terms depending on the borrower and property profile.

Q7: Can investors refinance asset based bridge loans?

A: Yes. Many investors refinance asset based bridge loans into long-term financing once the property is stabilized. This is common after renovations, tenant stabilization, or development progress.

Q8: Are asset based bridge loans available for development projects?

A: Yes. Asset based bridge loans are often used to acquire development sites before construction financing becomes available. Developers use bridge loans to secure land while preparing project plans and permits.

Q9: Are asset based bridge loans only for commercial real estate?

A: No. Asset based bridge loans can finance multiple property types including multifamily, commercial, development land, and high-value residential real estate. The key factor is the value and liquidity of the property used as collateral.

Why Japanese capital moving into U.S. real estate has accelerated in recent years

The economic forces pushing Japanese investors to invest overseas

Why U.S. property markets attract investors from Japan

What types of U.S. real estate Japanese buyers typically purchase

How foreign national mortgage programs may help overseas investors finance property in the U.S.

Why Is Japanese Capital Moving Into U.S. Real Estate?

Japanese capital moving into U.S. real estate is part of a broader global investment trend where investors diversify into international property markets for stability and long-term returns.

Japan is one of the world’s largest exporters of investment capital. According to international financial data summarized by organizations such as the International Monetary Fund, Japanese investors collectively hold trillions of dollars in foreign assets worldwide. This global capital base allows both institutional and private investors in Japan to allocate funds across international markets.

For many investors, U.S. property markets represent a combination of income potential, long-term appreciation, and transparent legal frameworks. These characteristics help explain why Japanese capital moving into U.S. real estate continues to attract attention from analysts and global investors alike.

Investors evaluating global property markets often compare the United States with other developed economies. Reports such as the U.S. Real Estate Market Outlook 2026 highlight how demographic growth, housing supply shortages, and economic expansion continue to shape long-term investment demand in American real estate markets.

What Economic Factors Are Driving Japanese Capital Overseas?

Several macroeconomic forces help explain why Japanese capital moving into U.S. real estate continues to increase.

1. Low Domestic Interest Rates in Japan

Japan has maintained some of the lowest interest rates in the developed world for decades. While this supports domestic borrowing, it also means investment yields within Japan can be relatively limited.

As a result, many investors seek higher returns internationally. U.S. real estate, particularly rental property, can offer stronger yield potential compared with domestic alternatives.

2. Currency Dynamics and Global Diversification

Currency movements also influence international investment flows. Periods of yen weakness often encourage Japanese investors to diversify globally.

Diversifying capital internationally can reduce exposure to domestic economic cycles and provide access to different types of assets. This is one reason analysts often discuss Japanese capital moving into U.S. real estate when examining global investment patterns.

Financial outlets such as Reuters frequently report on cross-border investment activity and note that Japanese investors are among the largest global buyers of overseas equities, bonds, and real estate assets.

3. Large Institutional Capital Pools

Japan is home to some of the world’s largest pension funds, financial institutions, and investment groups. These institutions routinely allocate portions of their portfolios to overseas assets.

Many analysts track these global capital movements because institutional investors often allocate billions of dollars into international markets each year.

Why Do Japanese Investors Consider U.S. Real Estate Attractive?

The United States remains one of the most attractive real estate markets for international investors.

Large and Liquid Property Markets

The U.S. offers one of the largest and most transparent property markets globally. Investors can access a wide range of property types including residential rentals, multifamily buildings, and commercial real estate.

Organizations such as the National Association of Realtors regularly analyze international real estate transactions and note that overseas investors continue to see the United States as a stable long-term investment destination.

Strong Rental Demand

Population growth and housing shortages in many American cities support long-term rental demand. Markets such as Texas, Florida, Arizona, and parts of the Southeast have attracted increasing attention from international investors.

High-net-worth investors often explore opportunities in premium markets as well. The growing interest in U.S. luxury property investments highlights how international buyers are diversifying across both residential and luxury real estate segments.

Transparent Ownership Structures

Property ownership laws in the United States are generally clear and well documented. This transparency can make it easier for overseas investors to evaluate potential opportunities.

Because of these factors, Japanese capital moving into U.S. real estate is often viewed as part of a long-term diversification strategy rather than a short-term trend.

What Types of U.S. Property Do Japanese Investors Typically Buy?

Japanese investors often focus on properties that generate steady income and long-term appreciation.

Common investment targets include:

Single-family rental properties in growing metropolitan areas

Multifamily apartment buildings

Residential investment portfolios

Institutional property funds and commercial assets

Many overseas investors evaluate markets where strong economic expansion and population growth support rental demand. Research reports published by the Urban Land Institute and similar organizations frequently highlight U.S. metropolitan areas as attractive destinations for long-term property investment.

Can Japanese Investors Finance U.S. Real Estate Purchases?

Yes. Many international investors explore financing rather than purchasing property entirely with cash.

Programs designed for overseas buyers may include:

Foreign National Mortgage Loans

DSCR loans for rental property investors

Portfolio financing for investors purchasing multiple properties

These lending structures allow investors to maintain liquidity while building property portfolios.

International investors who wish to move forward with financing options can begin the process by reviewing the secure application portal available through Secure Your U.S. Mortgage.

Why Do Many Overseas Investors Get Preapproved Before Buying U.S. Property?

Preparation plays an important role in international property transactions.

Many overseas investors choose to get preapproved for financing before identifying properties. Preapproval can help investors understand:

potential loan amounts

financing structures

documentation requirements

In competitive markets, having financing clarity can help buyers move more efficiently once suitable properties appear.

Investors exploring financing options can also speak directly with a mortgage specialist through our contact page or by contacting the international lending team at [email protected].

Understanding financing options early can be especially helpful for investors evaluating opportunities across multiple cities or property types.

Is Japanese Capital Moving Into the U.S. Real Estate Likely to Continue?

Global investment flows tend to follow long-term structural trends rather than short-term market movements.

Several factors suggest that Japanese capital moving into U.S. real estate may remain relevant:

Japan continues to hold one of the largest global pools of investment capital

International diversification remains a common strategy for large institutional investors

U.S. property markets continue to offer liquidity and income potential

While investment strategies vary widely between individual investors, analysts often view cross-border property investment as part of a broader global portfolio allocation strategy.

Frequently Asked Questions

Q1. Why are Japanese investors buying U.S. real estate?

A: Japanese investors often look abroad because domestic investment yields in Japan can be relatively low. U.S. real estate markets offer a combination of rental income, market transparency, and long-term appreciation potential. This combination makes international property investment attractive for portfolio diversification.

Q2. How much overseas capital does Japan invest globally?

A: Japan is one of the world’s largest sources of outbound investment capital. Japanese institutions and investors collectively hold trillions of dollars in overseas assets across equities, bonds, infrastructure, and real estate. This large capital base allows investors to allocate funds across global markets.

Q3. Why is the U.S. a popular destination for Japanese property investors?

A: The United States offers one of the largest and most transparent property markets in the world. Strong rental demand, clear property rights, and large metropolitan markets attract international investors seeking income-producing assets and long-term portfolio diversification.

Q4. Can Japanese citizens legally buy property in the United States?

A: Yes. Foreign nationals, including Japanese investors, are generally allowed to purchase property in the United States. Ownership rights are typically similar to those of domestic buyers, although financing options and tax considerations may differ.

Q5. Do Japanese investors usually pay cash for U.S. property?

A: Some international buyers purchase property with cash, but many investors explore financing options. Mortgage programs designed for foreign nationals may allow investors to leverage capital while building larger property portfolios.

Q6. What cities attract Japanese real estate investors?

A: Major metropolitan areas such as New York, Los Angeles, Miami, and Dallas have historically attracted international investors. However, growth markets in states like Texas, Florida, and Arizona are increasingly drawing attention due to population growth and rental demand.

Q7. What mortgage options exist for Japanese investors?

A: Foreign national mortgage programs may allow overseas investors to finance U.S. property purchases. Some lenders also offer DSCR loans designed for rental property investors, where loan qualification focuses on property income rather than personal employment income.

Q8. Why do international investors diversify into U.S. property?

A: Real estate diversification helps investors reduce exposure to domestic economic conditions. By allocating capital across different countries and property markets, investors can balance risk while accessing different sources of income and appreciation.

Q9. Should overseas investors get preapproved before searching for property?

A: Getting preapproved for financing can help international buyers understand their purchasing power and loan structures before beginning a property search. Preapproval may also help buyers move more quickly in competitive markets where desirable properties can receive multiple offers.

What You Will Learn

What’s really driving the Florida market price drop in 2026

Why prices usually rise faster than they fall, and what that means for investors

Why international buyers should get preapproved before demand returns

Which Florida markets global investors are watching right now

Is the Florida Market Price Drop a Warning Sign or a Buying Window?

The current Florida market price drop is largely driven by increased inventory, higher ownership costs, and condo-sector adjustments, not a nationwide housing downturn.

The recent Florida market price drop has made headlines, but smart investors look deeper than short-term data surrounding the Florida market. According to the latest housing forecast, median prices across Florida’s largest metro areas are expected to decline by around 1.9% in 2026, even as national prices remain slightly positive.

That doesn’t signal a market crash. Instead, it suggests a market reset driven by supply, shifting migration trends, and rising ownership costs.

Historically, U.S. real estate prices tend to climb faster than they fall. That’s why many experienced international investors view a Florida market price drop as a preparation phase, not a retreat.

What’s Actually Causing the Florida Market Price Drop Right Now?

Several structural factors are shaping the current Florida housing cycle:

Growing Supply and Slower Demand

Economists note that increasing inventory alongside slightly softer demand has created price pressure across the state.

More new construction and shifting remote-work trends have reduced the urgency buyers felt during the post-pandemic surge.

Rising Insurance and HOA Costs

Higher insurance premiums and increasing HOA fees, particularly in the condo segment, are weighing on affordability and buyer sentiment.

These costs influence short-term pricing but don’t change Florida’s long-term fundamentals as a global investment destination.

Regional Differences Matter

Not all Florida markets are moving the same way. Forecasts show projected declines of:

Meanwhile, Miami is expected to remain relatively resilient with modest growth.

For overseas buyers, this highlights the importance of market selection, something explored in our guide to investing in U.S. real estate as a foreign national.

Are Condos Driving the Florida Market Price Drop More Than Houses?

Yes, and this is one of the most misunderstood parts of the current cycle.

Data shows:

Condo listing prices fell about 10.8%

Single-family homes declined only 3.6%

This means the broader Florida market price drop is heavily influenced by the condo sector rather than detached housing.

Even with recent declines, values remain significantly higher than pre-2020 levels:

Condo prices up roughly 26% since 2020

Single-family homes up around 34% since 2020

That’s why many investors see the current phase as a rebalancing rather than a downturn.

Why Do Prices Increase Faster Than They Decrease in Real Estate Cycles?

Real estate cycles rarely move symmetrically.

When demand returns:

Inventory tightens quickly

Competition increases

Prices accelerate faster than they previously declined

Some economists suggest that easing mortgage rates could bring more buyers back into the market, which could stabilize prices again.

This pattern is why experienced investors often act during periods like the current Florida market price drop, before headlines shift back toward growth.

Why International Buyers Should Get Preapproved Before the Market Turns

Preparation matters more than timing headlines.

Many overseas buyers wait until markets “feel safe,” but by then:

Inventory shrinks

Competition rises

Negotiation power decreases

Getting preapproved early allows buyers to move quickly when opportunities appear , especially in off-market or fast-moving listings.

Programs like U.S. Expat Mortgage Loans and Foreign National Mortgage Programs are structured around international underwriting guidelines, helping borrowers qualify using foreign income, liquidity, and alternative credit documentation.

Understanding underwriting guidelines before searching helps global investors respond faster when the right property becomes available.

Which Florida Markets Are Global Investors Watching During the Florida Market Price Drop?

While some Gulf Coast areas face stronger corrections, major international hubs remain attractive:

Miami continues to show resilience due to global demand and diversified economic drivers.

Tampa’s moderate adjustment may create entry opportunities for long-term investors.

Emerging secondary markets may offer improved yield potential as supply expands.

Getting preapproved is often the first step international buyers take before searching on the MLS, where most U.S. properties are listed.

After that, instead of reacting to headlines, focus on preparation:

Review financing options and underwriting guidelines

Get preapproved as part of your buying strategy

Monitor inventory trends rather than daily price headlines

Work with lenders experienced in cross-border transactions

Preparation during a Florida market price drop often provides stronger negotiating leverage and better long-term positioning.

Speak to a Specialist — Get Preapproved Before Competition Returns

America Mortgages, Leading Experts in Foreign National and U.S. Expat Mortgage Loans, helps overseas buyers structure financing using foreign income, flexible credit profiles, and international lending solutions.

If you’re considering buying during the current Florida market price drop, speaking with a specialist early can help you understand eligibility, timelines, and next steps. You can reach our team directly through the America Mortgages Contact Page, email us at [email protected], or call +1 (845) 583-0830 to get preapproved and prepared before the market shifts again.

Frequently Asked Questions

Q1. Is the Florida market price drop a sign of a housing crash?

A: No, forecasts suggest a modest average decline rather than a collapse. The adjustment is largely tied to supply increases and higher ownership costs, not a fundamental demand breakdown.

Q2. Why are Florida condo prices falling faster than houses?

A: Higher HOA fees, insurance costs, and new regulations have impacted condos more heavily. Single-family homes have experienced much smaller price adjustments compared to the condo sector.

Q3. Should international buyers wait until prices fall further?

A: Timing markets perfectly is difficult. Many investors choose to get preapproved early so they can act when favorable opportunities appear rather than chasing the bottom.

Q4. Will mortgage rates affect the Florida market price drop?

A: Yes. Economists expect that easing mortgage rates could bring more buyers back into the market, which may stabilize or reverse price declines over time.

Q5. Are foreign nationals allowed to buy property in Florida during this market phase?

A: Yes. Foreign nationals can purchase U.S. property, and specialist lenders offer mortgage programs designed for overseas income and non-traditional credit profiles.

Q6. Why do smart investors focus on preparation instead of headlines?

A: Real estate cycles often shift quickly. Investors who prepare financing in advance are positioned to move when supply tightens or competition returns.

Q7. Which Florida cities are expected to remain strong despite price adjustments?

A: Markets like Miami show more resilience due to global demand, while some Gulf Coast markets are projected to see larger price corrections.

Q8. Does a Florida market price drop mean better negotiation opportunities?

A: In many cases, yes. Increased inventory can give buyers more leverage, particularly when sellers adjust expectations after rapid price growth.

Q9. How can overseas buyers get preapproved for U.S. property?

A: International buyers typically provide proof of income, liquidity, and documentation aligned with U.S. mortgage underwriting guidelines. Working with lenders specializing in foreign national and U.S. expat loans can streamline the process.

If you are researching rental property financing, understanding how DSCR loans work is essential. Investors increasingly rely on DSCR loans to scale portfolios, refinance equity, and bypass traditional income documentation hurdles.

This guide explains how DSCR loans work, how qualification happens, how underwriting evaluates risk, and when these loans make strategic sense.

What You Will Learn

What DSCR loans are and how the Debt Service Coverage Ratio is calculated for residential investment properties

How DSCR loan qualification works for U.S. expats and Foreign Nationals

What lenders review during DSCR underwriting, including rent verification and PITIA analysis

The best uses of DSCR loans for scaling rental portfolios and cash-out refinancing

Real case study examples showing how DSCR loans are structured in practice

How America Mortgages structures flexible DSCR programs, including below 1:1 and no-ratio scenarios

What Are DSCR Loans and How Do They Work?

DSCR loans are investment property mortgages where approval is based primarily on whether the rental income covers the property’s debt obligations, rather than the borrower’s personal income.

DSCR stands for Debt Service Coverage Ratio. It measures a property’s ability to generate enough income to service its mortgage. For most residential 1–4 unit investment properties, lenders calculate DSCR using the property’s market rent divided by PITIA, which includes Principal, Interest, Taxes, Insurance, and HOA dues if applicable.

For residential DSCR loans: DSCR = Market Rent ÷ PITIA

For example, if a property generates $4,800 per month in market rent and the total PITIA payment is $3,463, the DSCR equals 1.39. This means the property produces 39% more income than required to cover the mortgage payment, creating a lender cushion.

Most residential DSCR lenders require a minimum ratio between 1.1 and 1.25. A DSCR of 1.0 means the property breaks even. The higher the ratio, the stronger the perceived cash-flow stability and the better the potential loan terms.

What makes America Mortgages, a direct lender on DSCR loans unique is their flexibility in programs that other lenders will not consider including DSCR ratios below 1:1 and even NO RATIO. This means if you find the perfect property but it needs improvements to optimize the rental income, America Mortgages has you covered!

It’s important to note that in commercial and multifamily (5+ unit) lending, DSCR is typically calculated using Net Operating Income divided by total debt service, which accounts for operating expenses. Investopedia provides a broader explanation of this commercial DSCR framework for additional financial context.

Why Are DSCR Loans Popular With Real Estate Investors?

DSCR loans have grown in popularity because conventional loans restrict investors through personal income verification and debt-to-income ratios. Traditional mortgage programs require tax returns, W2s, and often limit borrowers to ten financed properties.

DSCR loans shift the focus entirely to property performance. It’s common sense underwriting. If the rental income supports the payment, approval is possible regardless of how personal income is structured. This makes DSCR loans especially attractive for portfolio investors, self-employed borrowers, and individuals who aggressively deduct expenses on tax filings.

Investors comparing funding structures often review rental property financing strategies to determine when DSCR loans outperform conventional options.

What Are the Best Uses of DSCR Loans?

One of the strongest uses of DSCR loans is scaling beyond conventional property limits. Because approval is not constrained by personal debt-to-income ratios, investors can continue acquiring rental assets as long as each property meets income thresholds.

DSCR loans are also widely used for cash-out refinancing. Investors refinance a performing rental, extract equity, and redeploy that capital into another acquisition. Since qualification depends on rent coverage rather than income growth, expansion becomes more systematic and predictable.