A DSCR loan qualifies an investment property mainly through its rental cash flow instead of your traditional personal income. This approach can help real estate investors finance income-producing properties. However, other options use different qualification methods. Conventional, bank statement, hard money, HELOC, and personal loans each serve different financial needs and investment strategies.

Understanding these differences can help you choose financing that matches your goals and financial position. Some loans focus on your income and credit, while others consider bank deposits, property value, or existing home equity. Therefore, comparing a DSCR loan with other financing options gives you a clearer view of which structure may suit your investment plan.

How Does a DSCR Loan Compare With Other Mortgage and Financing Options?

A DSCR loan qualifies you mainly through a property’s rental income rather than personal employment records or tax returns. This can suit self-employed investors and buyers expanding rental portfolios. However, the right financing option depends on your property type, available income documentation, investment strategy, and repayment plans. Therefore, a careful DSCR loan comparison is essential.

Key factors to compare include qualification method, property type, income documentation, and repayment plans. Before applying, reviewing the DSCR loan required documents can help you prepare the information lenders typically request.

- Qualification method: Property cash flow, personal income, bank deposits, credit, or home equity.

- Property type: Primary residence, rental property, or short-term investment project.

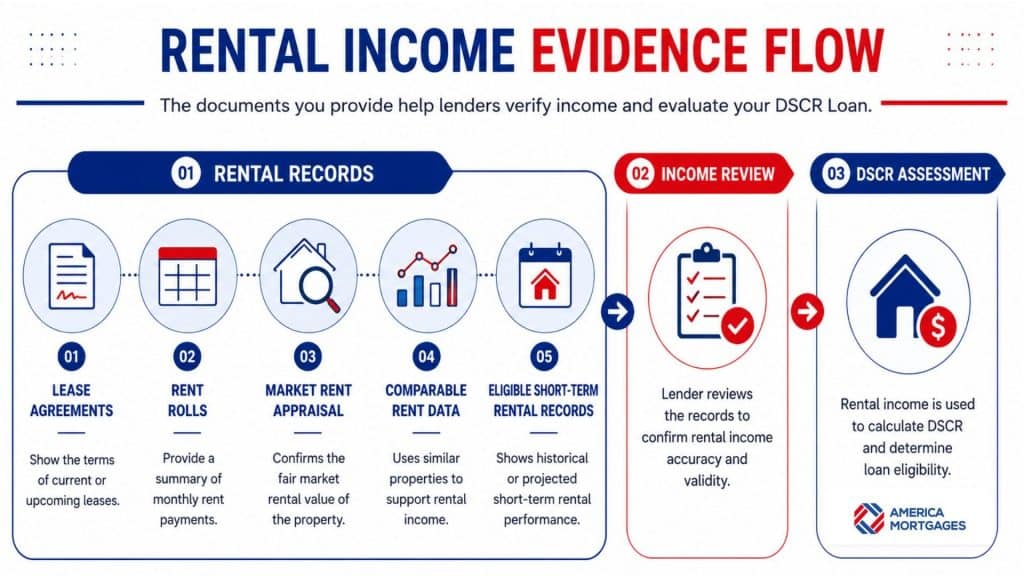

- Income documents: Tax returns, employment records, bank statements, or rental income records.

- Investment strategy: Long-term rentals, portfolio growth, renovations, or fix-and-flip projects.

- Upfront costs: Down payment requirements, closing costs, fees, and available cash reserves.

- Repayment plans: Loan term, interest structure, monthly payments, and expected holding period.

The debt service coverage ratio shows whether a property’s income can cover its debt obligations. Meanwhile, other financing options may focus more on your personal income, credit, deposits, or equity. DSCR loans may require larger down payments and higher rates than traditional mortgages. Therefore, you should compare the total costs, qualification rules, and long-term goals.

What Is the Difference Between a DSCR Loan vs Conventional Loan?

The main difference between a DSCR loan vs conventional loan is how lenders qualify you. A DSCR loan focuses mainly on the investment property’s rental income and cash flow. In contrast, conventional lenders review your personal income, tax returns, employment history, credit profile, and debt-to-income ratio before approving the loan.

When comparing a DSCR vs conventional loan, you should also consider property purpose, documentation, down payment, rates, and scalability. Conventional loans may offer lower rates but require stricter personal financial reviews. Meanwhile, DSCR loans can support rental portfolio growth without relying mainly on W-2 income. You can learn more in our DSCR loan guide.

How Does a Bank Statement Loan vs DSCR Loan Compare for Investors?

The main difference between a bank statement loan vs DSCR loan is the income source lenders review. Bank statement loans use deposits in your personal or business accounts to estimate income, making them suitable for self-employed borrowers, including some U.S. expats with non-traditional income records. In contrast, DSCR loans qualify borrowers primarily based on the rental income generated by the investment property, which can appeal to foreign nationals and U.S. expats investing in U.S. real estate.

A bank statement loan still relies on your personal or business income to support approval. Lenders typically review several months of bank deposits to assess your earning pattern. Meanwhile, a DSCR loan compares the property’s rental income with its debt obligations, allowing eligible investors to qualify without traditional income documents such as W-2 forms or tax returns.

Your choice depends on how you earn income and the type of property you want to finance. Bank statement loans may suit borrowers with strong cash flow but complex tax returns, while DSCR loans are often a better fit for investors focused on rental property income. Before comparing loan offers, it is also important to review each lender’s Loan Estimate, which outlines the interest rate, projected monthly payments, closing costs, and other key loan terms. The Consumer Financial Protection Bureau (CFPB) explains how borrowers can review and compare Loan Estimates to make informed mortgage decisions. You can also explore our mortgage options for foreign nationals when investing from overseas.

When Should You Choose a DSCR Loan vs Hard Money Loan, HELOC, or Personal Loan?

Choose a DSCR loan when you plan to buy or refinance a long-term rental property without using traditional personal income documents. However, other financing options suit different needs. A hard money loan can fund short property projects, while a HELOC uses existing home equity. Personal loans provide unsecured funds for smaller expenses.

The main differences include:

- DSCR loan vs hard money loan: Choose DSCR financing for long-term rentals and hard money for short-term fix-and-flip projects.

- DSCR loan vs HELOC: A DSCR loan uses rental cash flow, while a HELOC provides funds against existing home equity.

- DSCR loan vs personal loan: DSCR financing supports rental property investment, while personal loans offer unsecured funds for smaller needs.

Your investment timeline, available equity, and property plans should guide your financing choice. DSCR loans often suit investors building rental portfolios for long-term income. In contrast, other options can provide faster or more flexible funding for specific needs. Before choosing financing, you can learn how to read a DSCR loan term sheet and compare important loan terms or compare the pros and cons of a DSCR loan to better understand your situation.

How Do Debt Yield, FCCR, Cash DSCR, and Interest Coverage Ratio Differ From DSCR?

DSCR measures a property’s cash flow against its required debt payments. The DSCR ratio calculation uses property income and debt obligations to determine repayment capacity. However, other financial metrics provide different views of risk and financial strength.

| Metric | What It Measures | Main Use | Key Difference From DSCR |

| DSCR | Cash flow compared with total debt payments | Loan repayment analysis | Includes principal and interest payments |

| Debt Yield | Net operating income compared with loan amount | Property lending risk | Does not depend on interest rate or loan term |

| FCCR | Earnings available for fixed financial obligations | Wider financial analysis | Includes rent, leases, and other fixed charges |

| Cash DSCR | Available cash compared with debt payments | Cash liquidity analysis | Focuses more closely on actual available cash |

| Interest Coverage Ratio | Earnings compared with interest expense | Interest payment analysis | Measures interest coverage rather than total debt service |

When comparing debt yield vs DSCR, FCCR vs DSCR, or DSCR vs interest coverage ratio, you should consider the purpose of each metric. The fixed charge coverage ratio vs DSCR comparison covers wider obligations. Similarly, cash DSCR vs DSCR focuses more closely on available cash. Together, these measures can support clearer lending and investment analysis.

Which DSCR Loan Option Is Right for Your U.S. Property Investment?

Financing a U.S. investment property from overseas can feel complicated. You may face challenges with income documents, residency requirements, rental income calculations, and unfamiliar loan terms. Moreover, the right option can vary by property type and investment strategy. Without clear guidance, you may struggle to compare loan structures and choose suitable financing.

At America Mortgages, we help foreign nationals and U.S. expats explore financing options for U.S. property investments. Our team considers your rental income, property type, investment plans, and borrower circumstances. You can speak with our mortgage team to discuss your options and find a financing approach that supports your investment goals.

FAQS

Q1: Can You Use a DSCR Loan for a Primary Residence?

No, a DSCR loan is generally designed for investment properties rather than primary residences. The lender evaluates the property’s expected rental income and debt payments. Therefore, you usually need another mortgage option for a home you plan to occupy. DSCR financing is better suited to eligible income-producing rental properties.

Q2: What DSCR Ratio Do Lenders Usually Require?

Many lenders look for a DSCR of around 1.0 or higher, although requirements vary between loan programs. A ratio above 1.0 means the property generates enough income to cover its debt payments. However, lenders may also review credit, reserves, property type, and other factors before making a lending decision.

Q3: Can Foreign Nationals Qualify for a DSCR Loan in the United States?

Yes, eligible foreign nationals can access DSCR loan programs for U.S. investment properties. Since qualification can focus on property cash flow, traditional U.S. income documents may not always be required. However, requirements vary by lender and borrower profile. Therefore, investors should review down payment, reserve, credit, and property requirements carefully.

Q4: Can You Use a DSCR Loan for a Short-Term Rental Property?

Yes, some DSCR loan programs allow eligible short-term rental properties. However, lenders may calculate qualifying rental income differently based on the property and program. They may review market rent, lease income, or other approved records. Therefore, you should confirm the income calculation method before relying on projected short-term rental earnings.

Q5: Can You Refinance an Existing Rental Property With a DSCR Loan?

Yes, you can use a DSCR loan to refinance an eligible rental property if you meet the lender’s requirements. Investors may refinance to change loan terms or access available property equity. However, qualification standards, equity limits, costs, and cash reserve requirements vary. Therefore, compare the new financing terms before refinancing.

Q6: Does a DSCR Loan Affect Your Personal Debt-to-Income Ratio?

A DSCR loan generally qualifies you through the investment property’s cash flow instead of a traditional personal debt-to-income calculation. This structure can support investors who want to expand their portfolios. However, lenders may still review credit and other borrower details. Therefore, qualification should not be confused with having no financial requirements.