Your DSCR ratio compares a rental property’s qualifying income with the housing payment used in the lender’s calculation. This figure helps investors understand whether the property’s income can support the proposed financing.

The calculation is especially relevant for foreign nationals and U.S. expats investing in U.S. rental properties. Their income, assets, employment, and tax records may be based outside the United States. Therefore, property-focused financing can offer a practical alternative to conventional income-based qualification.

However, calculating the ratio requires more than dividing expected rent by an estimated loan payment. You need accurate income and payment figures. You must also understand how the lender evaluates your specific property type.

What Is a DSCR Ratio and What Does It Measure?

A DSCR ratio measures how qualifying rental income compares with the property payment used for loan qualification. DSCR stands for debt service coverage ratio.

The result shows the relationship between two figures. A ratio above 1.0 means qualifying rent exceeds the calculated payment. A ratio of 1.0 means both figures are equal. Below 1.0, the qualifying rent falls short of that payment.

For example, a 1.25 ratio means qualifying rent equals 1.25 times the calculated payment. However, that figure does not represent a 25% investment return. DSCR measures income coverage rather than overall profitability.

Actual investment performance depends on additional factors. These may include maintenance, repairs, vacancies, management costs, and local market conditions. Therefore, investors should use DSCR as one part of their wider property analysis.

This property-focused approach can be useful for investors with financial records outside the United States. A foreign national may earn and bank abroad. Similarly, a U.S. expat may work for an overseas employer or own a foreign business.

Investors who need a broader overview can review the complete guide to DSCR loans for real estate investors.

What Is the DSCR Ratio Formula?

The DSCR ratio formula divides qualifying rental income by the applicable housing payment. Many residential DSCR programs calculate these figures monthly.

The basic calculation is:

DSCR Ratio = Qualifying Monthly Rental Income ÷ Applicable Monthly Housing Payment

The first figure is the rental income accepted for loan qualification. Depending on the property and program, lenders may review different sources to establish this amount. These can include existing lease information or an appraiser’s market-rent assessment.

The second figure is the housing payment used in the calculation. It commonly includes principal and interest payments, property taxes, insurance, and applicable association dues. These combined costs are often described as PITIA.

Consider this example:

| Monthly Figure | Amount |

| Qualifying rental income | $2,800 |

| Principal and interest | $1,650 |

| Property taxes | $300 |

| Insurance | $150 |

| HOA dues | $100 |

| Total housing payment | $2,200 |

| DSCR Ratio | 1.27 |

The DSCR ratio calculation is $2,800 divided by $2,200. Therefore, the result is 1.27.

In this example, qualifying rental income equals 1.27 times the calculated housing payment. This calculation gives the investor a clear view of the property’s income coverage.

DSCR is also a broader measure used in income-property lending to assess whether property income can cover debt obligations. The Office of the Comptroller of the Currency discusses debt service coverage as an important measure in income-property lending. However, the exact income and payment figures used in the calculation can differ by lending context and loan program.

Loan documents may also show annual debt service when presenting payment obligations over a yearly period. The meaning of total debt service can vary across lending contexts and programs. Therefore, investors should follow the definitions used in their specific loan documents.

Calculation methods can also vary between loan programs. For this reason, an investor’s initial calculation should use realistic figures and the correct program method.

How Do You Calculate the DSCR Ratio Correctly?

You calculate the DSCR ratio by confirming qualifying rent, determining the applicable payment, and dividing those figures. Following the correct order reduces errors and creates a more useful estimate.

Use these five steps:

- Identify the qualifying rental income.

Start with the income that may qualify under the loan program. An existing lease can provide useful rental information. For vacant properties, an appraiser may estimate market rent using comparable local rentals. - Calculate the applicable housing payment.

Add the payment components required by the program. These may include principal, interest, property taxes, insurance, and applicable HOA dues. - Apply the formula.

Divide the qualifying monthly rent by the applicable monthly housing payment. For example, $3,000 divided by $2,400 produces a ratio of 1.25. - Check the income method for your property type.

Lenders may assess income differently across rental strategies. A leased property and a vacant property do not provide the same income evidence. Eligible short-term rentals may also require a program-specific income review. - Compare the result with the program requirement.

Check whether the calculated result meets the lender’s applicable Minimum DSCR. The required threshold depends on the lender and specific loan program.

Once you understand the calculation, review how it appears within the proposed financing terms. The interest rate, loan amount, and payment structure can affect the final figures. Learning how to read a DSCR loan term sheet can help you assess those details together.

What Is a Good DSCR Ratio for a Rental Property?

A good DSCR Ratio meets the chosen program’s requirement and supports the investor’s wider financing strategy. There is no single ratio that qualifies every property for every DSCR loan program. Lenders set their own program guidelines. Some programs require a ratio above 1.0. Others may consider different ratios under specific conditions. Therefore, investors should confirm the applicable threshold before relying on an early calculation.

The ratio also works within a wider loan structure. A lender may review available equity, cash reserves, credit profile, property type, and loan purpose. These factors can affect the financing options available for a particular transaction.For this reason, the lowest qualifying ratio should not become the only selection criterion. Investors should also review the interest rate, required equity, reserves, fees, and prepayment terms. Together, these details show how the financing may affect the investment.

International investors have additional practical considerations. Foreign nationals may need to document overseas assets or transfer funds across borders. U.S. expats may hold income, savings, or business interests in another country. The financing structure should fit those circumstances and the property itself. Foreign investors can explore financing options for foreign nationals based on their cross-border circumstances. U.S. citizens abroad can review mortgage options for U.S. citizens living overseas.

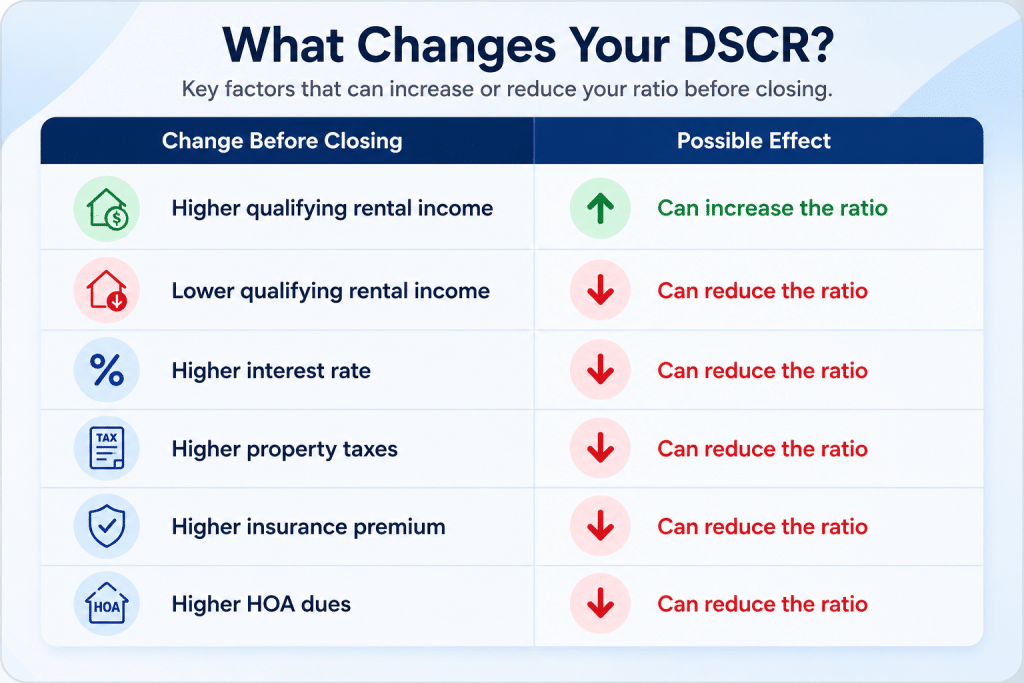

What Can Change Your DSCR Ratio Before Closing?

Your DSCR Ratio can change before closing when the lender updates qualifying income or housing payment figures. Several parts of the transaction may remain subject to review during appraisal and underwriting.

For example, an investor may estimate rent using local listings before applying. Later, the appraisal process may support a different qualifying rental amount. That updated figure can change the income side of the calculation.

The payment side can also change during the loan process. A higher interest rate increases the principal and interest portion of the mortgage payment. Updated taxes, insurance premiums, or HOA dues can increase the total housing obligation.

Therefore, investors should update their calculation when important figures change. They should also ask which loan terms are final and which remain subject to review. This approach helps prevent surprises before closing. It also gives investors a clearer basis for reviewing the final financing structure.

How Can Investors Use DSCR When Comparing Rental Properties?

Investors can use DSCR ratio calculations to compare income coverage across potential rental properties. Applying a consistent method helps identify which properties provide more qualifying income relative to their calculated payments.

Consider three potential investments:

| Property | Qualifying Rent | Housing Payment | DSCR Ratio |

| Property A | $2,800 | $2,200 | 1.27 |

| Property B | $3,100 | $2,500 | 1.24 |

| Property C | $2,400 | $2,450 | 0.98 |

Property A has the highest ratio in this comparison. Property B earns more monthly rent, but it also carries a larger housing payment. Property C has qualifying rent below its calculated payment.

This comparison shows why rent alone cannot measure financing strength. A higher-rent property can still have a lower ratio when its payment is also higher.

Investors can use this comparison during early property screening. However, they should also assess location, operating costs, rental strategy, and long-term ownership plans. Those factors address investment questions that the DSCR calculation does not measure.

For overseas investors, the comparison can support a more structured U.S. property search. It helps narrow potential investments before beginning a detailed financing review.

Understand Your DSCR Before Financing a U.S. Investment Property

Understanding your DSCR Ratio helps you review a rental property with greater financial clarity. Start with accurate rental income and housing payment figures. Then, consider how the financing fits your available capital and long-term investment plans. Foreign nationals and U.S. expats often manage assets, income, and banking relationships across different countries. As a result, their financing needs can require experience with cross-border borrower profiles and U.S. property investment.

America Mortgages works with international investors seeking financing for U.S. real estate. You can contact our mortgage team to discuss your property and available financing options. If you are considering a U.S. investment property, email [email protected] or call +1 (845) 583-0830. An experienced mortgage specialist can discuss your property and investment plans with you.

FAQs

Can I Improve My DSCR Ratio Before Applying for a Loan?

Yes. A higher qualifying rent or lower housing payment can improve the ratio. Depending on the transaction, investors may review pricing, loan amount, insurance costs, or other financing factors with their lender.

Does a High DSCR Ratio Mean a Rental Property Is Profitable?

No. DSCR measures whether qualifying rental income covers the payment used in the lender’s calculation. It does not fully account for maintenance, vacancies, repairs, management costs, income taxes, or investment returns.

Can Two Lenders Calculate Different DSCR Ratios for the Same Property?

Yes. Lenders may use different program rules for qualifying rent, short-term rental income, or payment components. Therefore, the same property can produce different results when approved calculation methods differ.

Should I Calculate DSCR Before Making an Offer on a Rental Property?

Yes. An early calculation can show whether projected rent supports the expected housing payment. However, use realistic figures because the final appraisal, interest rate, taxes, and insurance may change the result.

Can Currency Exchange Rates Affect a DSCR Loan Application for International Investors?

Exchange rates do not directly change a property’s U.S. rental-income DSCR calculation. However, currency movements may affect available funds, reserve documentation, and the cost of transferring money for closing.