Large housing developments often require funding before long-term financing is available. Bridge loans help foreign national investors secure U.S. real estate quickly, cover short-term funding gaps, and keep projects moving without unnecessary delays. This makes them a practical option for time-sensitive development opportunities.

For many international buyers, securing funds for a large development can be more challenging than finding the right property. Understanding U.S. bridge loans helps explain how short-term funding works, while bridge loans simplified provides a clear overview of when this type of loan may be the right choice for a development project.

Every development project is different, and choosing the right funding strategy is an important first step. Whether you are buying land or investing in a large residential community, America Mortgages is here to help you move forward with confidence.

How Can Bridge Loans Help Foreign National Investors Finance Large Housing Developments?

Bridge loans help foreign national investors secure large housing developments without waiting for long-term financing. They provide fast access to funds for buying land, acquiring residential projects, or covering early development costs. As a result, investors can move quickly when valuable opportunities become available and keep their projects on schedule.

Key benefits for large housing developments:

- Purchase land or residential developments before another buyer.

- Access funds faster than many traditional loan options.

- Cover early project costs, including deposits and pre-construction expenses.

- Keep construction plans moving while arranging permanent financing.

- A bridging loan for property development can provide short-term funding while you arrange a long-term loan.

In many cases, acting quickly can help investors secure better opportunities. Sellers and developers often prefer buyers who can complete transactions without long delays. Therefore, short-term funding can make the purchase process more flexible while giving investors extra time to arrange permanent financing.

For foreign national investors, timing can make a big difference. The right funding solution gives you more time to complete your purchase, prepare your development, and move to long-term financing without putting your investment plans on hold.

What Should You Prepare Before Applying for a Bridge Loan?

Before applying for a bridge loan, gather the financial and property documents your lender needs. This helps speed up the review process. It also reduces delays and gives the lender a clear understanding of your project, financial position, and repayment plan.

| Document | Why It Is Important |

| Passport or government-issued ID | Confirms your identity. |

| Property purchase agreement | Provides details about the property you plan to buy. |

| Development or business plan | Explains your project’s goals, timeline, and estimated costs. |

| Proof of available funds | Shows your down payment or available cash reserves. |

| Asset and bank statements | Helps lenders review your financial position. |

| Exit strategy | Explains how you plan to repay the loan, such as refinancing or selling the property. |

First, check that all your documents are complete and up to date. This makes the review process faster. It also helps prevent unnecessary delays. As a result, your application can move forward more smoothly.

Next, review the lender’s requirements before you apply. This helps you prepare the right information from the start. If you want to understand how lenders evaluate property-backed financing, asset-based bridge loans explained provide helpful information before you begin the application process.

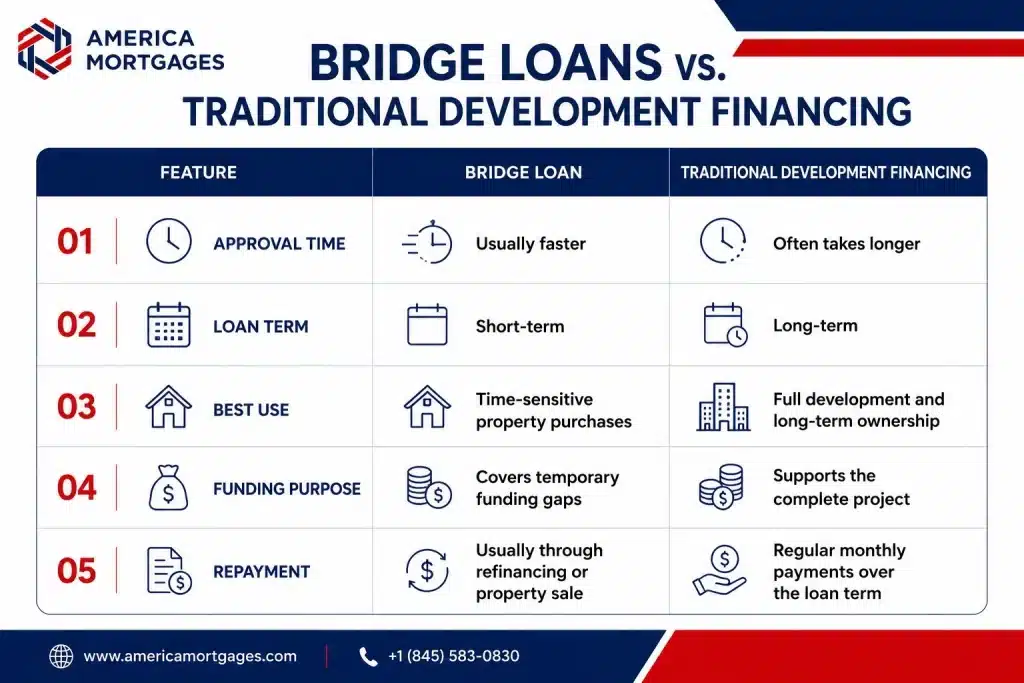

How Do Bridge Loans Compare with Traditional Development Financing?

Bridge loans provide fast, short-term funding when time is important. In contrast, traditional development financing is designed for long-term projects and usually takes longer to approve. Therefore, many investors use a bridge loan first and then switch to long-term financing once the project is ready.

The right option depends on your investment goals and project timeline. If you need to secure a property quickly, short-term funding may be the better choice. If you still have questions about loan terms or eligibility, the bridge loan FAQ for HNW homeowners answers many common questions before you move forward.

Many developers use both options at different stages of the same project. They often secure the property with a bridge loan first. Later, they move to long-term financing once the project is ready. In many cases, a commercial bridging loan for property development provides the flexibility needed before permanent financing is in place.

What Risks Should Developers Consider Before Using Bridge Financing?

Bridge financing can help you move quickly, but it also comes with important risks. Before you apply, understand the loan terms, repayment plan, and project timeline. Careful planning helps reduce unexpected costs and keeps your development on track from start to finish.

Have a Clear Exit Strategy

Plan how you will repay the loan before signing the agreement. Many developers refinance into a long-term loan or sell the property after completion. A clear exit strategy helps reduce financial pressure and lowers the risk of repayment delays.

Prepare for Higher Borrowing Costs

Bridge financing often has higher interest rates and fees than long-term loans. Therefore, include these costs in your project budget. This helps you avoid cash flow problems and keeps your development financially stable.

Allow Time for Unexpected Delays

Construction delays, permit approvals, or market changes can affect your project schedule. As a result, your repayment plan may also change. Setting a realistic timeline gives you more flexibility if unexpected challenges arise.

Review Market Conditions

Property values and financing conditions can change during your project. Therefore, monitor the market regularly and adjust your plans when needed. This helps you make informed decisions and reduces the impact of unexpected market changes.

According to the Office of the Comptroller of the Currency (OCC), refinancing challenges, changing market conditions, and loan maturity are key risks in commercial real estate lending. Developers should review their repayment strategy and project timeline carefully before relying on short-term financing.

Move Your Development Forward with America Mortgages Bridge Loan Strategy

Delays in funding can slow your project, increase costs, and cause you to miss valuable investment opportunities. If you need quick access to capital for a housing development, the right lending partner can make all the difference.

America Mortgages helps foreign national investors secure financing for U.S. real estate with a simple and efficient process. Our experienced team understands the challenges international buyers face and works with you to find a solution that matches your project and timeline.

Whether you want to buy land, purchase a residential development, or move to long-term financing later, America Mortgages is here to help. Contact our team to discuss your project and funding needs. You can also email [email protected] or call +1 (845) 583-0830 to speak with an experienced lending specialist and explore the right solution for your investment.

FAQs

Q1: Can foreign national investors qualify without U.S. income?

Yes, many foreign national investors can qualify even without U.S. income. Instead, lenders often look at the property’s value, available assets, and your repayment plan. As a result, financing may still be available if you meet the program requirements.

Q2: Can this financing help me buy land for a future project?

Yes, this financing can help you purchase land before construction begins. It gives you quick access to funds while you finalize development plans or arrange long-term financing, helping you move forward without unnecessary delays.

Q3: How is it different from a regular business loan?

This financing is designed specifically for real estate projects, while a regular business loan supports general business needs. It also offers faster funding and focuses more on the property’s value than your business income or operating history.

Q4: Can I use it for renovations or property purchases?

Yes, you can use these funds to buy investment properties, renovate existing buildings, or complete a development before moving to a long-term mortgage. This gives you greater flexibility at different stages of your project.

Q5: How do most investors repay the loan?

Most investors repay the loan by refinancing into a long-term mortgage after the project is complete. Others repay it by selling the property or using rental income once the development begins generating steady returns.