For many U.S. expats in Germany, investing in U.S. real estate is not just a financial move, it’s a long-term strategy for stability, wealth building, and future planning. Whether you’re based in Berlin, Munich, or Frankfurt, owning property in the U.S. allows you to stay connected to a familiar market while benefiting from dollar-based income.

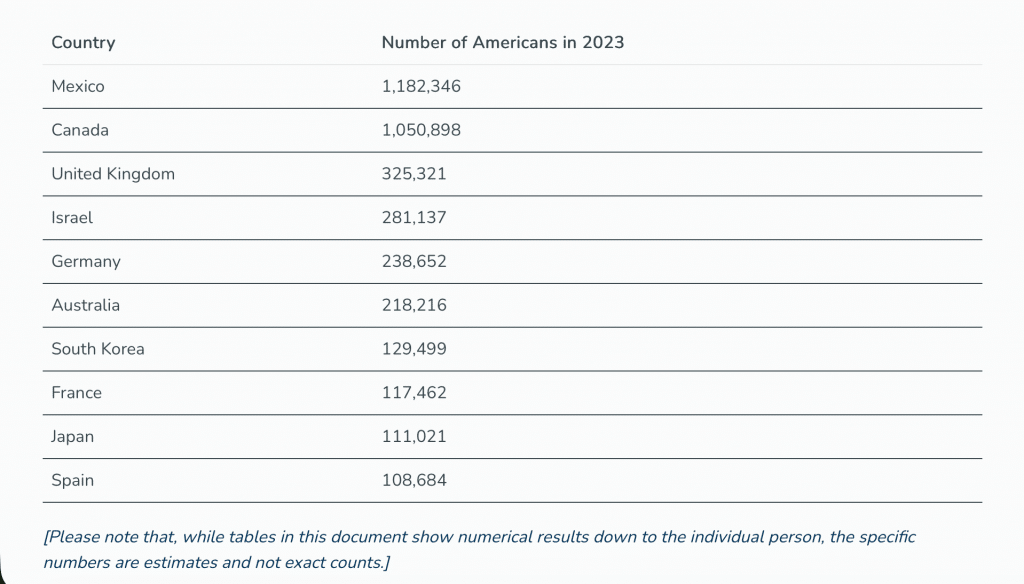

The opportunity is growing. Globally, an estimated 5.5 million Americans live abroad, reflecting a major shift toward international living and investing . Within Europe, Germany remains one of the top destinations, with over 100,000 U.S. citizens and up to 300,000+ Americans including broader residency ties . This growing base of U.S. expats in Germany is increasingly looking back to the U.S. housing market as part of their long-term financial strategy.

What You Will Learn

How U.S. expats in Germany can qualify for a U.S. mortgage

What documents and income requirements lenders actually look for

How foreign income (EUR) is evaluated under underwriting guidelines

The best loan options available for expats living in Germany

Which U.S. markets are attractive for U.S. real estate for expats

How to avoid common mistakes when buying U.S. property from Germany

Why working with a specialized expat mortgage lender changes approval outcomes

Why Are U.S. Expats in Germany Investing in U.S. Real Estate?

Stability, income diversification, and long-term wealth.

Many U.S. expats in Germany are earning in euros but planning in U.S. dollars. U.S. real estate offers a hedge against currency fluctuations while creating opportunities for rental income and long-term appreciation. Additionally, Americans abroad are typically highly educated professionals or retirees, often with global income streams and long-term planning horizons .

Market timing is also playing a role. Many overseas buyers are analyzing trends highlighted in the 2026 U.S. Real Estate Watchlist and early market signals in U.S. real estate. For U.S. expats in Germany, this data-driven approach is critical when making cross-border investment decisions.

Why Do U.S. Expats in Germany Struggle with Traditional U.S. Lenders?

The issue is not your financial strength, it is the system.

After years of advising clients globally, one thing is clear: the U.S. banking system was not designed for expats. Most lenders rely on standardized income verification models, primarily focused on U.S.-based W-2 employment. This creates friction for U.S. expats in Germany, even when they have strong financial profiles.

Traditional lenders struggle to:

Verify foreign currency income

Evaluate non-U.S. employment structures

Accept international tax documentation

This is why many U.S. expats in Germany face unnecessary declines, not because they are unqualified, but because they do not fit rigid domestic underwriting systems.

America Mortgages solves this gap. As the world’s only U.S. international mortgage lender specialist based overseas, and as expats ourselves, we understand how to structure loans that align with your real financial situation.

How Can U.S. Expats in Germany Qualify for a U.S. Mortgage?

Yes, U.S. expats in Germany can qualify, and often more easily with the right lender.

The process focuses on your global financial profile. Lenders evaluate foreign income, assets, and financial consistency rather than rejecting applications due to location. However, one requirement remains constant: U.S. tax returns are essential, even if income is earned abroad.

When applying for a U.S. mortgage from Germany, income earned in euros is converted into USD and assessed for stability. Proper structuring is key, which is why many borrowers work with professionals such as those listed in our guide to top expat accountants for U.S. citizens living overseas.

What Makes America Mortgages Different for U.S. Expats in Germany?

This is where the real advantage lies.

Our mortgage programs are built specifically for U.S. expats in Germany and mirror U.S. bank standards, while adapting to international income structures.

Overseas income and credit accepted

Up to 80% loan-to-value (LTV)

Loan sizes from $150K to $5M

15- and 30-year fixed rates, plus ARM options

30-year amortization regardless of age

Interest-only options for flexible cash flow

This allows U.S. expats in Germany to access financing without being penalized for living abroad. Whether you’re focused on investment or future relocation, the structure supports your goals.

How Does Income Earned in Germany Affect Mortgage Approval?

Income in euros is fully acceptable, but must be evaluated correctly.

For U.S. expats in Germany, lenders convert foreign income into U.S. dollars and analyze consistency over time. Many expats work in multinational roles, which adds credibility to their income profile when properly documented.

The difference lies in expertise. A traditional lender may reject foreign income outright. A specialized expat mortgage lender understands how to interpret international employment structures, making approval far more achievable.

What Are the Best Property Types for U.S. Expats in Germany?

The best property depends on your strategy.

Many U.S. expats in Germany prefer rental properties due to income potential and ease of long-distance ownership. Others invest in second homes or future primary residences in anticipation of relocation.

For investors, options like DSCR loans are particularly relevant. These loans allow qualification based on property income rather than personal income, making them ideal for U.S. real estate for expats building portfolios from abroad.

Which U.S. Markets Are Best for U.S. Expats in Germany?

Market selection is critical.

Many U.S. expats in Germany are targeting growth markets with strong rental demand and population inflows. Cities in Texas, Florida, and Arizona continue to stand out due to affordability and economic expansion.

When buying U.S. property from Germany, the focus should not just be on price, but on long-term fundamentals such as job growth, migration trends, and rental demand.

What Is the Step-by-Step Process for U.S. Expats in Germany?

Define your budget and investment goals

Organize income, tax, and asset documentation

Get pre-approved with an expat-focused lender

Identify target U.S. market and property

Submit an offer and secure financing

Close remotely using digital processes

This streamlined approach allows U.S. expats in Germany to invest in U.S. real estate without unnecessary complexity.

Summary

For U.S. expats in Germany, investing in U.S. property is both achievable and strategic. With millions of Americans living abroad and Germany ranking among the top destinations, the demand for cross-border financing solutions continues to grow.

The key is working with the right lender, understanding underwriting guidelines, and preparing your documentation early. With the right structure, U.S. expats in Germany can access competitive financing and build long-term wealth through U.S. real estate.

Frequently Asked Questions

Q1. Can U.S. expats in Germany get a mortgage in the U.S.?

A: Yes, U.S. expats in Germany can qualify using foreign income, assets, and U.S. tax returns. Specialized lenders are designed to evaluate international borrowers effectively.

Q2. Do I need U.S. tax returns if I live in Germany?

A:A: Yes, U.S. tax returns are typically required. Even when income is earned abroad, lenders rely on these documents for underwriting U.S. expats in Germany.

Q3. Can I use euro income to qualify?

A: Yes, euro income is accepted and converted into USD. Lenders evaluate stability and apply conservative assumptions for U.S. expats in Germany.

Q4. What is the minimum down payment required?

A: Most U.S. expats in Germany can access up to 80% LTV, meaning a 20% down payment is standard depending on the loan program.

Q5. Are DSCR loans suitable for expats?

A: Yes, DSCR loans are ideal for U.S. expats in Germany investing in rental properties since approval is based on property income.

Q6. Can I buy U.S. property remotely?

A: Yes, U.S. expats in Germany can complete purchases remotely through digital processes and structured closing support.

Q7. Why do traditional lenders reject expats?

A: Traditional lenders struggle with foreign income, credit, and documentation, making it harder for U.S. expats in Germany to qualify without specialized programs.

Q8. What property types are best for expats?

A: Rental and long-term investment properties are popular among U.S. expats in Germany due to income potential and flexibility.

Q9. Is now a good time to invest in U.S. real estate?

A: Yes, current market trends and financing conditions make it a strong opportunity for U.S. expats in Germany to invest strategically.

The cost of U.S. education continues to rise, making long-term financial planning essential for international families. Tuition, accommodation, and living expenses can quickly exceed expectations, especially for multi-year programs.

What many families don’t realize is that U.S. real estate can play a strategic role in offsetting these costs. By combining housing needs with investment potential, property ownership can transform education expenses into long-term wealth-building opportunities.

What You Will Learn

How real estate can help reduce education-related expenses

The role of rental income and appreciation in funding tuition

Why buying near universities is a high-demand strategy

How Foreign Nationals and expats can structure financing effectively

How Real Estate Helps Offset Education Costs

One of the most effective ways to reduce the financial burden of studying in the U.S. is by replacing rent with ownership. Instead of paying years of rent with no return, families can build equity while their child studies.

Additionally, U.S. real estate offers two powerful financial benefits:

Rental income: Leasing unused rooms or units can generate monthly cash flow

Property appreciation: U.S. home values have increased significantly over time, with long-term growth exceeding 300% since 1995.

In many cases, rental income alone can cover a meaningful portion of housing or tuition costs. For example, the average U.S. rent ranges from approximately $1,700 to $2,000 per month, depending on property type . This creates a consistent income stream that can directly offset student living expenses.

From an investment perspective, real estate also acts as a hedge against inflation and a diversification tool, helping families preserve and grow capital while managing education costs .

For families planning ahead, this aligns closely with strategies discussed in U.S. real estate market outlook 2026 which highlights long-term market resilience and investment potential.

Why Student Housing Is a Strategic Advantage

Buying property near universities introduces an additional layer of opportunity: high and consistent demand. Student housing remains one of the most stable rental segments in the U.S. market.

This makes it possible to structure a property that not only houses your child but also generates income from other tenants.

For families navigating both visa and housing decisions, this approach connects directly with a clear path to U.S. education. Additionally, student-focused investments allow for flexible strategies such as renting by the room, which can significantly increase total rental income compared to traditional leasing .

Financing Options for Global Buyers

A common misconception is that buying U.S. property requires local employment or a W-2 income. In reality, many lenders offer tailored programs for:

Foreign Nationals: Using documented foreign income, assets, and international credit profiles

U.S. Expats: Qualifying without U.S.-based employment under specific underwriting guidelines

These programs are designed to align with global income structures, making property ownership accessible even before relocation.

The key is working with lenders experienced in cross-border transactions who understand documentation requirements and currency considerations.

Long-Term Wealth vs. Short-Term Expense

Education is typically viewed as a cost, but when paired with real estate, it becomes part of a broader financial strategy.

Instead of:

Paying rent for 4–6 years with no return

Families can:

Build equity

Generate income

Retain an appreciating asset after graduation

Real estate provides multiple layers of financial benefit, including tax advantages, equity growth, and income generation, which together can significantly offset education expenses over time.

How America Mortgages Helps You Align Property Investment with Education Goals

Turning a property purchase into a strategy that supports U.S. education requires more than just financing, it requires the right guidance and structure.

At America Mortgages, we help global families navigate this process by aligning education timelines with real estate investment opportunities. Whether you’re planning ahead or preparing for an upcoming move, our team works with you to structure solutions that fit your profile.

Families benefit from:

Specialized programs for Foreign Nationals and U.S. expats, using foreign income, assets, and credit

Clear guidance on underwriting guidelines, so you know exactly how to prepare

Strategic insights on property types and locations that support both living and income generation

With the right approach, your property can do more than provide housing, it can become a financial tool that supports your child’s education and your long-term investment goals.

If you’re considering this strategy, America Mortgages offers the expertise to help you move forward with clarity and confidence. Get in contact with us at [email protected] or call us now to learn more.

Summary

Buying U.S. property while planning for education is not just about housing, it’s about strategic financial positioning.

By combining rental income, long-term appreciation, and smart financing, families can reduce the net cost of education while building a valuable asset in one of the world’s most stable real estate markets.

For Foreign Nationals and U.S. expats, this approach offers a unique advantage: turning a necessary expense into a long-term investment opportunity.

Frequently Asked Questions

Q1: Can rental income really offset education costs?

A: Yes. In many cases, rental income can cover a significant portion of housing expenses or even contribute toward tuition, depending on the property and location.

Q2: Is buying near a university a good strategy?

A: Absolutely. Student housing typically offers strong demand, consistent occupancy, and higher rental yield potential compared to standard residential properties.

Q3: Can Foreign Nationals qualify for U.S. mortgages?

A: Yes. Many lenders offer programs that allow Foreign Nationals to qualify using foreign income, assets, and credit profiles under specific underwriting guidelines.

Q4: What happens after graduation?

A: Families can continue renting the property for income, sell for potential appreciation gains, or convert it into a long-term investment asset.

Q5: Is it better to buy a property before or after the student moves to the U.S.?

A: Ideally, purchasing before arrival allows families to secure better locations and avoid rising rental costs. It also provides time to prepare the property for occupancy or rental income generation from day one.

Q6: What type of property works best for offsetting education costs?

A: Properties near universities—such as condos, townhomes, or small multi-unit residences—tend to perform best. These allow for flexible rental strategies, including renting to other students, which can maximize income potential.

Q7: Are there risks involved in using real estate to offset education costs?

A: Like any investment, real estate carries risks such as market fluctuations, vacancy periods, and maintenance costs. However, choosing strong locations, especially near universities, and working with experienced lenders can significantly reduce these risks.

What You Will Learn

Which top U.S. cities to buy property near major universities offer the strongest returns

Why student housing investment USA remains stable even during downturns

How to choose the right property near universities USA for long-term value

Strategic insights for U.S. residents, expats, and foreign nationals

Why Are the Top U.S. Cities to Buy Property Near Major Universities So Profitable in 2026?

The top U.S. cities to buy property near major universities continue to outperform traditional residential markets because they benefit from one of the most reliable demand drivers in real estate: education.

With more than 19 million students enrolled across U.S. institutions, according to the National Center for Education Statistics, demand for off-campus housing remains consistently high. Unlike conventional rental markets, university-driven demand refreshes every academic year, ensuring a steady tenant pipeline.

What makes the top U.S. cities to buy property near major universities particularly attractive is their resilience. Even during economic downturns, enrollment often rises, which directly supports rental demand. Data from CBRE’s student housing outlook shows occupancy rates in prime university markets exceeding 95%, reinforcing the strength of this asset class.

For families planning long-term education strategies, property ownership can also reduce housing uncertainty. This aligns with planning approaches outlined in how families secure the f-1 student visa and plan long-term housing, where real estate becomes part of a broader education investment strategy.

Which Are the Top U.S. Cities to Buy Property Near Major Universities in 2026? (High ROI + Demand Ranked)

The top U.S. cities to buy property near major universities are not just defined by student numbers, they combine economic growth, housing constraints, and long-term appreciation trends.

Austin, Texas – Why Is It One of the Best University Property Markets?

Austin stands out due to its rapid population growth and thriving tech economy. The University of Texas alone enrolls over 50,000 students, creating sustained rental demand. Investors benefit from strong appreciation combined with solid rental yields, making it one of the most balanced markets in the U.S.

Boston, Massachusetts – Is This the Most Stable Student Housing Market?

Boston is one of the most established education hubs globally, home to Harvard, MIT, and Boston University. The city’s limited housing supply and strong international student demand support premium rental pricing. According to the U.S. Census Bureau, Boston maintains one of the highest renter populations in the country, reinforcing its long-term stability.

Raleigh-Durham, North Carolina – Why Is the Research Triangle Growing Fast?

This region combines top universities with a booming tech and healthcare sector. Duke, UNC, and NC State create a diverse and steady tenant base. Property prices are still relatively accessible, offering investors strong appreciation potential alongside rental demand.

Ann Arbor, Michigan – What Makes This a Classic High-Performing College Town?

Ann Arbor’s real estate market is heavily supported by the University of Michigan. Demand remains strong due to limited housing inventory and a high concentration of students. Properties here tend to retain value well, making them attractive for long-term investors.

Gainesville, Florida – Is This One of the Best Cash Flow Markets?

Gainesville offers a lower entry point compared to larger cities, while still benefiting from strong demand driven by the University of Florida. Investors often achieve higher rental yields here, making it ideal for those focused on income rather than appreciation alone.

Los Angeles, California – Why Do Global Investors Target This Market?

Los Angeles combines world-class universities like UCLA and USC with international demand. While entry costs are higher, the market offers strong appreciation potential and consistent rental demand from both domestic and international students.

Madison, Wisconsin – Is This a Stable Low-Volatility Market?

Madison provides a balanced mix of affordability and demand. The University of Wisconsin supports a consistent rental base, while the city’s stable economy keeps vacancy rates low. It’s a strong option for conservative investors.

Columbus, Ohio – Why Is Scale Driving Opportunity Here?

With over 60,000 students at Ohio State University, Columbus has one of the largest student populations in the country. This scale creates reliable demand and makes it easier to maintain occupancy across different property types.

Phoenix, Arizona – Is This a High-Growth University Market?

Arizona State University is one of the largest in the U.S., and Phoenix continues to attract new residents and investors. The combination of population growth and student demand makes it one of the fastest-growing university real estate markets.

How to Choose the Right Property Near Universities (Investor + Family Strategy Guide)

Choosing from the top U.S. cities to buy property near major universities requires more than just selecting a well-known school. The success of an investment depends on how well the property aligns with student behavior and local market dynamics.

Properties located within walking distance or a short commute to campus tend to command higher rents and experience lower vacancy rates. Investors also benefit from selecting layouts that support shared living, as renting by the room can significantly increase total income.

Families planning education pathways often integrate real estate decisions into their broader strategy. Resources like best boarding schools in the U.S. highlight how early planning can influence both education and housing choices.

Ready to Invest in the Top U.S. Cities to Buy Property Near Major Universities? Here’s How America Mortgages Can Help

Investing in the top U.S. cities to buy property near major universities is not just about choosing the right location, it’s about securing the right financing strategy that aligns with your long-term goals.

U.S. residents structure competitive financing for student housing investments

U.S. expats leverage global income while meeting U.S. underwriting guidelines

Foreign nationals navigate documentation requirements for foreign income, assets, and credit

Whether you’re purchasing property for rental income, your child’s education, or long-term portfolio growth, our team provides clear guidance tailored to your profile.

We don’t just offer mortgage solutions, we help you align your investment with education planning, currency considerations, and cross-border financial strategy.

If you’re exploring opportunities in the top U.S. cities to buy property near major universities, now is the right time to understand what financing options are realistically available to you.

Get in contact with an America Mortgages expert to evaluate your eligibility and structure the right loan strategy for your investment. Email us at [email protected] to reach out directly.

Summary

The top U.S. cities to buy property near major universities offer a rare combination of consistent demand, strong rental income, and long-term appreciation.

For U.S. residents, these markets provide reliable cash flow. For U.S. expats, they offer a strategic way to align housing with education planning. For foreign nationals, they represent one of the most accessible entry points into U.S. real estate, provided they meet underwriting guidelines by documenting foreign income, assets, and credit.

In 2026, university-driven markets remain one of the most resilient and value-driven real estate strategies available.

Frequently Asked Questions

Q1: What are the top U.S. cities to buy property near major universities in 2026?

A: Cities like Austin, Boston, Raleigh-Durham, and Phoenix lead due to strong student demand and economic growth. These markets combine rental stability with appreciation potential. Investors prioritize cities with large universities and limited housing supply.

Q2: Why is student housing investment USA considered stable?

A: Student housing benefits from recurring demand tied to academic cycles. Even during economic downturns, enrollment often increases. This keeps occupancy rates high and reduces investment risk.

Q3: Is buying property near universities better than traditional rentals?

A: In many cases, yes. University properties often allow room-by-room rental, increasing income potential. They also experience lower vacancy due to consistent student demand.

Q4: Which cities offer the highest rental yields near universities?

A: Markets like Gainesville, Columbus, and Phoenix typically offer higher yields due to lower entry prices. While premium cities offer appreciation, these markets focus more on cash flow.

Q5: Can foreign nationals invest in U.S. student housing markets?

A: Yes, foreign nationals can purchase property in the U.S. They must meet underwriting guidelines by documenting foreign income, assets, and credit. Financing options vary depending on their profile.

Q6: What type of property works best near universities?

A: Properties designed for shared living tend to perform best. Multi-bedroom homes and condos near campus are particularly effective. These maximize rental income and reduce vacancy risk.

Q7: How important is location within a university city?

A: Location is critical. Properties closer to campus or public transport attract higher rents. Distance directly impacts occupancy rates and long-term value.

Q8: Are university real estate markets affected by recessions?

A: They are generally more resilient than traditional markets. Education demand often increases during downturns. This helps sustain rental demand and occupancy levels.

Q9: Should families buy property instead of renting for students?

A: For long-term stays, buying can be more cost-effective. It provides stability and potential appreciation. Many families use this approach to offset education-related housing costs.

How Global Investors Access California Real Estate Finance — The Complete Guide by America Mortgages

Key Takeaways

Foreign nationals can qualify for hard money bridge loans on California real estate and the process is more straightforward than most international investors expect.

Asset-based underwriting is uniquely suited to foreign national borrowers. No US credit history, no US income, and no US tax returns are required.

Entity structure whether a US LLC, foreign corporation, or offshore trust dramatically affects both mortgage availability and tax exposure. Getting this right before acquisition is critical.

America Mortgages and GMG Capital have closed California bridge loans for investors from more than 40 countries.

California’s market velocity makes the speed of hard money financing a decisive competitive advantage for foreign national investors.

Introduction: Why California Is the #1 US Market for Foreign Real Estate Investment

Foreign nationals invest more in California real estate than in any other US state and have for decades. The reasons are well understood: world-class cities, technology economy growth, cultural diversity, and an established international investment community that makes California uniquely welcoming to global capital.

What is less well understood is how foreign nationals actually finance California real estate acquisitions, particularly in the fast-moving situations where conventional bank financing is unavailable, too slow, or inaccessible due to the borrower’s non-US financial profile.

Hard money bridge loans are the answer. And for foreign national investors, the asset-based underwriting approach of hard money lending is not a workaround, it is ideally suited to their situation. A lender who qualifies the loan on the California property value rather than the borrower’s US tax returns, US credit score, or US employment history is precisely what an international investor needs.

This guide, developed by America Mortgages’ international specialists, explains exactly how foreign national investors access California hard money bridge financing including entity structures, documentation requirements, deal types, and the specific advantages that GMG Capital and America Mortgages bring to international borrowers.

Part 1: Why Hard Money Is Ideal for Foreign National California Buyers

The Conventional Bank Problem for Foreign Nationals

Major US banks like JPMorgan Chase, Wells Fargo, and Bank of America have largely withdrawn from foreign national mortgage lending for investment properties. Those that remain impose requirements that are genuinely difficult for international investors to meet:

US credit score (FICO) requirement: most foreign nationals have none

US income documentation: foreign income is difficult or impossible to verify through standard bank channels

US tax return requirements: foreign nationals typically have no US tax returns

Long processing timelines of 45 to 90 days: incompatible with California’s competitive market

Loan size limitations: many bank programs cap out at $2 million to $3 million for foreign national borrowers

Why Hard Money Solves Every One of These Problems

The table below summarises how hard money bridge lending addresses each barrier that conventional banks create for international borrowers.

Bank Requirement

Foreign National Problem

Hard Money Solution

US Credit Score (FICO)

Foreign nationals have no US credit history

Asset-based underwriting — no US credit required

US Income Documentation

Foreign income is difficult to verify through US bank channels

Income not verified — property value qualifies the loan

US Tax Returns

Foreign nationals typically have no US tax returns

No tax return requirement for most hard money programs

45-90 Day Timeline

Too slow for California’s competitive market

10-21 day close — cash-competitive speed

$2-3M Loan Cap for Foreign Nationals

Limits larger acquisitions and portfolio building

No practical maximum with global capital access via GMG Capital

US LLC/Entity Requirement

Creates tax complexity for international investors

Hard money lenders accept various entity structures with guidance

The Foreign National Hard Money Advantage For a foreign national investor, a hard money bridge loan is often the optimal financing tool — not a compromise. It closes faster, requires no US financial documentation, accepts offshore entity ownership, and with lenders like GMG Capital and America Mortgages, carries no practical loan size ceiling. The higher rate is the price of speed, flexibility, and certainty — all of which have real dollar value in California’s competitive market.

Part 2: Entity Structure for Foreign National California Investors

The Three Most Common Structures and Their Mortgage Implications

Before securing a California hard money bridge loan, foreign national investors must decide on their ownership structure. This decision has implications for mortgage availability, California tax exposure, US estate tax, and liability protection. America Mortgages works with international tax specialists to help clients make this decision before they need financing — not after.

Structure 1: US LLC (Most Common and Most Lender-Friendly)

A US Limited Liability Company (LLC) formed in Delaware, California, or Wyoming is the most widely accepted entity structure for California hard money bridge loans.

Accepted by nearly all California hard money lenders, including GMG Capital

Provides liability protection, limits personal exposure to the property

Pass-through taxation, no entity-level tax; income flows to the member’s tax return

Relatively simple and inexpensive to form and maintain

Requires an Employer Identification Number (EIN) from the IRS, which is obtainable by foreign nationals

Important: US Estate Tax Warning for US LLC Owned by Foreign Nationals A foreign national’s membership interest in a US LLC that owns California real estate is considered a US-situs asset for estate tax purposes. Foreign nationals have only a $60,000 US estate tax exemption, compared with $13.6 million for US citizens. On a $2 million California property, this represents potential estate tax exposure of up to $776,000. This risk must be addressed at the entity structure stage.

Structure 2: Foreign Corporation Owning a US LLC (Blocker Corporation Structure)

A more sophisticated structure for many foreign national investors: a foreign corporation typically registered in the investor’s home country or a favorable jurisdiction such as the Cayman Islands, British Virgin Islands, or Singapore; owns the US LLC, which in turn owns the California property.

Significantly reduces or eliminates US estate tax exposure, the estate asset is a foreign corporate share, not a direct US real property interest

More complex to administer annual US tax filings (Form 5472) are required

Harder to finance, most hard money lenders require specialised review; GMG Capital and America Mortgages have structured loans for this configuration

Requires a US CPA and international tax attorney

Structure 3: Personal Name (Simplest but Most Problematic)

Purchasing in the foreign national’s personal name is the simplest administrative approach but the most problematic from a tax and estate perspective. It is only appropriate for investors who have explicit written advice from a US international tax attorney confirming it is suitable for their individual situation.

Entity Structure Decision Framework

Factor

US LLC

Foreign Corp + US LLC

Personal Name

Mortgage Availability

Excellent — most lenders

Good — specialist lenders required

Good — specialist lenders

US Estate Tax Exposure

High (only $60K exemption)

Low to None

High (only $60K exemption)

Liability Protection

Yes

Yes (double layer)

No

Administrative Complexity

Low

High

Very Low

Annual Tax Filings

Form 1065 or Schedule E

Forms 5472, 1120, 1065

Form 1040-NR

Recommended For

Most investors, smaller portfolios

Larger investors, estate planning focus

Only with specific legal advice

Part 3: California Hard Money Bridge Loan Programs for Foreign Nationals

Program Types Available to International Investors

Program Type

Key Feature

Documentation Required

Best For

Pure Asset-Based Bridge

No income or credit verification

Passport, entity docs, down payment source

Clean property, clear exit, experienced investor

DSCR Bridge (Investment Property)

Rental income covers loan payment

Rental income projection or signed lease

Income-producing properties

Cross-Border Bridge

Accepts foreign income and assets

Foreign bank statements, international wealth documentation

High-net-worth investors with strong global financial profile

Construction Bridge

Ground-up or major renovation

Project budget, contractor credentials, development experience

Experienced developers with entitlements in hand

Portfolio Bridge

Multiple CA properties, single loan

Full portfolio documentation, entity structure review

Experienced investors scaling California portfolios

Documentation Requirements for Foreign National California Bridge Loans

Compared with conventional mortgage lending, hard money bridge loans require significantly less documentation. For foreign nationals specifically, the typical requirements are:

Valid passport: all pages, including all visa stamps

Entity documents (if borrowing through a US LLC): Articles of Organization, Operating Agreement, and the EIN confirmation letter from the IRS

Proof of funds for down payment and reserves: Foreign bank statements covering 3 to 6 months, investment account statements, or a bank reference letter from a tier-1 institution

Property information: Address, basic description, and a preliminary title report if available

Exit strategy documentation: Comparable sales for a sale exit, or preliminary interest from a permanent lender for a refinance exit

Foreign corporation documents (if applicable): Certificate of incorporation, director identification, and a registered agent in the home country

What Foreign National Hard Money Borrowers Do NOT Need

US credit score or FICO report

US tax returns (Form 1040 or 1040-NR)

US employment verification

US income documentation

ITIN (helpful but not always required)

An existing US banking relationship though funds must ultimately be held in a US account for closing

Part 4: California Markets by Foreign National Investor Origin

Where Different International Communities Invest in California

Investor Origin

Primary California Markets

Preferred Asset Types

Typical Deal Size

Chinese / Hong Kong

San Gabriel Valley, Bay Area, Irvine

Residential, condo, multifamily

$500K – $5M

Canadian

Los Angeles, San Diego, Palm Springs

Vacation/short-term rental, residential

$500K – $3M

UK / European

Los Angeles, San Francisco, Wine Country

Luxury residential, commercial

$1M – $15M

Australian

Los Angeles, San Diego, Bay Area

Residential, hospitality

$500K – $5M

Middle Eastern / GCC

Beverly Hills, Santa Barbara, San Francisco

Ultra-luxury residential, commercial

$3M – $50M+

Korean

Los Angeles (Koreatown), Bay Area

Commercial, multifamily, mixed-use

$1M – $10M

Indian / South Asian

Bay Area (Silicon Valley), LA

Residential, commercial

$500K – $5M

Latin American

Los Angeles, Orange County

Residential, commercial

$500K – $10M

Part 5: The Foreign National California Bridge Loan Process (Step by Step)

Step 1: Initial Consultation with America Mortgages (Day 1) Contact the America Mortgages international specialist team. Describe your investment objective, property type, target market, and approximate deal size. Specialists are available across all global time zones and speak multiple languages.

Step 2: Entity Structure Review (Days 1 to 7) Before the loan process begins, America Mortgages reviews your proposed entity structure or helps you establish the right one in coordination with US international tax specialists.

Step 3: Deal Identification and Term Sheet Request (As Soon as the Property Is Identified) Once a property is in mind, submit a brief deal summary. America Mortgages and GMG Capital provide preliminary term sheets within 24 to 48 hours.

Step 4: Documentation Preparation (Days 3 to 7) Prepare the documentation package using the checklist above. America Mortgages provides a customised checklist based on your specific country of origin and entity structure.

Step 5: Appraisal and Title (Days 5 to 14) The lender orders an appraisal from a California-licensed MAI appraiser. The title company begins the preliminary title search. Both can run simultaneously with document review.

Step 6: Underwriting and Approval (Days 7 to 14) GMG Capital’s underwriting team reviews the property analysis and documentation. For foreign national bridge deals, approval is typically faster because income documentation review is not required.

Step 7: Closing Preparation (Days 14 to 20) Loan documents are prepared. Funds are confirmed in a US escrow account. Foreign national investors must wire funds to US title/escrow from a verifiable foreign bank account — source of funds documentation is required for AML compliance.

Step 8: Funding and Closing (Days 20 to 21) The loan funds. The deed is recorded. The bridge period begins.

Important: Source of Funds Documentation California escrow companies and lenders are required to comply with the US Bank Secrecy Act and Anti-Money Laundering (AML) regulations. International wire transfers from foreign bank accounts require source-of-funds documentation typically a bank reference letter and account history showing the origin of the down payment and reserves. America Mortgages guides clients through this process to prevent delays at closing.

Part 6: FIRPTA, California Tax, and Exit Strategy for Foreign Nationals

FIRPTA at Exit – The Tax Foreign Investors Must Plan For

When a foreign national sells California real estate, the buyer’s agent is required to withhold 15% of the gross sales price and remit it to the IRS under the Foreign Investment in Real Property Tax Act (FIRPTA). Key points:

The 15% withholding applies to the gross price, not the gain. A foreign investor who sells at a $100,000 loss on a $2 million property still has $300,000 withheld.

The withholding is a prepayment of tax, not a final liability. Filing a US tax return (Form 1040-NR) after the sale allows the investor to calculate actual tax liability and claim a refund of over-withheld amounts.

California imposes an additional 3.33% withholding on top of the federal 15%, meaning total withholding at closing can reach 18.33% of the gross sale price.

Withholding can be reduced or eliminated in certain situations — for example, where the sale price is under $300,000 and the buyer intends to use the property as a primary residence, or where a qualified withholding certificate is obtained from the IRS. These require planning before the sale.

California Rental Income Tax for Foreign Nationals

If the California property generates rental income during the bridge period or is converted to a rental after exit foreign nationals are subject to US and California income tax on net rental income. The most tax-efficient approach is to:

File a US tax return (Form 1040-NR) electing to treat rental income as effectively connected income (ECI)

Deduct all allowable expenses: mortgage interest, property tax, insurance, management fees, and depreciation (27.5 years for residential; 39 years for commercial)

Use depreciation deductions, which often create a net paper loss despite positive cash flow, thereby reducing or eliminating US tax on rental income

Common Mistakes Foreign National Investors Make in California Bridge Lending

Wrong entity structure at acquisition. Restructuring after purchase triggers California transfer taxes (0.11% to 1.1% of value) and potential tax complications. Establish the right structure before acquisition.

Insufficient US-account liquidity at closing. Down payment and reserves must be in a US bank account before closing. Wire funds early — international transfers can take 5 to 10 business days and may trigger AML review.

Not budgeting for FIRPTA at exit. Model the 15% gross withholding into your exit return projections from day one. Many foreign investors are surprised by the scale of this withholding.

Choosing a lender without international borrower experience. A California hard money lender who has never processed a foreign national loan will create delays and errors. America Mortgages and GMG Capital have managed hundreds of international borrower closings.

Ignoring California estate tax exposure. The $60,000 US estate tax exemption for foreign nationals is not theoretical — it affects every investor who owns California real estate in a personal name or US LLC. Address this at the structure stage.

Not having a US-based property management team. Remote management from abroad creates legal, maintenance, and tenant management risks. California’s tenant protection laws require sophisticated local management. The California Department of Real Estate provides licensee information for vetting local managers.

Future Trends for Foreign National California Bridge Lending

Digital Verification Platforms: New international KYC and AML platforms are reducing the time required to verify foreign national borrower identity and source of funds, shrinking closing timelines further.

Expanding Global Capital Sources: More Asian, Middle Eastern, and European institutional capital is being deployed into US private real estate debt, increasing lender competition and improving terms for foreign national borrowers.

Offshore Entity Lending Expansion: More US hard money lenders are developing structured products for foreign corporation and offshore trust entity ownership, reducing the complexity that currently requires specialist lenders like GMG Capital and America Mortgages.

FIRPTA Reform Discussions: Congress periodically discusses FIRPTA reform. Any reduction in the withholding rate or expansion of exemptions would meaningfully improve California’s appeal to foreign national investors.

Cross-Border PropTech: Real estate technology platforms enabling foreign nationals to identify, underwrite, and close California properties remotely with integrated bridge financing are emerging and will change how international investors access the market.

Frequently Asked Questions

Q1: Can a foreign national get a hard money bridge loan in California without a US credit score?

Yes. Hard money bridge loans are underwritten primarily on California property value, not the borrower’s US credit history. Foreign nationals with no US credit score, no FICO score, and no US financial history can qualify based on asset quality, loan-to-value ratio, and exit strategy strength. This is one of the core advantages of hard money lending for international investors.

Q2: What is the minimum down payment for a foreign national hard money bridge loan in California?

Most California hard money lenders require a 25% to 35% down payment from foreign national borrowers (65% to 75% LTV). Higher down payments of 30% or more often unlock better rates and faster processing. Some programs allow up to 75% LTV for strong assets with clear exit strategies and experienced borrowers.

Q3: How does America Mortgages handle non-English documentation from foreign national borrowers?

America Mortgages works with certified translation services and has multilingual specialists on staff. Foreign bank statements, income documents, and entity paperwork can be submitted in the original language. America Mortgages manages the translation and certification process as part of its loan origination service.

Q4: Can a foreign national get a bridge loan for a California Airbnb or short-term rental property?

Yes, and this is one of the most active segments for foreign national bridge lending. California markets including Palm Springs, Lake Tahoe, Big Bear, and the Wine Country have robust short-term rental markets that attract international investors. Specialist lenders in the GMG Capital and America Mortgages network accept AirDNA market data for underwriting short-term rental income on bridge deals.

Q5: Do foreign national hard money borrowers need an ITIN?

An Individual Taxpayer Identification Number (ITIN) is helpful but not universally required for hard money bridge loans. It is required for US tax return filing, which is necessary if you earn rental income or sell the property. America Mortgages recommends applying for an ITIN early in the process. It can be obtained via IRS Form W-7 through a Certified Acceptance Agent, a process that typically takes 6 to 10 weeks.

Q6: How do GMG Capital and America Mortgages differ from other hard money lenders for foreign nationals?

Three key differentiators: First, international borrower expertise; America Mortgages has processed loans for borrowers from more than 40 countries and understands the documentation, entity structure, and AML considerations for each market. Second, global capital depth GMG Capital can fund deals of any size without the syndication delays that constrain local lenders. Third, full-service capability from entity structure advice to loan origination to connection with international tax specialists, the service extends well beyond the loan itself.

Ready to Discuss Your California Investment?

America Mortgages serves international investors 24 hours a day across all time zones. Whether you are in Singapore, London, Dubai, Hong Kong, or Sydney and whether your California deal is $500,000 or $50,000,000, a specialist is available to discuss your financing options, review your deal structure, and provide a preliminary term sheet within 24 to 48 hours.

Deal Structures, Market-by-Market Strategy, and the Professional’s Framework for Maximizing Bridge Capital

Key Takeaways

Successful California investors treat hard money as a tool, not a crutch — the deal structure determines success, not the financing source.

Market selection matters: different California markets require different bridge strategies and exit timelines.

The fix-and-flip, value-add multifamily, and 1031 exchange bridge are the three dominant use cases — each with distinct structuring requirements.

Seasoned investors have lender relationships established before they need them — particularly with global-capital lenders like GMG and America Mortgages.

The investors who scale in California are those who master the acquisition-bridge-stabilize-refinance cycle repeatedly.

The California Hard Money Bridge Loan Playbook: Strategy, Structures, and Scaling

Introduction: The Investor Who Masters the Bridge Cycle Wins

The most successful California real estate investors share a common framework: they acquire undervalued or underperforming assets using bridge capital, execute a value-creation plan during the bridge period, and exit or refinance into long-term financing at improved values. Repeat.

This cycle: acquire, bridge, reposition, exit/refinance, is the engine of California real estate wealth creation. The hard money bridge loan is the fuel. And the investors who understand how to use that fuel efficiently, structuring their deals correctly, choosing the right lender, managing the bridge period strategically, generate returns that conventional borrowers simply cannot access.

This article is the strategic playbook for that process.

Part 1: The Three Core Bridge Loan Strategies in California

Strategy 1: The Fix-and-Flip Bridge

The fix-and-flip is California’s most-executed bridge strategy. An investor acquires a distressed residential property below market value, renovates it to comparable standards, and sells for a profit within 6-12 months. The bridge loan funds both the acquisition and, in many cases, the renovation costs.

The Fix-and-Flip Financial Model

Variable

Conservative Case

Base Case

Strong Case

Purchase Price

$750,000

$900,000

$1,100,000

Renovation Budget

$120,000

$150,000

$180,000

Total Cost Basis

$870,000

$1,050,000

$1,280,000

ARV (Comparable Sales)

$1,200,000

$1,500,000

$1,850,000

Bridge Loan (70% ARV)

$840,000

$1,050,000

$1,295,000

Borrower Equity Required

$30,000

$0

Lender funds all costs

Projected Net Profit (after all costs)

$180,000 – $230,000

$280,000 – $340,000

$400,000 – $480,000

Annualized ROI on Equity

55% – 70%

Infinite (no equity in)

N/A — all debt

The California Fix-and-Flip Cost Stack Beyond the bridge loan, investors must model: California transfer tax (varies by county — up to 1.1% in LA City), agent commissions (typically 5-6% on the sale), escrow and title costs (0.5-1%), holding costs (insurance, utilities, property tax during bridge period), and the bridge loan interest and fees. A fully loaded pro forma is essential before committing to any acquisition.

Strategy 2: Value-Add Multifamily Bridge

California’s housing shortage and chronic rent growth make value-add multifamily one of the most institutionally validated real estate strategies in the state. An investor acquires an underrented apartment building, often with below-market tenants, deferred maintenance, and outdated unit interiors, and renovates to bring rents to market. The bridge loan funds the acquisition and renovation; the exit is a permanent agency loan (Freddie Mac, Fannie Mae) or CMBS once the property is stabilized.

Value-Add Underwriting Framework

Current State Analysis: What is the property producing today? Current gross rents, vacancy, operating expenses, and resulting NOI.

Renovation Scope: Unit-by-unit renovation cost. In California, kitchen and bathroom renovations typically justify $200-500/month rent premiums per unit.

Stabilized State Projection: Post-renovation occupancy (target 95%+), market rents (supported by comparable recently renovated properties), and projected stabilized NOI.

Cap Rate Exit: Apply a market cap rate to the stabilized NOI to determine projected stabilized value. This is the value the permanent lender will underwrite to.

Bridge Loan Sizing: Most lenders will fund 70-75% of current value, with additional holdback for renovation costs funded in draws.

California Value-Add Multifamily Example 12-unit apartment building in Oakland | Current Rents: $18,000/month gross | Current NOI: $126,000/year | Current Value (at 7% cap): $1,800,000 | Renovation: $8,000/unit x 12 = $96,000 | Post-Renovation Market Rents: $26,400/month | Stabilized NOI: $196,800/year | Stabilized Value (at 6.5% cap): $3,027,000 | Bridge Loan: $1,350,000 (75% of current value) + $96,000 renovation holdback | Permanent Loan at 70% stabilized value: $2,118,900 — pays off the bridge with significant equity creation.

Strategy 3: The 1031 Exchange Bridge

Section 1031 of the Internal Revenue Code allows investors to defer capital gains taxes by rolling proceeds from a sold property into a ‘like-kind’ replacement property. The rules are strict: the replacement property must be identified within 45 days of the relinquished sale and closed within 180 days.

Here’s the problem: California’s most competitive properties trade fast. An investor who has identified the perfect replacement property, but whose equity is still tied up in escrow on the relinquished property, or who faces competition from all-cash buyers, cannot wait for conventional financing. The bridge loan is the solution.

Exchange Bridge Loan Use Case 1: Equity Advance — Borrower draws a bridge loan against the identified replacement property while their 1031 proceeds are in transit. The exchange completes, 1031 funds pay off the bridge.

Exchange Bridge Loan Use Case 2: Competitive Acquisition — Bridge loan allows investor to close the replacement property as a cash-equivalent buyer (7-14 day close). After acquisition, conventional financing replaces the bridge.

Exchange Bridge Loan Use Case 3: Improvement Exchange — Bridge funds acquisition of replacement property, renovation funds bring the basis up to the required equal-or-greater replacement value under 1031 rules.

Part 2: California Market-by-Market Bridge Strategy Guide

Long commute risk for residential; industrial fundamentals strong

$500K – $15M

Part 3: The Professional’s Due Diligence Framework for California Bridge Deals

Pre-Acquisition Due Diligence Checklist

Title Search: Order a preliminary title report before going under contract. Mechanics’ liens, lis pendens, HOA disputes, and easements are California’s most common title deal-killers.

Permit History: Pull the property’s permit history from the city/county building department. Unpermitted additions are common in California — they must either be legalized (expensive) or disclosed to buyers (value-reducing).

Rent Control Analysis: Understand exactly which units are subject to local rent control (LA RSO, SF Rent Ordinance) and state rent control (AB 1482 for buildings 15+ years old). This determines your income upside potential.

Environmental Screening: Phase I Environmental Site Assessment for commercial properties and any residential with prior commercial use. California’s strict liability for environmental contamination (Proposition 65 etc.) makes environmental due diligence non-optional.

Comparable Sales Analysis: Pull the last 6-12 months of comparable sales within 0.5 miles. In California, micro-location matters enormously, comps from adjacent neighborhoods can be misleading.

Contractor Bids: For renovation projects, obtain at least two independent contractor bids before finalizing the bridge loan request. California construction costs are highly variable and lenders will scrutinize your renovation budget.

Market Rent Survey: For income-producing properties, conduct a current market rent survey with at least 5 comparable properties. This is your stabilized income foundation.

Part 4: Managing the Bridge Period — What Nobody Tells You

The Bridge Period Is Where Deals Win or Lose

Most articles on hard money bridge loans focus on the acquisition, the loan terms, the closing process. Far less attention is paid to the bridge period itself: the months between loan funding and exit. This is where investor discipline, project management, and market awareness determine whether you make a profit or sustain a loss.

Bridge Period Management Principles

Start Your Exit Before Your Bridge Closes: If your exit is a sale, have your real estate agent actively preparing comps, a marketing strategy, and a listing timeline from day one of the bridge period, not month 10 of a 12-month loan.

Begin Takeout Lender Conversations on Day One: If your exit is a permanent refinance, engage conventional lenders (agencies, banks, CMBS lenders) immediately after closing the bridge. Know exactly what stabilization metrics they require for approval.

Maintain Reserve Liquidity: Unexpected costs during the bridge period are not the exception — they are the rule in California construction and renovation. Maintain your post-closing reserves in liquid form throughout the bridge period.

Monitor Extension Options: Negotiate extension options before you need them. Most California hard money lenders offer 3-6 month extensions at a fee (0.25-1.0%). Understand your extension rights and costs before closing, not when your loan is expiring.

Communicate Proactively With Your Lender: Hard money lenders who are kept informed of project progress are significantly more flexible when issues arise. Surprises — especially negative ones — damage the relationship and your ability to get extensions or additional draws.

The Bridge Period Timeline — A Framework Month 1-3: Acquisition, construction mobilization, design/permit finalization | Month 3-8: Active renovation or repositioning; monthly draw requests if applicable | Month 6-9: Begin exit strategy execution — listing preparation OR stabilization for refi | Month 9-11: Exit in process — property on market or takeout lender committed | Month 12: Exit complete — bridge loan repaid. If timeline extends, extension negotiated before month 12.

Part 5: Scaling from One Deal to a Portfolio — Using Bridge Capital Strategically

The investors who use California hard money bridge loans most effectively are not doing single deals in isolation. They are building portfolio momentum, using each successful bridge transaction to access better terms, larger loans, and more capital for the next deal.

The Portfolio Momentum Cycle

Deal 1: Establish the Relationship. Accept slightly less optimal terms. Close on time. Manage the bridge period professionally. Exit as planned. Pay off the loan.

Deal 2: Leverage the Track Record. Reference your successful Deal 1 exit. Request marginally better terms — lower rate, higher LTV. Build the relationship with the same lender.

Deal 3-5: Unlock Scale and Capital Depth. With two or three successful exits documented, lenders like GMG Capital will engage you as a preferred borrower — better rates, faster processing, higher loan amounts, and access to products not available to new borrowers.

Portfolio Stage: Cross-Collateralized Programs. Experienced operators with established lender relationships can access cross-collateralized portfolio bridge facilities, a single loan structure spanning multiple properties — with capital efficiency unavailable to individual deal borrowers.

Why Lender Relationship Matters at Scale A real estate operator who has done 8 successful California bridge transactions with GMG Capital does not apply for the 9th loan like a new borrower. They call their relationship manager, describe the deal, and receive a term sheet within hours — often with terms unavailable in the open market. This relationship capital is one of the most undervalued assets in professional real estate investment.

Common Mistakes in California Bridge Loan Strategy

Buying at the Wrong Basis. No bridge loan can fix an overpaid acquisition. California’s market is competitive, but discipline at purchase is the foundation of every successful bridge strategy.

Underestimating California Holding Costs. Property taxes (even at Prop 13 base), insurance (increasingly expensive in California), utilities, and security during renovation all add up. Model them accurately.

Not Stress-Testing the Exit. What happens if the market cools 10% during your bridge period? Does your profit disappear? Does your LTV for the takeout refinance fall below threshold? Stress-test your exit at both conservative and base cases.

Single Exit Strategy. Every bridge deal should have a primary exit and a secondary exit. If your primary is a sale, your secondary might be a rental conversion + permanent loan. If your primary is an agency refinance, your secondary might be a portfolio lender refinance at slightly higher rates.

Choosing Speed Over Lender Quality. Closing in 7 days means nothing if the lender calls the loan at 6 months because their capital is stressed or they have a different interpretation of the loan terms. Execution certainty matters as much as closing speed.

Frequently Asked Questions — California Bridge Loan Strategy

Q1: How do I know if a property is a good candidate for a hard money bridge loan in California?

Strong bridge loan candidates share these characteristics: property is below market value or below market rents (value creation potential), there is a clear, well-supported path to a higher-value exit (comps or stabilized income analysis), the project timeline fits within 6-24 months, and the all-in cost basis (purchase + renovation + financing + exit costs) leaves meaningful profit. Weak candidates have thin margins, unclear exit strategies, or require bridge periods longer than 24 months.

Q2: What is the best California market for fix-and-flip in 2025?

Sacramento and the Inland Empire continue to offer the strongest fix-and-flip fundamentals — lower acquisition costs relative to ARV, strong buyer demand, and less regulatory complexity than the Bay Area or Los Angeles. For larger deal sizes, Los Angeles value-add multifamily remains one of the most compelling strategies despite its regulatory complexity.

Q3: Can I use a California hard money bridge loan for a 1031 exchange?

Yes, and this is one of the most valuable uses of bridge financing in the California market. A bridge loan allows 1031 exchange investors to close the replacement property quickly (as a near-cash buyer) and then refinance to permanent financing after acquisition. The key is selecting a lender who understands 1031 timing constraints and can commit to funding before the 180-day deadline.For California hard money bridge loan strategy consultation, contact America Mortgages — specialists are available across time zones to discuss your specific deal.

Global Capital Access, Institutional Speed, and the Relationships That Close Deals Others Can’t

Key Takeaways

GMG Capital and America Mortgages bring global capital to California deals — removing the size and complexity ceilings that constrain local lenders.

Experienced lenders and brokers refer their hardest deals here because the network, expertise, and capital depth are unmatched.

The combination of local California market knowledge + institutional global capital is the competitive moat.

Speed, certainty of execution, and relationship depth are the three pillars that define why professionals choose GMG and America Mortgages.

This isn’t just a referral, it’s a strategic advantage for every deal in the pipeline.

Introduction: The Problem With Most California Hard Money Lenders

There are hundreds of hard money lenders operating in California. They advertise on Google, LinkedIn, and BiggerPockets. They promise fast closings, high LTVs, and low rates. And many of them, when a serious deal lands on their desk, a $15 million mixed-use repositioning in Downtown Los Angeles, a $30 million construction loan for a luxury Marin County development, an $8 million bridge on a distressed coastal hospitality asset, quietly fold. Their capital runs out. Their syndication takes too long. Their underwriting team has never seen a deal this complex.

This is the wall that sophisticated California real estate professionals: developers, operators, family offices, and institutional investors, hit regularly with local hard money lenders. And it is precisely why they turn to GMG Capital and America Mortgages.

This article explains what makes these firms genuinely different: not in marketing language, but in structural, operational, and capital terms that matter when a $20 million deal needs to close in two weeks.

Part 1: What ‘Global Capital Access’ Actually Means — And Why It Changes Everything

The Local Lender Capital Constraint Problem

Most California hard money lenders operate from a pool of capital that is fundamentally local and finite. They raise money from local high-net-worth investors, family offices, and small funds. Their typical deal size is $500,000 to $5 million. When a larger deal comes in, they either pass, or they spend weeks trying to syndicate the loan across multiple capital sources — which kills the one thing their borrower needs: speed.

Capital Constraint Analogy A local hard money lender with a $20 million capital pool is like a regional airline. They can serve local routes efficiently. But when you need to cross an ocean — when you need $25 million closed in 10 days — they simply don’t have the aircraft. GMG Capital and America Mortgages are the international carriers: global capital reach, large-capacity vehicles, and the infrastructure to fly anywhere.

What Global Capital Access Unlocks

Capability

Local Hard Money Lender

GMG Capital / America Mortgages

Maximum Loan Size

Typically $5M – $15M cap

No practical ceiling — $50M+ achievable

Capital Sources

Local HNW investors, small family offices

Global institutional capital: Asia, Europe, Middle East, US

Institutional underwriting teams = same speed at any size

Relationship Depth

Single lender relationship

Network of global capital partners — best execution guaranteed

Market Downturns

Capital may pull back

Diversified global capital = consistent deployment

Part 2: The GMG Capital Difference — Institutional Expertise Meets Private Flexibility

Who GMG Capital Serves and Why

GMG Capital operates at the intersection of institutional discipline and private lender flexibility. This is not a contradiction, it is a deliberately engineered competitive advantage. The clients who choose GMG are not desperate borrowers. They are:

Experienced California developers who have outgrown the local hard money market and need lenders who can scale with their ambitions

Family offices executing value-add multifamily strategies across multiple California markets simultaneously

International investors deploying capital into US real estate who need a lender that understands both sides of the transaction

Seasoned mortgage brokers who have a complex deal and need a capital partner who won’t embarrass them in front of their client

Real estate operators who need certainty of execution, not a lender who might pull back at the last minute

The Three Pillars of GMG’s Market Position

Pillar 1: Capital Depth Without Concentration Risk

GMG’s capital base is deliberately diversified across geographies and investor types. This means no single capital source represents more than a fraction of total deployment capacity. In practical terms: when markets shift, when one investor pulls back, when interest rates move — GMG’s ability to lend is not compromised by a single relationship going cold. This consistency is worth more to a serious operator than a slightly lower rate from a lender whose capital is concentrated and fragile.

Pillar 2: Underwriting Sophistication at Private Lender Speed

The reason most institutional lenders (banks, insurance companies, CMBS) take 45-90 days to close is not because the analysis takes that long, it’s because of bureaucratic review layers, committee approval processes, and regulatory compliance burdens. GMG has stripped out the bureaucracy while retaining the analytical rigor. The result: institutional-quality underwriting completed in a timeframe that competes with, and often beats — local hard money lenders.

Pillar 3: Relationship Capital

In real estate finance, relationships are leverage. GMG’s network includes appraisers, title companies, environmental consultants, attorneys, and correspondent lenders who have worked on hundreds of California transactions. When a complex situation arises, an unexpected title issue, a zoning variance question, an appraisal that comes in light — GMG’s relationship network provides solutions that a lender without that depth cannot access.

Part 3: America Mortgages — The Global Borrower’s Mortgage Specialist

What Makes America Mortgages Different

America Mortgages was built to solve a specific, underserved problem: US real estate financing for borrowers who exist outside the traditional US lending framework. This includes foreign nationals, US expats, international investors, and domestic borrowers with complex financial profiles that trip up standard underwriting.

The Global Capital Connector: Accessing lenders, funds, and capital sources across Asia, Europe, the Middle East, and beyond, bringing international liquidity to California deals.

The Complex Borrower Specialist: Foreign income documentation, offshore entity structures, ITIN borrowers, multi-jurisdictional tax situations, America Mortgages has structured solutions for all of it.

The Network Hub: For California hard money deals, America Mortgages functions as the hub connecting qualified borrowers with the right capital source, at the right terms, every time.

The America Mortgages + GMG Capital Combination — A Unique Competitive Moat

When America Mortgages and GMG Capital work together on a California hard money bridge loan, the combination produces something genuinely rare in the market:

What It Produces

Why It Matters to the Borrower

Global capital at local speed

Deals that are too large for local lenders close in days, not months

International borrower expertise + California deal knowledge

No borrower profile is too complex — foreign nationals, offshore entities, US expats all accommodated

Broker-level market access + direct capital deployment

Best execution: not limited to one capital source, but accessing the optimal one for each deal

Rigorous underwriting without bureaucratic delay — the best of both worlds

Compliance depth + transactional agility

Fully licensed, regulated, and compliant — without sacrificing the speed that makes hard money valuable

Part 4: Why Seasoned Lenders and Brokers Refer to GMG and America Mortgages

The Referral Economy in Hard Money Lending

The professional referral is the highest form of credibility in financial services. When a seasoned California mortgage broker, someone who has seen hundreds of deals, worked with dozens of lenders, and knows exactly who performs, sends their most valuable client to a specific lender, that is not marketing. That is a proven track record speaking.

GMG Capital and America Mortgages receive referrals from:

Other hard money lenders whose deal exceeds their capital capacity

Conventional mortgage brokers with a borrower who needs a bridge to their long-term financing

Commercial real estate brokers who need their buyer to close competitively

Real estate attorneys structuring complex acquisitions or 1031 exchange transactions

Family office wealth managers whose clients are deploying capital into US real estate

International real estate agents and advisors whose clients are foreign investors entering the California market

What Referring Professionals Experience

“I’ve referred three deals to GMG and America Mortgages in the past 18 months. Every single one closed. Two of them were deals I had already tried with two other lenders. The combination of capital access and execution certainty is unlike anything else in the California market.” — Senior California Commercial Mortgage Broker

“My client needed $22 million to close a multifamily acquisition in 12 days. Every local lender I called either couldn’t go that high or said they needed 30+ days. GMG closed it in 11 days at a rate that was competitive with the best terms we’d seen at that speed. That kind of execution is worth every basis point.” — California Real Estate Investment Advisor

The ‘Last Resort Fallacy’ — A Contrarian Perspective

The conventional wisdom is that sophisticated borrowers avoid hard money unless they have no other choice. This is precisely backwards for the California market. Here’s why:

Speed has economic value. A borrower who can credibly offer a 10-day cash-equivalent close (using hard money) regularly negotiates 5-10% purchase price discounts on off-market deals. On a $5M acquisition, that’s $250,000-$500,000 in acquisition profit, far exceeding the additional cost of hard money financing.

Flexibility has economic value. The ability to acquire a property in its current (impaired) state and reposition it, without the income-based qualification constraints of conventional lending, creates value-add opportunities unavailable to conventional borrowers.

Relationship has economic value. Operators with established hard money relationships, who can call GMG Capital and get a term sheet in 24 hours, have a structural deal-sourcing advantage over competitors who have to start lender conversations from scratch for every deal.

Part 5: The Deal Types Where GMG and America Mortgages Excel

Deal Type

Why GMG / America Mortgages Excel

Typical Loan Size

Large California Multifamily Bridge ($10M+)

Capital depth to fund without syndication; multifamily expertise

$10M – $50M+

Foreign National California Acquisitions

International borrower documentation expertise + hard money flexibility

$500K – $20M+

Complex Commercial Repositioning

Experienced with value-add underwriting; understands stabilized exit

$5M – $50M+

Ground-Up Construction Bridge

Experienced construction monitoring; draw management expertise

$3M – $30M+

Distressed Asset Acquisition

High-complexity underwriting; quick due diligence

$1M – $20M+

1031 Exchange Acquisition Leg

Speed + certainty for time-sensitive replacement property

$500K – $20M+

Portfolio / Cross-Collateralized Loans

Global capital allows cross-collateralization across multiple assets

$5M – $100M+

International Borrower US Real Estate

America Mortgages expertise; offshore entity structuring

$500K – $30M+

Part 6: The Process — Working with GMG and America Mortgages

From First Contact to Funding: The Experience

Initial Consultation (Day 1): Contact the team with a brief deal summary, property, loan request, use of funds, exit strategy. America Mortgages has specialists available across time zones to accommodate international clients.

Preliminary Term Sheet (Within 24-48 Hours): A non-binding indication of interest with proposed rate, LTV, term, and points, faster than almost any competitor in the California market.

Formal Underwriting Package: Borrower provides documentation package (property details, financials, entity docs). The GMG underwriting team begins parallel-tracking appraisal, title, and credit review.

Appraisal and Due Diligence (Days 3-10): GMG works with a network of California-experienced appraisers to expedite valuation. Title is simultaneously reviewed for any issues.

Loan Committee and Commitment Letter (Days 7-14): Formal approval and commitment letter issued. Unlike committees at large banks, GMG’s decision-making process is streamlined for speed without sacrificing rigor.

Document Preparation and Closing (Days 10-21): Loan documents are prepared, escrow coordinates, funds are wired. GMG and America Mortgages close California hard money bridge loans in 10-21 days as standard practice.

Common Mistakes When Choosing a California Hard Money Lender

Choosing solely on advertised rate. A lender who advertises 9% but can’t fund your deal size or closes in 45 days is worse than a lender at 10.5% who closes in 12 days. Evaluate execution reliability, not just rate.

Not verifying capital availability. Ask specifically: ‘Is the capital for my loan already committed, or do you need to syndicate it?’ Syndicated capital = timing uncertainty. Committed capital = certainty.

Ignoring licensing. Verify the lender’s DRE or CFL license. Unlicensed California lenders create legal risk for the borrower as well.